Eurozone Macro Daily(Beta Mode)

German Orders Slump Widens Bund Yield Gap

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,062.29 | +0.00% |

| DAX | 24,759.05 | -0.75% |

| CAC 40 | 8,199.29 | -0.23% |

| EUR/USD | 1.15 | -0.59% |

| EUR/GBP | 0.86 | -0.02% |

| EUR/JPY | 184.78 | -0.53% |

| Gold | 4,365.70 | +0.66% |

| Brent Crude | 94.65 | +1.68% |

| Bitcoin | 63,631.95 | +0.62% |

| German 2Y Bund | - | - |

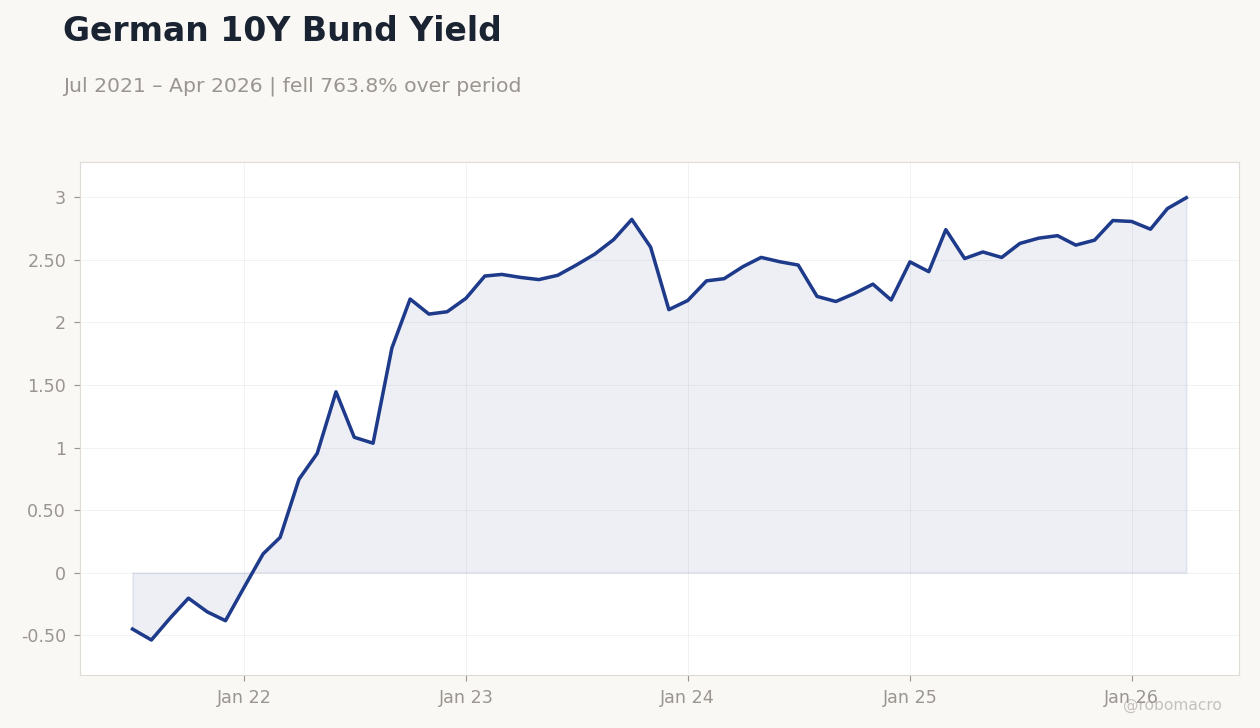

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Factory Orders Month-over-Month | 5 | -1.20 | -3.80 |

German 10Y Bund Yield | Type: macro_line | 10Y Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | 10Y Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 14,300m | 14,200m | 22:00 |

| Exports Month-over-Month | 0.50 | - | 22:00 |

| Industrial Production Month-over-Month | -0.70 | 0.50 | 22:00 |

| Industrial Production Month-over-Month | 0.70 | 0.10 | 00:00 |

- German factory orders contracted 3.8% m/m in May, missing consensus by a wide margin and highlighting persistent manufacturing weakness.

- DAX fell 0.75% while the 10-year Bund yield climbed 3 bp to 3.00% as markets adjusted rate expectations.

- Eurozone investor sentiment improved modestly but Germany continues to weigh on the bloc’s growth outlook.

Yesterday's Recap

German factory orders dropped 3.8% month-over-month in May against a consensus of -1.2%, confirming a sharp reversal from April’s 5% gain and underscoring the sector’s vulnerability to external demand. The miss triggered modest selling in German equities, with the DAX closing 0.75% lower at 24,759.05 while the broader Euro Stoxx 50 held flat at 6,062.29. The euro weakened across the board, with EUR/USD falling 0.59% to 1.15 and EUR/JPY declining 0.53% to 184.78.

Brent crude rose 1.68% to $94.65 amid supply concerns, and gold advanced 0.66% to $4,365.70 as a hedge. The German 10-year Bund yield increased 2.97% to 3.00%, reflecting reduced expectations for near-term ECB easing. No other major Eurozone data were released on the day.

The Day Ahead

Markets will focus on Germany’s May trade balance, exports and industrial production figures due at 22:00 ET, all carrying medium-to-high impact. Italian industrial production for April follows at midnight, with consensus pointing to a modest 0.1% gain. A significant undershoot in German output could reinforce bets on further ECB accommodation.

No Governing Council speeches or policy publications are scheduled. Traders will also monitor any updates on EU fiscal discussions that could influence periphery spreads.

Other Economic Notes

Investor surveys show sentiment improving outside Germany, yet the country’s persistent manufacturing drag continues to limit the recovery. Discussions around a “breathing” debt brake in Berlin highlight ongoing fiscal policy uncertainty that could affect bund curves. Broader demographic trends, including France’s declining birth rate, add long-term headwinds to potential growth.

Global Macro News

Middle East tensions are lifting inflation expectations and prompting some ECB officials to flag the possibility of further rate hikes despite the 2.00% deposit rate. European leaders backed direct talks between Ukraine and Russia, reducing near-term geopolitical risk premia for the euro. Global energy prices remain elevated, supporting Brent but pressuring household spending across member states.

<i>↓ p.2</i>