Eurozone Macro Daily(Beta Mode)

Bundesbank Cuts 2026 Growth Outlook Amid Iran War

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,187.63 | +2.16% |

| DAX | 24,635.30 | +1.76% |

| CAC 40 | 8,350.87 | +1.83% |

| EUR/USD | 1.16 | +0.30% |

| EUR/GBP | 0.86 | -0.02% |

| EUR/JPY | 185.81 | +0.24% |

| Gold | 4,330.40 | +2.74% |

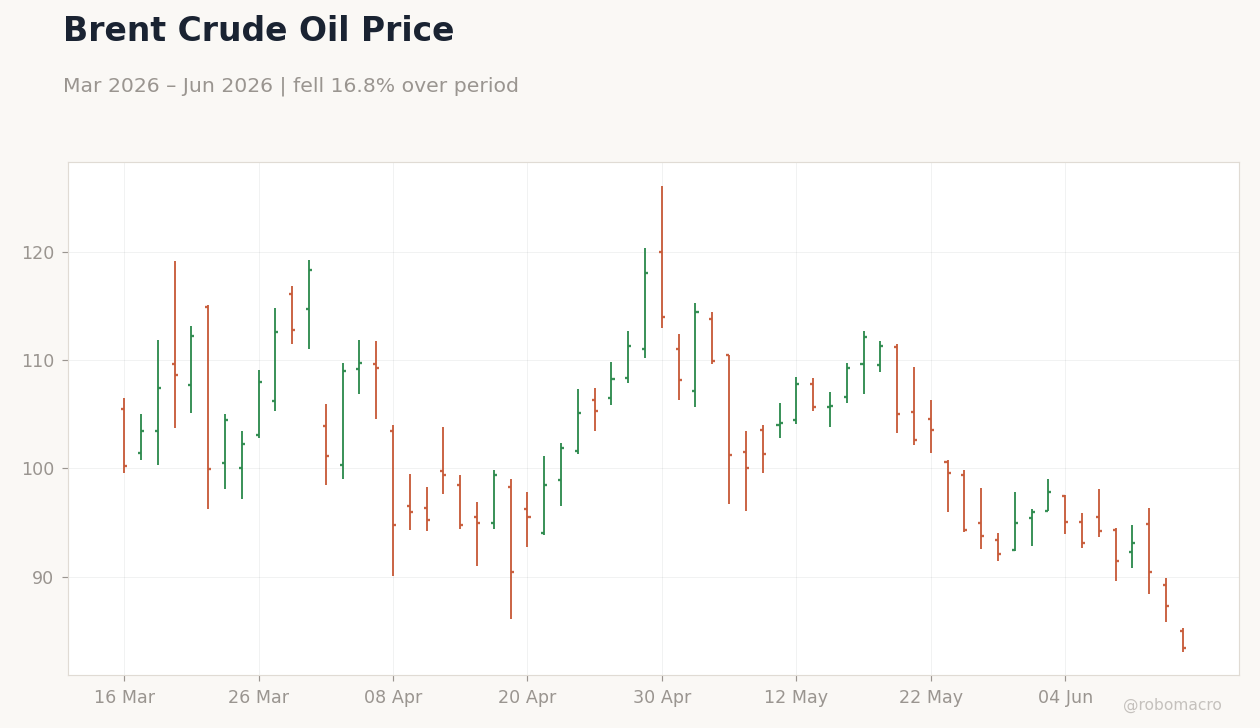

| Brent Crude | 83.43 | -4.47% |

| Bitcoin | 65,749.98 | +2.06% |

| German 2Y Bund | - | - |

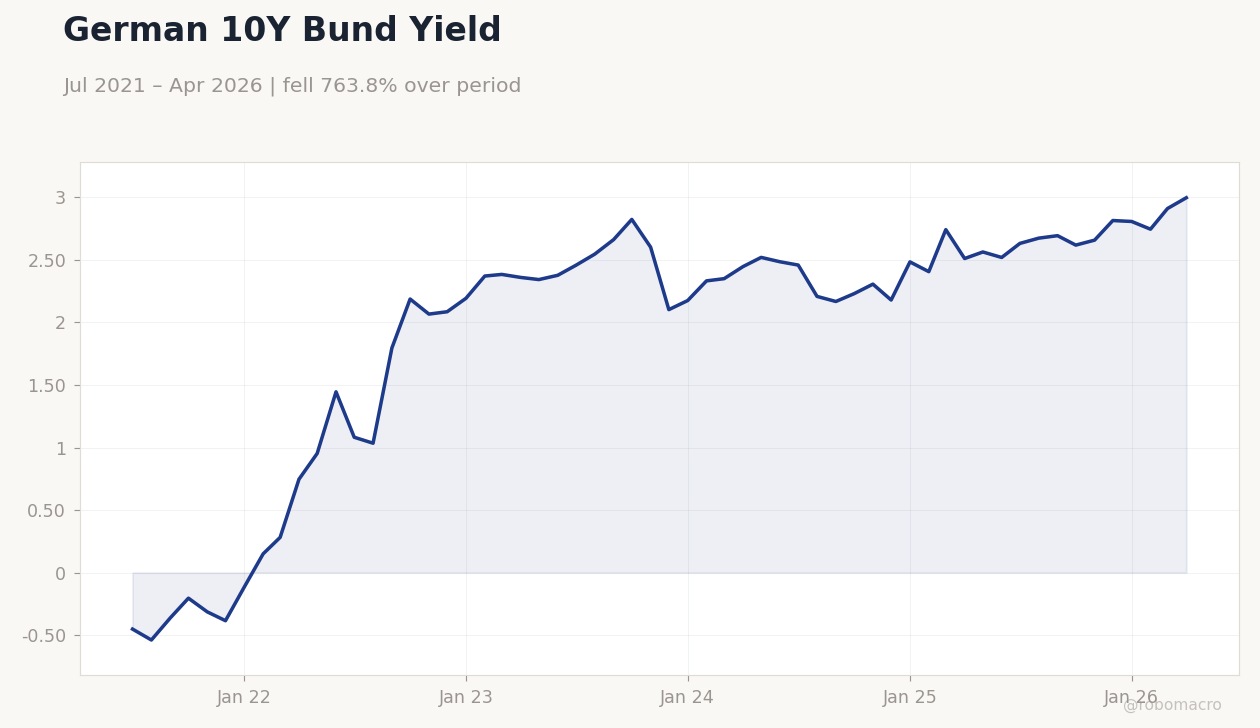

| German 10Y Bund | 3.00% | +2.97% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Wholesale Prices Month-over-Month | 2 | - | -0.60 |

| Wholesale Prices Year-over-Year | 6.30 | - | 5.90 |

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

German 10Y Bund Yield | Type: macro_line | Yield %: 2.996 (2026-04-01) | Range: -0.5386–2.996 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,2.996

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Trade Balance | 4,709m | - | 00:00 |

| ZEW Economic Sentiment Index | -10.20 | - | 01:00 |

| Headline Unemployment Rate | 3.90 | - | 20:30 |

| Producer Price Index Year-over-Year | 1.70 | - | 22:00 |

- German wholesale prices fell sharply in May, easing producer pressures.

- Euro Stoxx 50 rose 2.16% while German 10-year Bund yields climbed to 3.00%.

- Bundesbank lowered 2026 growth forecast and raised inflation projection amid energy shocks.

Yesterday's Recap

German wholesale prices contracted 0.6% month-over-month in May while the year-over-year rate eased to 5.9% from 6.3%, pointing to cooling pipeline pressures in Europe's largest economy. Equity markets advanced strongly with the Euro Stoxx 50 gaining 2.16% to 6,187.63, the DAX rising 1.76% and the CAC 40 adding 1.83%. The euro strengthened 0.30% against the dollar to 1.16 while gold surged 2.74%.

