Eurozone Macro Daily(Beta Mode)

Mixed PMIs and Dutch Inflation Add to Euro Pressure

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,077.15 | -0.43% |

| DAX | 24,914.67 | +0.48% |

| CAC 40 | 8,244.43 | +0.00% |

| EUR/USD | 1.16 | -0.41% |

| EUR/GBP | 0.86 | -0.13% |

| EUR/JPY | 185.68 | -0.12% |

| Gold | 4,379.30 | -2.16% |

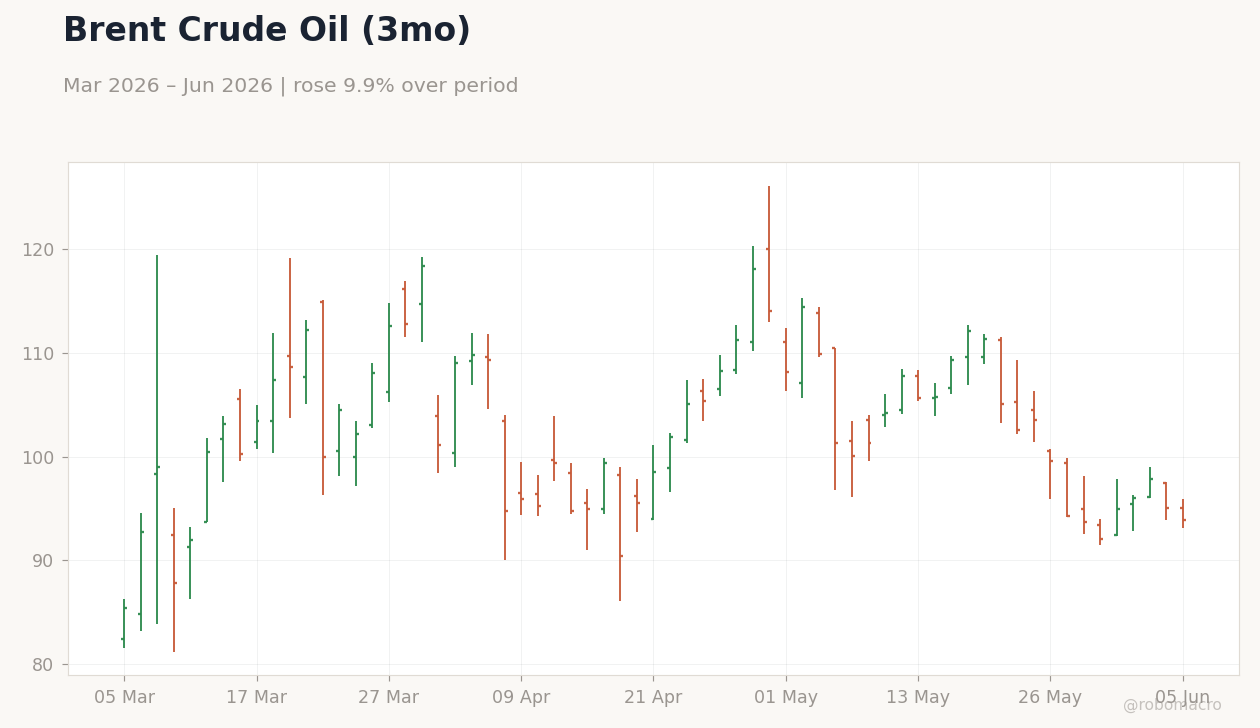

| Brent Crude | 93.61 | -1.49% |

| Bitcoin | 60,800.97 | -4.70% |

| German 2Y Bund | - | - |

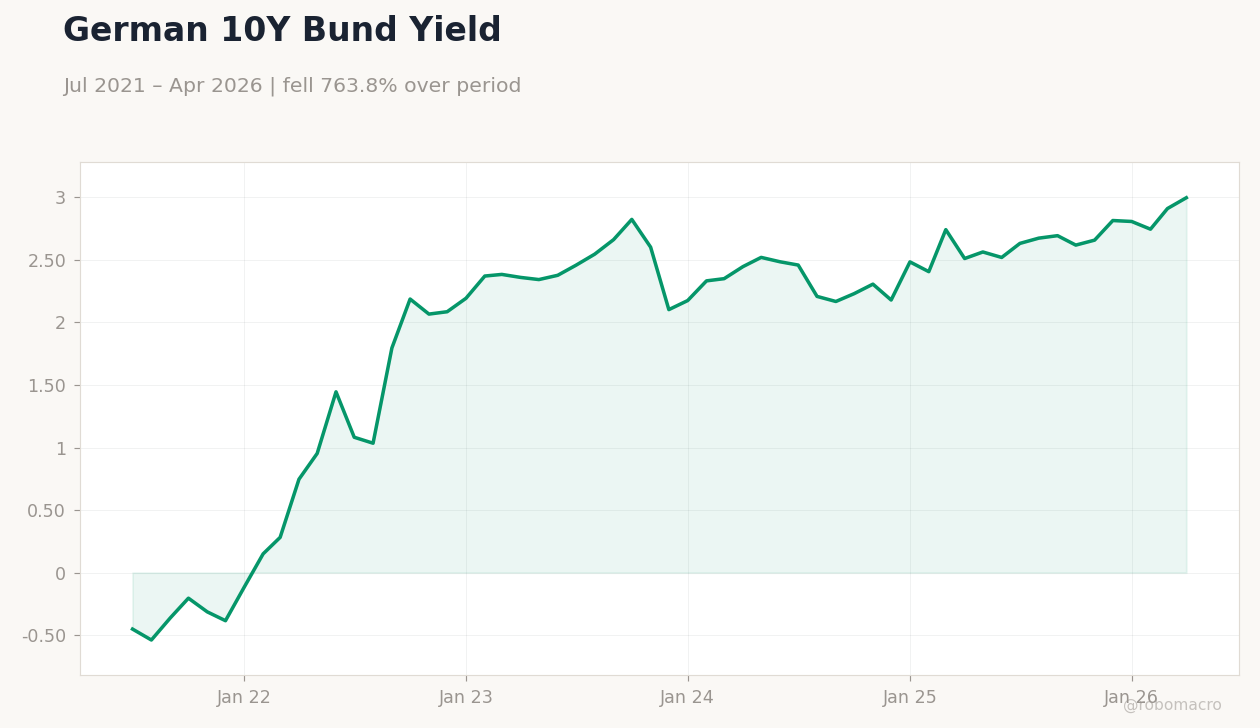

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Retail Sales Month-over-Month | -0.30 | -0.40 | -0.30 |

