Eurozone Macro Daily(Beta Mode)

German Orders Slump, Bund Yields Jump

Market Snapshot

| Asset | Level | Change |

|---|---|---|

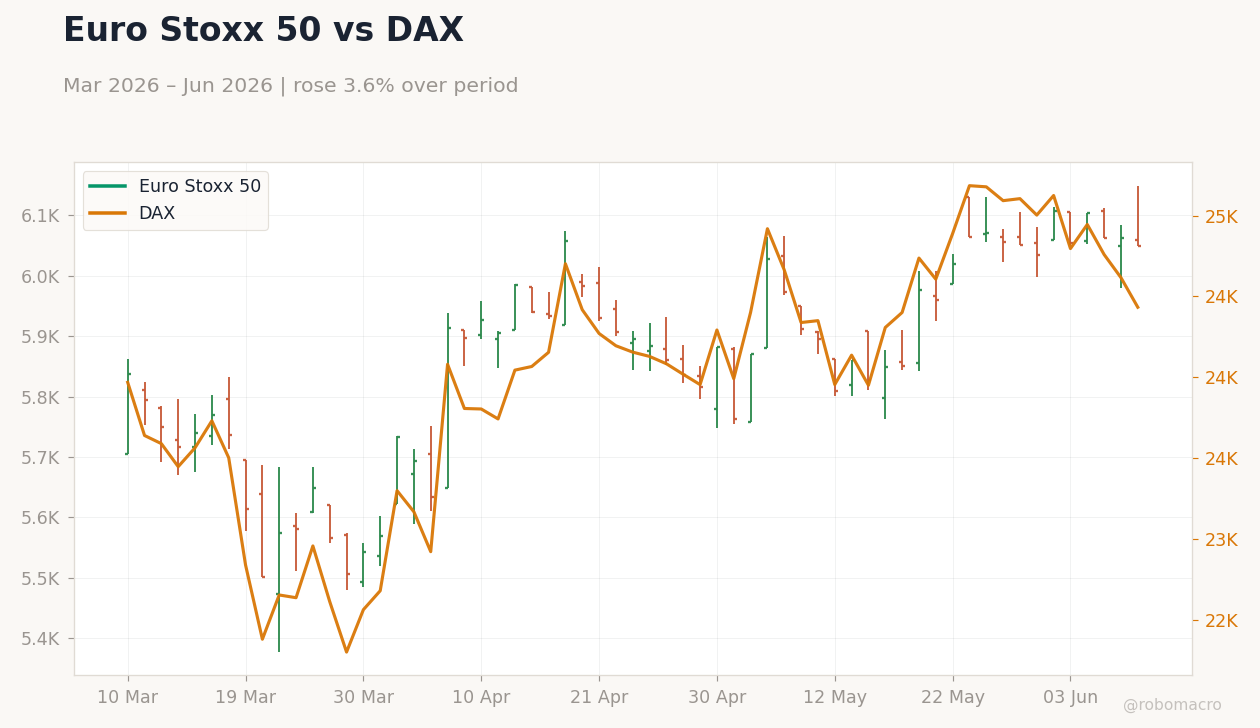

| Euro Stoxx 50 | 6,049.74 | -0.21% |

| DAX | 24,224.34 | -0.85% |

| CAC 40 | 8,203.43 | +0.05% |

| EUR/USD | 1.16 | +0.13% |

| EUR/GBP | 0.86 | -0.25% |

| EUR/JPY | 185.36 | +0.19% |

| Gold | 4,097.80 | -0.25% |

| Brent Crude | 93.74 | +0.69% |

| Bitcoin | 62,808.96 | +1.89% |

| German 2Y Bund | - | - |

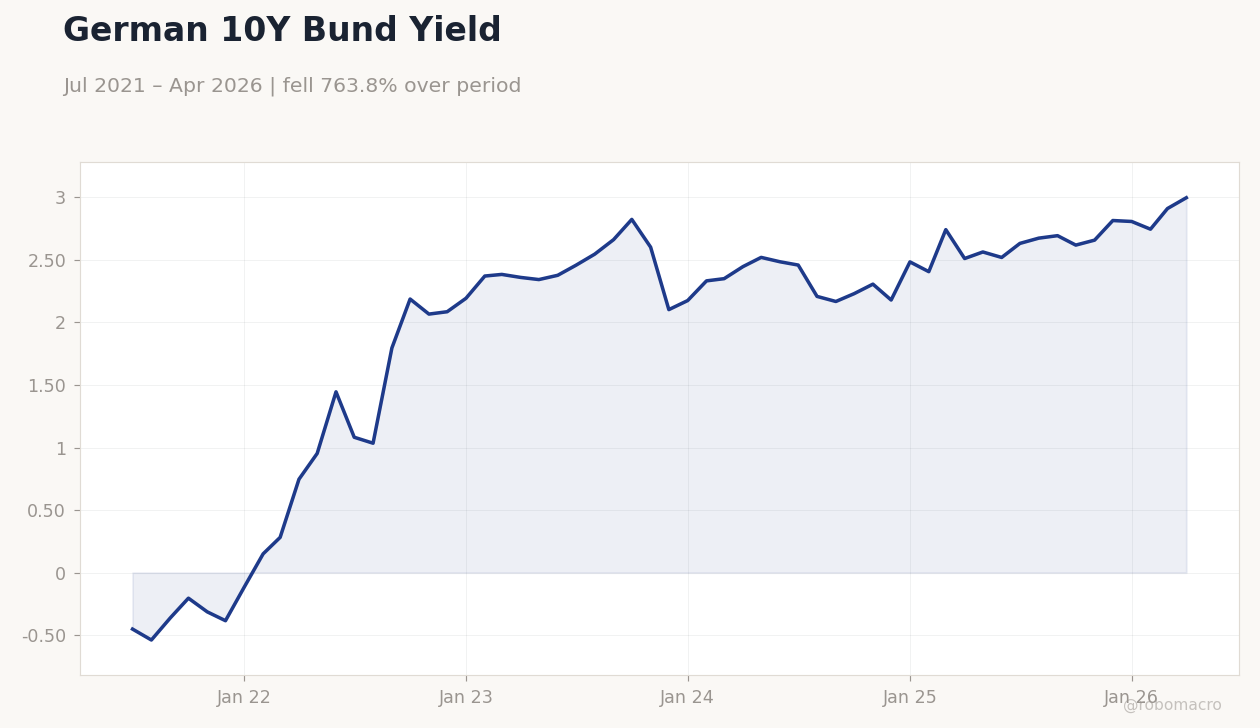

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Factory Orders Month-over-Month | 4.50 | -1.20 | -3.80 |

| Trade Balance | 14,700m | 15,000m | 14,500m |

| Exports Month-over-Month | 0.30 | - | 0.90 |

| Industrial Production Month-over-Month | -0.10 | 0.40 | 0.40 |

| Industrial Production Month-over-Month | 0.60 | -0.10 | 0.50 |

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- German factory orders fell 3.8% m/m in May, missing consensus of -1.2%, while Italian industrial production rose 0.5%.

- Euro Stoxx 50 declined 0.21% and DAX dropped 0.85% as German 10-year Bund yields climbed 2.97% to 3.00%.

- ECB Deposit Rate remains at 2.00% with markets shifting toward earlier tightening on Iran-driven inflation risks.

Yesterday's Recap

German May factory orders contracted 3.8% month-over-month against expectations of a 1.2% decline, while the trade balance narrowed to 14.5 billion euros. German exports rose 0.9% and industrial production increased 0.4%, matching forecasts. Italian industrial production expanded 0.5% month-over-month, beating the -0.1% consensus.