Brent crude dropped 4.47% to $83.43 per barrel. German 10-year Bund yields increased 2.97% to 3.00%. The moves followed Bundesbank announcements that trimmed Germany's 2026 growth expectation and lifted its inflation forecast because of the Iran conflict and associated energy costs.

The Day Ahead

Italy will release its May trade balance at midnight ET. Germany's closely watched ZEW Economic Sentiment Index prints at 01:00 ET and is expected to influence Bund and euro price action. The Netherlands reports its headline unemployment rate at 20:30 ET.

Germany follows with the producer price index year-over-year reading at 22:00 ET. Markets will also monitor any follow-up comments from ECB officials on the inflation outlook. These releases will set the tone for rate-sensitive assets ahead of the weekend.

Other Economic Notes

Fiscal stimulus is projected to support a modest German recovery in 2027-2028 despite slower near-term growth. Eurozone unemployment remains at 6.70%, providing some buffer against labour-market overheating. Energy-price volatility from the Middle East conflict continues to dominate inflation dynamics across member states.

Defence-spending initiatives discussed at EU level may add to fiscal outlays in coming years.

Global Macro News

The Iran conflict has pushed European energy costs higher, prompting the ECB to tighten policy further. G7 discussions in France highlighted coordinated efforts to reopen the Strait of Hormuz and stabilise oil flows. US tariff threats against French wine added friction to transatlantic trade talks.

<i>↓ p.2</i>