Eurozone Macro Daily(Beta Mode)

ECB Hikes Rates on Iran-Driven Inflation

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,056.96 | +0.78% |

| DAX | 24,251.13 | +0.23% |

| CAC 40 | 8,200.80 | +0.48% |

| EUR/USD | 1.16 | +0.26% |

| EUR/GBP | 0.86 | -0.05% |

| EUR/JPY | 185.38 | +0.11% |

| Gold | 4,197.40 | +2.62% |

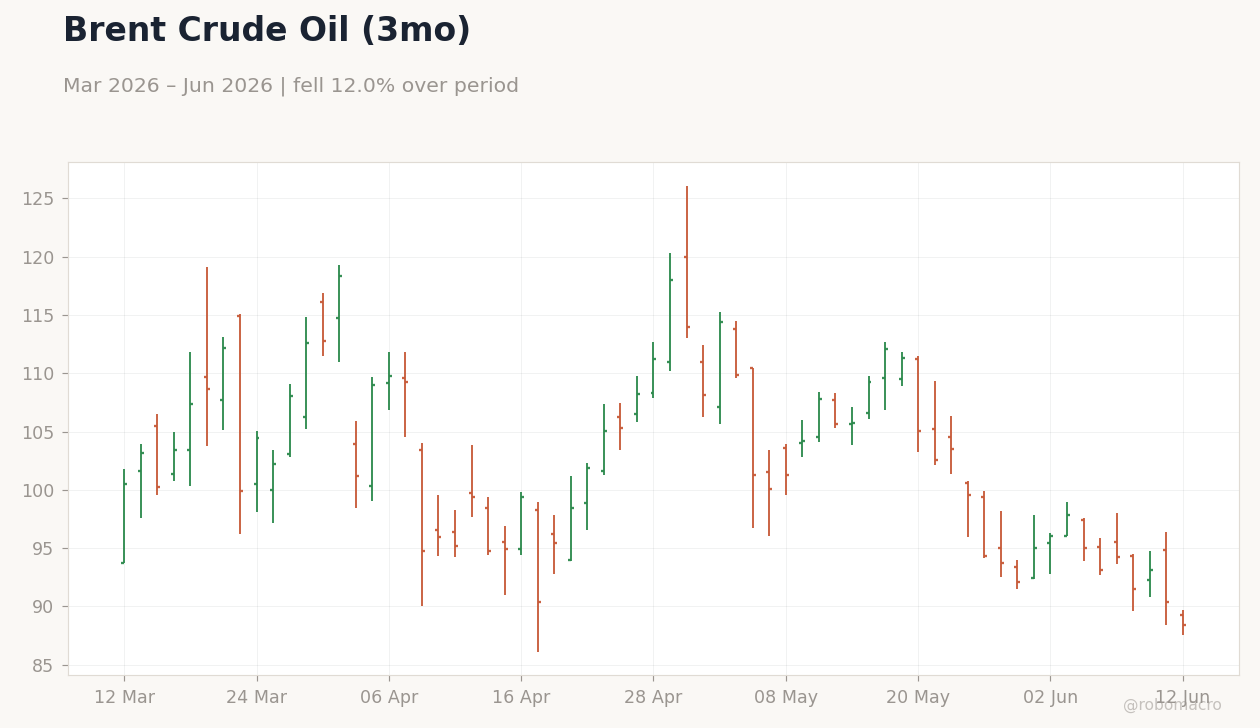

| Brent Crude | 88.28 | -2.32% |

| Bitcoin | 63,309.03 | +3.03% |

| German 2Y Bund | - | - |

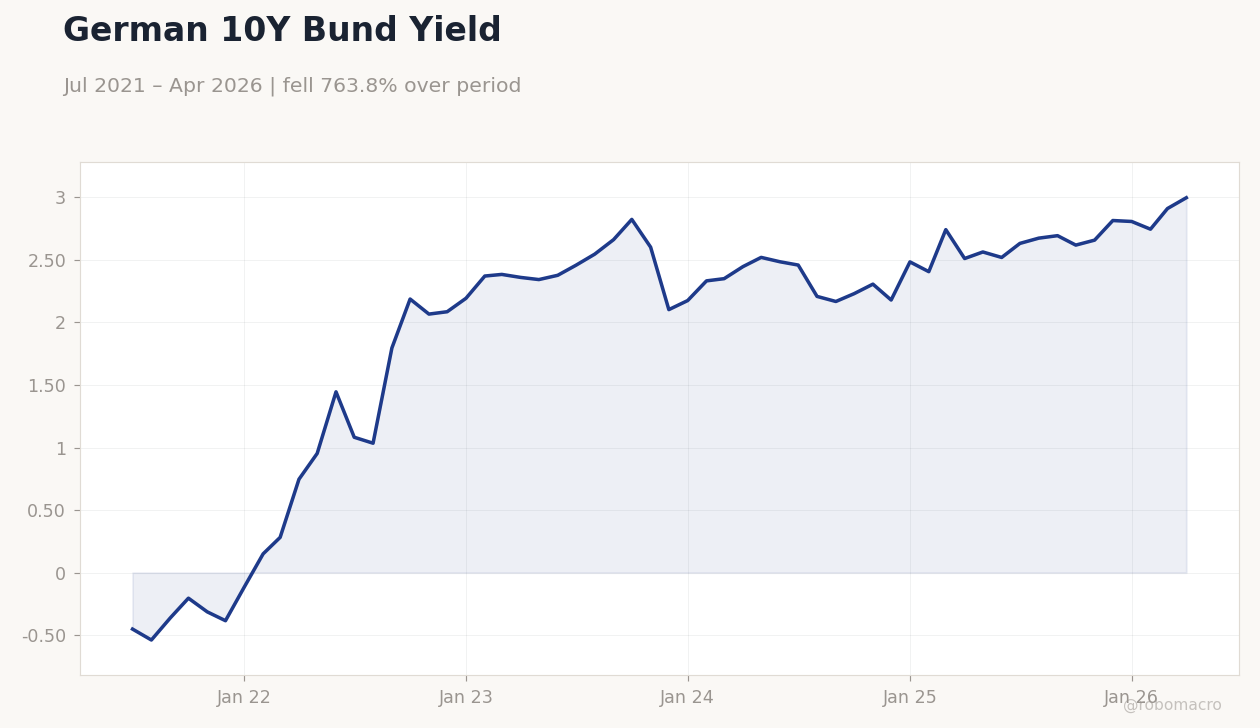

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Factory Orders Month-over-Month | 4.50 | -1.20 | -3.80 |

| Trade Balance | 14,700m | 15,000m | 14,500m |

| Exports Month-over-Month | 0.30 | - | 0.90 |

| Industrial Production Month-over-Month | -0.10 | 0.40 | 0.40 |

| Industrial Production Month-over-Month | 0.60 | -0.10 | 0.50 |

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- German factory orders plunged 3.8% m/m in May, missing consensus, while industrial production rose 0.4% m/m in line with expectations.

- ECB lifts deposit rate to 2.00% in first hike since 2023, citing Iran conflict-driven inflation pressures.

- Euro Stoxx 50 gains 0.78% and DAX rises 0.23% as EUR/USD climbs to 1.16 amid policy clarity.

Yesterday's Recap

German factory orders fell 3.8% m/m against a -1.2% consensus, while the trade balance narrowed to €14.5 billion. German exports rose 0.9% m/m and industrial production increased 0.4% m/m. Italian industrial production expanded 0.5% m/m, beating the -0.1% forecast.