Equity markets closed mixed with the CAC 40 edging up 0.05% while the DAX posted the largest loss. The euro gained 0.13% versus the dollar to 1.16 and 0.19% versus the yen. German 10-year Bund yields surged nearly 3% to 3.00% as inflation concerns mounted.

Brent crude advanced 0.69% to 93.74 amid supply worries.

The Day Ahead

No major Eurozone data releases are scheduled for 11 June, leaving markets to digest yesterday’s German and Italian industrial figures. Attention will turn to any follow-up commentary from national central bank officials on inflation pressures linked to energy markets. EUR crosses may remain sensitive to global risk sentiment and US-Iran developments.

Equity futures point to a cautious open for the Euro Stoxx 50 and DAX. Traders will monitor Bund auction results and any shifts in OIS pricing around the 2.00% ECB Deposit Rate. Quiet conditions could persist absent fresh geopolitical headlines.

Other Economic Notes

DIW warned of a possible technical recession in Germany this year after energy price spikes from the Iran conflict slowed the recovery. EU finance ministers extended the Recovery and Resilience Facility disbursement window by twelve months to support member states. Eurozone unemployment stands at 6.70%, providing some buffer against labor-market deterioration.

Broader stagflation fears resurfaced as supply shocks coincide with still-elevated core inflation readings across Germany and France. National fiscal positions remain under scrutiny ahead of potential additional defense spending in several member states.