| Retail Sales Year-over-Year | -0.20 | - | -0.30 |

| S&P Global Manufacturing PMI Index | 51.70 | 52 | 51.20 |

| S&P Global Manufacturing PMI Index | 52.10 | 52 | 52.90 |

| Inflation Rate Year-over-Year Preliminary | 2.80 | - | 3.50 |

| Unemployment Level Change | -62,700 | -56,800 | -36,300 |

| S&P Global Services PMI | 47.90 | 48 | 50.10 |

| S&P Global Services PMI | 49.80 | - | 49.40 |

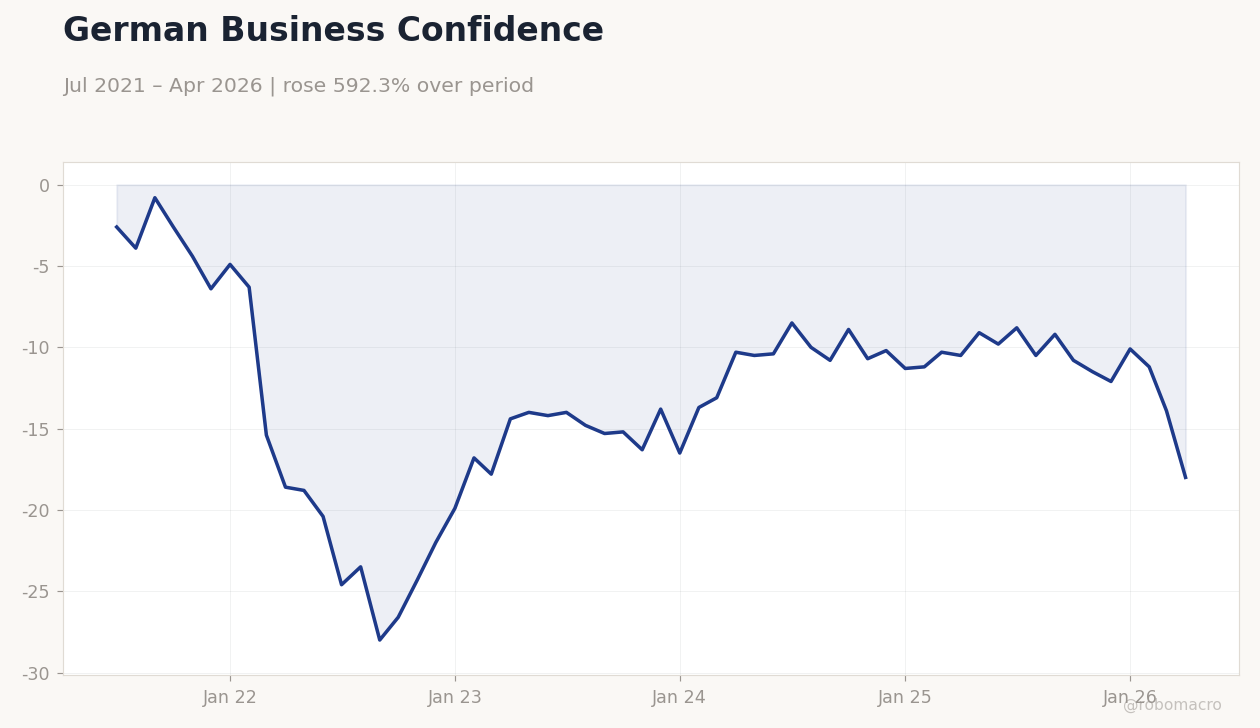

German Business Confidence | Type: macro_line | Confidence Index: -18 (2026-04-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.9,-18

German Business Confidence | Type: macro_line | Confidence Index: -18 (2026-04-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.9,-18

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Month-over-Month | 1 | -0.20 | 22:45 |

| Trade Balance | -6,900m | -6,500m | 22:45 |

| Retail Sales Month-over-Month | 0.80 | 0.20 | 01:00 |

- Spanish manufacturing PMI fell to 51.2 while Italian rose to 52.9, showing uneven factory momentum across the bloc.

- Dutch headline inflation jumped to 3.5% y/y, adding pressure on services prices amid energy cost rebound.

- Euro Stoxx 50 declined 0.43% and EUR/USD dropped 0.41% as growth concerns resurfaced after Q1 contraction.

Yesterday's Recap

German retail sales printed -0.3% m/m, matching the prior month and beating the -0.4% consensus, while the y/y rate slipped to -0.3%. Spanish manufacturing PMI eased to 51.2 from 51.7, underperforming expectations, whereas Italian manufacturing PMI strengthened to 52.9 from 52.1. Dutch inflation accelerated sharply to 3.5% y/y.

Spanish unemployment declined by 36,300, less than the 56,800 drop forecast. Spanish services PMI rebounded to 50.1 from 47.9, but Italian services PMI edged down to 49.4. Equity markets showed mixed performance with the DAX rising 0.48% while the Euro Stoxx 50 fell 0.43%.

The German 10-year Bund yield climbed 3 basis points to 3.00% and EUR/USD weakened to 1.16.

The Day Ahead

French industrial production and trade balance figures are due this evening, with markets expecting a 0.2% m/m drop in output after last month’s 1% gain. Italian retail sales are scheduled for release overnight, with consensus pointing to a 0.2% m/m increase following the prior 0.8% rise. No major ECB speakers are listed.

