Eurozone Macro Daily(Beta Mode)

German Orders Slump, Bund Yields Jump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,055.88 | -0.11% |

| DAX | 24,471.81 | -0.59% |

| CAC 40 | 8,223.41 | +0.29% |

| EUR/USD | 1.16 | +0.23% |

| EUR/GBP | 0.86 | +0.07% |

| EUR/JPY | 185.28 | +0.34% |

| Gold | 4,187.10 | -1.71% |

| Brent Crude | 92.01 | +0.61% |

| Bitcoin | 61,540.01 | -0.17% |

| German 2Y Bund | - | - |

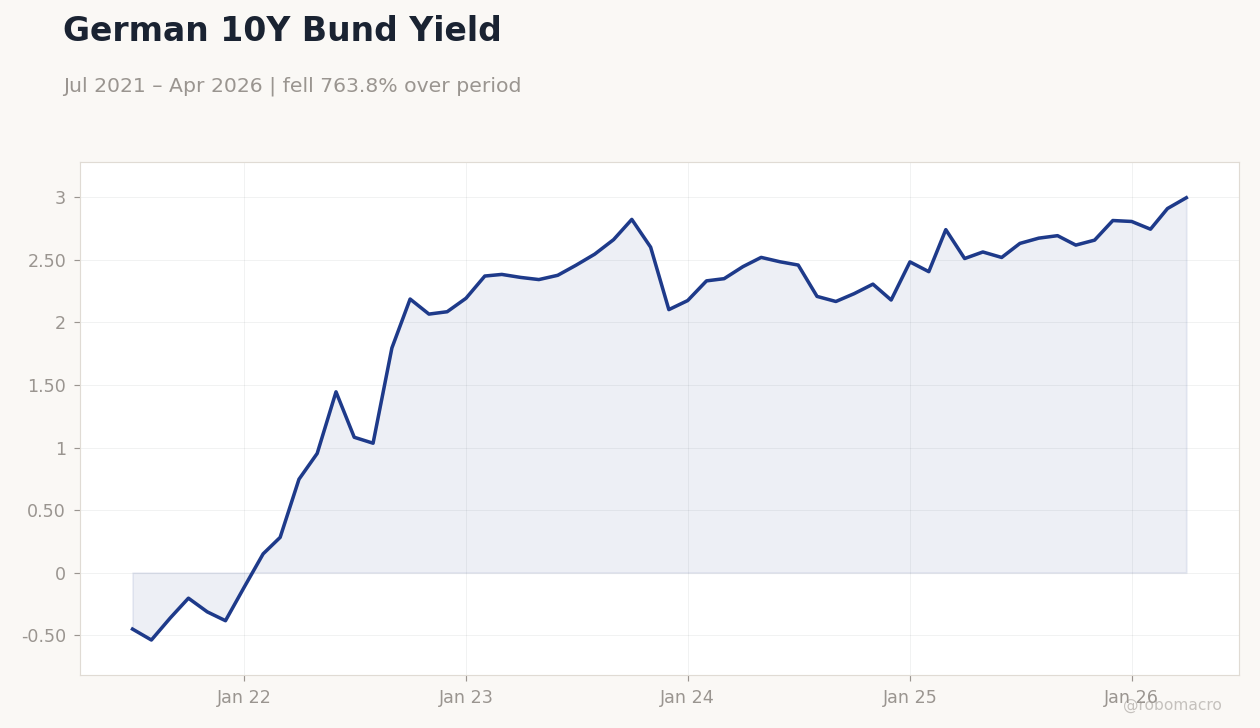

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Factory Orders Month-over-Month | 4.50 | -1.20 | -3.80 |

| Trade Balance | 14,700m | 15,000m | 14,500m |

| Exports Month-over-Month | 0.30 | - | 0.90 |

| Industrial Production Month-over-Month | -0.10 | 0.40 | 0.40 |

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Industrial Production Month-over-Month | 0.70 | 0 | 00:00 |

- German factory orders fell 3.8% m/m in May, well below the -1.2% consensus, while industrial production rose 0.4% m/m in line with forecasts.

- German 10-year Bund yields rose 2.97% to 3.00% as markets digested the mixed data and priced limited ECB easing.

- Euro Stoxx 50 slipped 0.11% and DAX declined 0.59%, while EUR/USD gained 0.23% to 1.16 amid divergent equity moves across France and Germany.

Yesterday's Recap

German May factory orders contracted 3.8% m/m against a -1.2% consensus, confirming a sharp slowdown in manufacturing demand. The trade balance narrowed to €14.5 billion from €14.7 billion previously, while exports rose 0.9% m/m. German industrial production matched the 0.4% consensus, providing a modest offset.

Equity markets reflected the weakness, with the DAX falling 0.59% to 24,471.81 and the Euro Stoxx 50 edging 0.11% lower to 6,055.88. The CAC 40 gained 0.29% to 8,223.41. German 10-year Bund yields surged 2.97% to 3.00%, lifting borrowing costs across the curve.

EUR crosses strengthened modestly, with EUR/USD at 1.16 and EUR/JPY at 185.28.

The Day Ahead

Italian industrial production for April is due today, with consensus at 0.0% m/m after a 0.7% prior gain. Markets will monitor the release for signs of sustained momentum in Italy’s manufacturing sector. No high-impact German or French data are scheduled.

Attention will also turn to any follow-up comments from Banque de France officials on the 2026 inflation outlook. Trading desks expect limited volatility ahead of the ECB’s next policy meeting unless Italian figures deviate sharply from expectations.

Other Economic Notes

Softer German orders data reinforce the view that Eurozone growth remains uneven, with Germany lagging France and Italy. Dutch consumer spending growth in April added some support to regional demand, tempering immediate recession concerns. Absenteeism trends in France and rising executive absences point to persistent labor-market frictions that could cap productivity gains.

Energy-price differentials between France and Germany have narrowed on summer cooling-demand risks, adding a mild upside bias to near-term inflation prints.