Eurozone Macro Daily(Beta Mode)

ZEW Surge Offsets Weak Wholesale Prices

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,300.07 | +0.68% |

| DAX | 24,931.55 | +0.08% |

| CAC 40 | 8,430.79 | -0.20% |

| EUR/USD | 1.15 | -0.73% |

| EUR/GBP | 0.87 | +0.05% |

| EUR/JPY | 185.08 | -0.63% |

| Gold | 4,320.00 | -0.89% |

| Brent Crude | 77.87 | -2.11% |

| Bitcoin | 64,027.06 | -2.40% |

| German 2Y Bund | - | - |

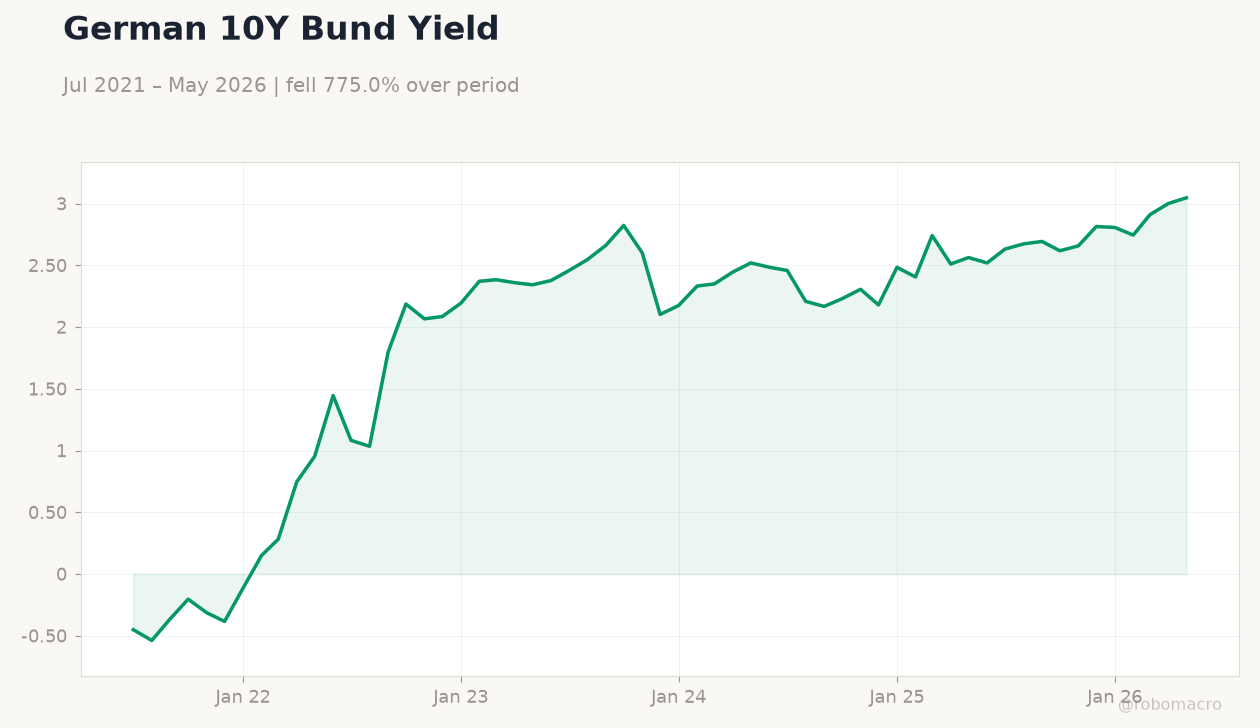

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Wholesale Prices Month-over-Month | 2 | 0.80 | -0.60 |