Equity markets advanced with Euro Stoxx 50 at 6,056.96 and DAX at 24,251.13. EUR/USD reached 1.16 while the German 10-year Bund yield climbed to 3.00%. Gold surged 2.62% and Brent crude declined 2.32%.

The ECB raised its deposit rate to 2.00% to address inflation pressures linked to the Iran conflict. Markets reacted with modest gains in equities and a firmer euro as the decision delivered clearer policy direction.

The Day Ahead

No major Eurozone data releases are scheduled for 12 June. Markets will monitor follow-through from the ECB's rate decision and any comments on inflation persistence from Iran-related supply shocks. Attention may shift to German ZEW sentiment indicators due next week for clues on growth momentum.

French and Italian industrial output trends remain in focus after mixed May prints. EUR crosses could react to any fresh signals on quantitative tightening pace.

Other Economic Notes

Germany's DAX composition is shifting toward AI-exposed champions as US tech giants pour hundreds of billions into infrastructure. Volkswagen plans to cut 19,000 German jobs by end-2026 amid restructuring. France faces widening pension deficits that could pressure fiscal space ahead of EU budget talks.

Euroclear and Banque de France advance tokenization of €300 billion in short-term bonds to modernize markets. Eurozone unemployment stands at 6.70%. The committee voted to raise rates.

Global Macro News

The Iran conflict is lifting eurozone inflation, prompting the ECB's first rate increase since 2023. G7 leaders gather in France with China participating in rare economic talks hosted by Macron. Trump dismissed concerns over US inflation hitting a three-year high.

<i>↓ p.2</i>