Eurozone Macro Daily(Beta Mode)

German ZEW Surges, Bund Yields Rise

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,328.22 | +0.08% |

| DAX | 25,044.19 | +0.44% |

| CAC 40 | 8,487.54 | +0.23% |

| EUR/USD | 1.15 | -0.49% |

| EUR/GBP | 0.87 | +0.22% |

| EUR/JPY | 184.65 | -0.08% |

| Gold | 4,170.50 | -1.27% |

| Brent Crude | 80.17 | +0.40% |

| Bitcoin | 62,477.49 | -0.67% |

| German 2Y Bund | - | - |

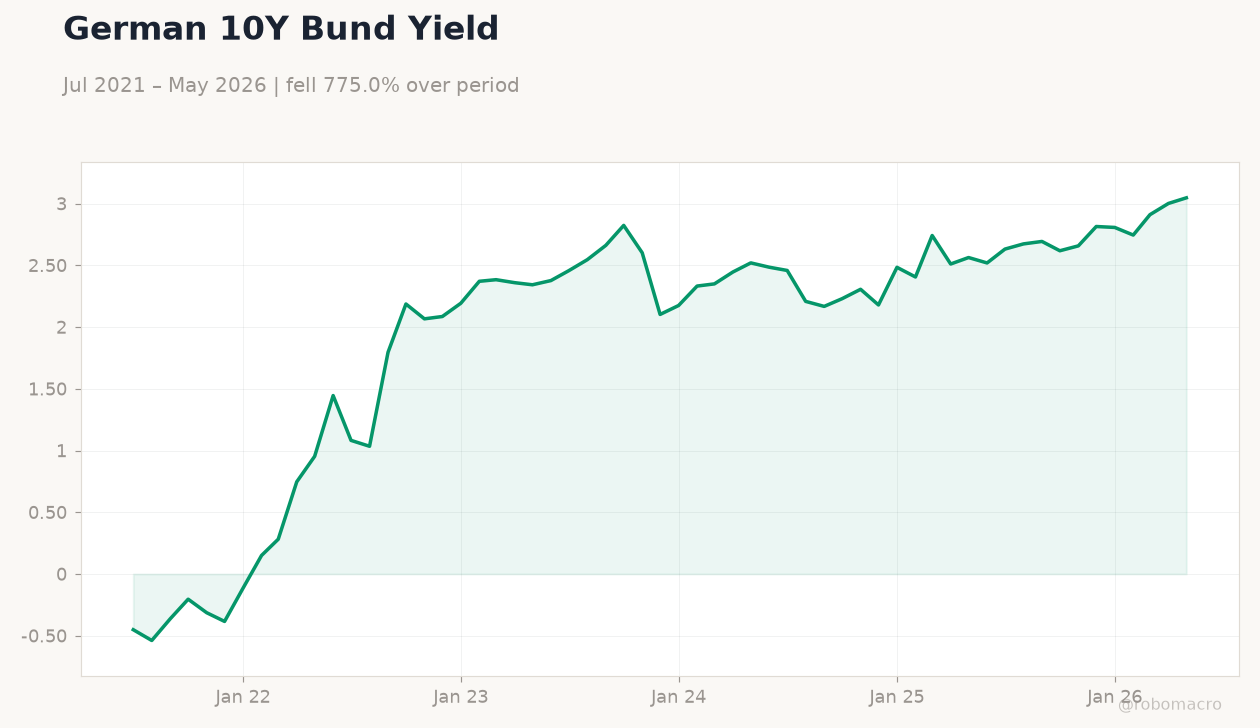

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Wholesale Prices Month-over-Month | 2 | 0.80 | -0.60 |