Attention will also turn to any updates on PEPP reinvestment flows. Traders will monitor early reactions for signs of softening demand in the core economies.

Other Economic Notes

Eurozone unemployment stands at 6.7%. First-quarter GDP contracted 0.2%, driven by a sharp Irish slump and weaker household spending. Preliminary Dutch inflation at 3.5% y/y highlights renewed energy-price risks that could complicate the return to target.

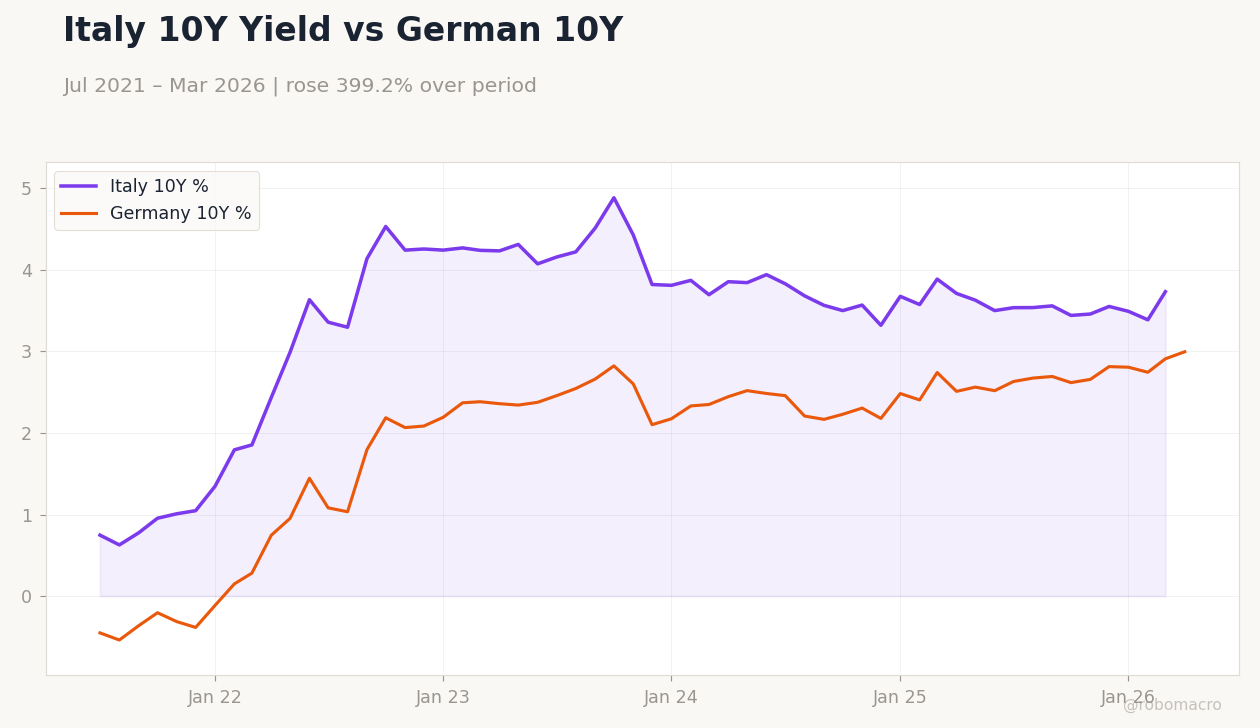

Member-state divergences remain pronounced, with Italian factory surveys outperforming Spanish readings. Fiscal discussions in Germany continue to focus on potential adjustments to the debt brake without immediate market impact.

Global Macro News

The G7 summit in France will draw attention to transatlantic trade and defense spending, with reports of possible Pentagon cancellation of a German missile deal adding geopolitical friction. Broader risk sentiment weakened as Bitcoin fell 4.7% and gold dropped 2.16%. <i>↓ p.2</i>