| Wholesale Prices Year-over-Year | 6.30 | - | 5.90 |

| Trade Balance | 4,813m | 5,190m | 4,293m |

| ZEW Economic Sentiment Index | -10.20 | -6 | 10.50 |

| Headline Unemployment Rate | 3.90 | - | 3.90 |

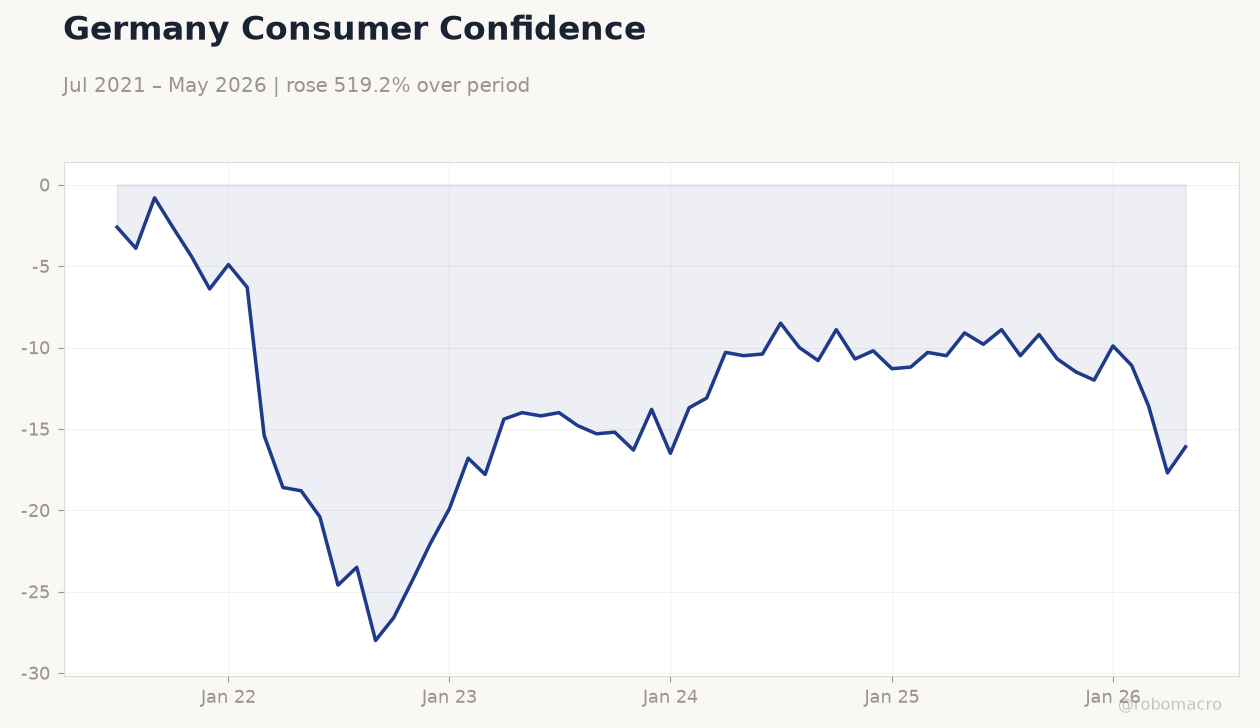

Germany Consumer Confidence | Type: macro_line | Consumer Sentiment Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

Germany Consumer Confidence | Type: macro_line | Consumer Sentiment Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Producer Price Index Year-over-Year | 1.70 | 2.50 | 22:00 |

| Friday (2026-06-19) | |||

| Producer Price Index Year-over-Year | 1.70 | 2.50 | 22:00 |

- German ZEW jumps to 10.5, beating consensus of -6

- Euro Stoxx 50 gains 0.68% while EUR/USD drops 0.73% to 1.15

- German 10-year Bund yield rises to 3.05%

Yesterday's Recap

German wholesale prices fell 0.6% month-over-month, missing the 0.8% consensus, while the year-over-year rate eased to 5.9%. Italian trade balance narrowed to 4.293 billion euros against expectations of 5.19 billion. German ZEW Economic Sentiment Index soared to 10.5, well above the -6 consensus forecast.

Dutch unemployment remained unchanged at 3.9%. Euro Stoxx 50 advanced 0.68% to 6,300.07 and DAX rose 0.08%, while CAC 40 slipped 0.20%. The German 10-year Bund yield increased 1.52% to 3.05%.

EUR/USD declined 0.73% to 1.15 and EUR/JPY fell 0.63%. The positive ZEW surprise contrasted with softer price data, supporting risk assets in equities while the euro weakened on mixed inflation signals. Bunds saw modest yield gains as markets digested the sentiment improvement without immediate policy implications.

The Day Ahead

Germany will release the producer price index year-over-year at 22:00 ET, with consensus at 2.5%. No other high-impact releases are scheduled across France, Italy, Spain or the Netherlands. Markets will assess whether the strong ZEW reading alters near-term inflation views.

Focus stays on any follow-through price action in Bunds and EUR crosses ahead of the weekend. Traders will monitor whether the PPI outcome reinforces or challenges the recent ZEW-driven optimism on growth prospects.

Other Economic Notes

France gained German backing for an EU proposal to impose US-style tariffs and quotas on Chinese imports to shield domestic industries. Germany and Poland signed a new defense agreement that shifts the European security balance. Banque de France cut its 2026 growth forecast to 0.5% and raised its inflation projection to 2.5%.

Eurozone unemployment remains at 6.70%. These developments highlight ongoing efforts to address external trade pressures and fiscal coordination within the bloc while domestic forecasts point to subdued expansion amid persistent price risks.

Global Macro News

G7 leaders pledged coordinated action on debt vulnerabilities in developing economies. Energy-price pass-through effects continued to influence euro-area inflation dynamics. Chinese export surges prompted fresh calls for faster EU trade safeguards at the Evian summit.

<i>↓ p.2</i>