| Wholesale Prices Year-over-Year | 6.30 | - | 5.90 |

| Trade Balance | 4,813m | 5,190m | 4,293m |

| ZEW Economic Sentiment Index | -10.20 | -6 | 10.50 |

| Headline Unemployment Rate | 3.90 | - | 3.90 |

| Producer Price Index Year-over-Year | 1.70 | 2.50 | 2.20 |

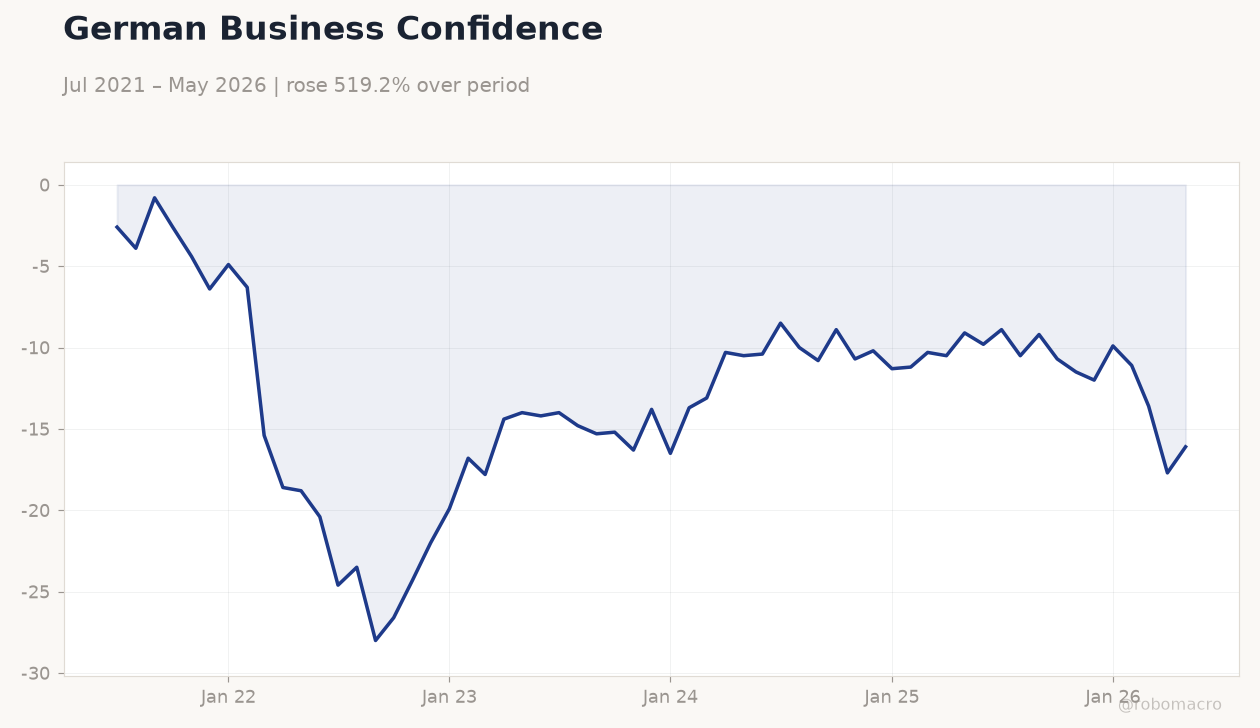

German Business Confidence | Type: macro_line | Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

German Business Confidence | Type: macro_line | Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- German ZEW Economic Sentiment jumped to 10.5, far above consensus of -6, signaling improved business expectations.

- Eurozone equities advanced modestly with DAX rising 0.44% while EUR/USD fell 0.49% to 1.15 amid higher German yields.

- Ifo cut its 2027 German growth forecast to 0.8% from 1.2%, citing persistent price pressures.

Yesterday's Recap

German wholesale prices fell 0.6% month-over-month in May against a 0.8% consensus, with the year-over-year rate easing to 5.9%. Italy’s trade balance narrowed to €4.293 billion versus an expected €5.19 billion. German ZEW sentiment surged to 10.5, reversing prior weakness and beating forecasts by a wide margin.

Dutch unemployment held steady at 3.9%. German producer prices rose 2.2% year-over-year, below the 2.5% consensus. Equity markets closed higher, with the DAX gaining 0.44% to 25,044.19 and the CAC 40 up 0.23%.

The 10-year Bund yield climbed 1.52% to 3.05%, pressuring EUR/USD lower to 1.15.

The Day Ahead

No high-impact Eurozone data releases are scheduled for 19 June. Markets will monitor any follow-through from the strong German ZEW print and assess implications for June flash HICP due next week. German and French business surveys may provide incremental color on sentiment.

ECB speakers remain quiet, leaving focus on incoming inflation prints. Traders will watch Bund auctions and any comments from national central bank officials for rate path signals. Thin calendars typically amplify moves from any surprise commentary.

Other Economic Notes

Evonik announced more than 2,000 job cuts in Germany as the chemicals sector faces prolonged weakness. Ifo’s downward revision to 2027 growth highlights risks from sticky prices and subdued domestic demand. Broader Eurozone unemployment remains at 6.70%, providing some labor-market support but offering little offset to softening growth expectations.

Corporate pension trends among DAX firms show continued emphasis on supplementary retirement schemes amid fiscal pressures.

Global Macro News

The US opened a tariff investigation into German pharmaceutical pricing, raising trade tension risks for exporters. The Swiss National Bank held rates steady while monitoring franc strength. <i>↓ p.2</i>