Eurozone Macro Daily(Beta Mode)

Bund Yields Rise on Iran Risks, ECB Hawkishness

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,293.13 | -0.48% |

| DAX | 25,044.19 | +0.44% |

| CAC 40 | 8,421.14 | -0.55% |

| EUR/USD | 1.15 | +0.00% |

| EUR/GBP | 0.87 | +0.32% |

| EUR/JPY | 185.19 | +0.20% |

| Gold | 4,210.20 | -0.33% |

| Brent Crude | 79.03 | -1.03% |

| Bitcoin | 64,180.34 | -0.09% |

| German 2Y Bund | - | - |

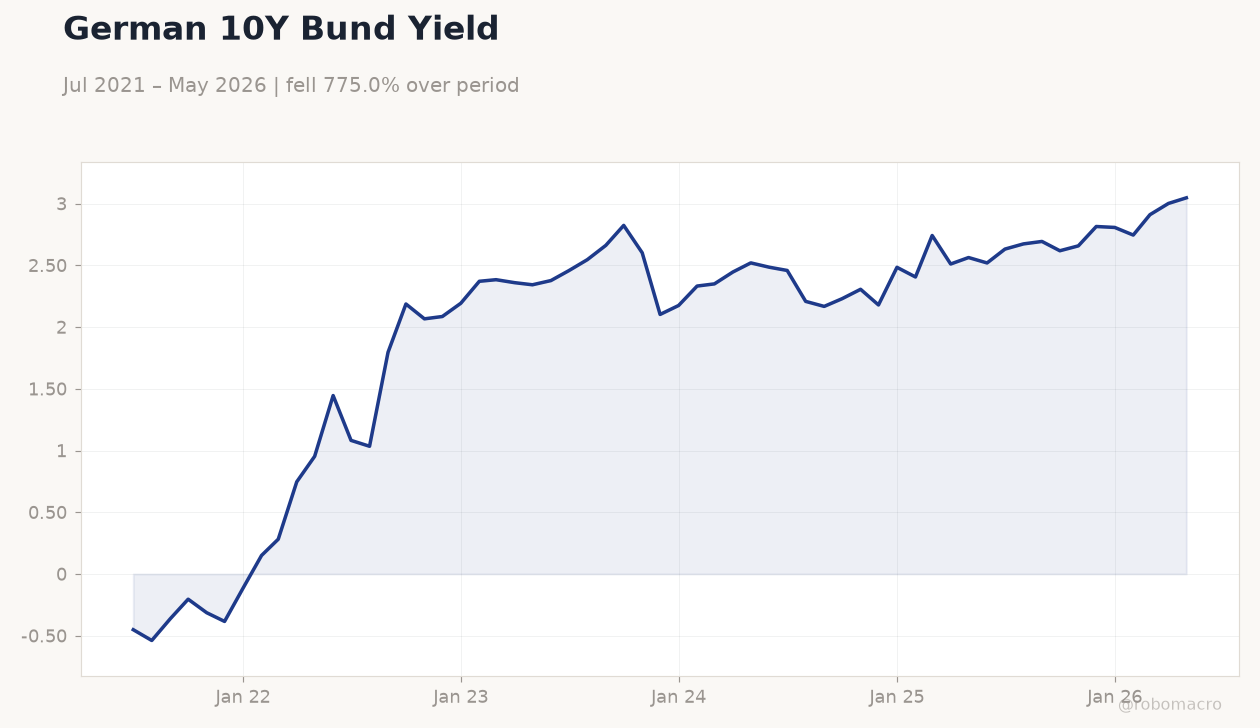

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

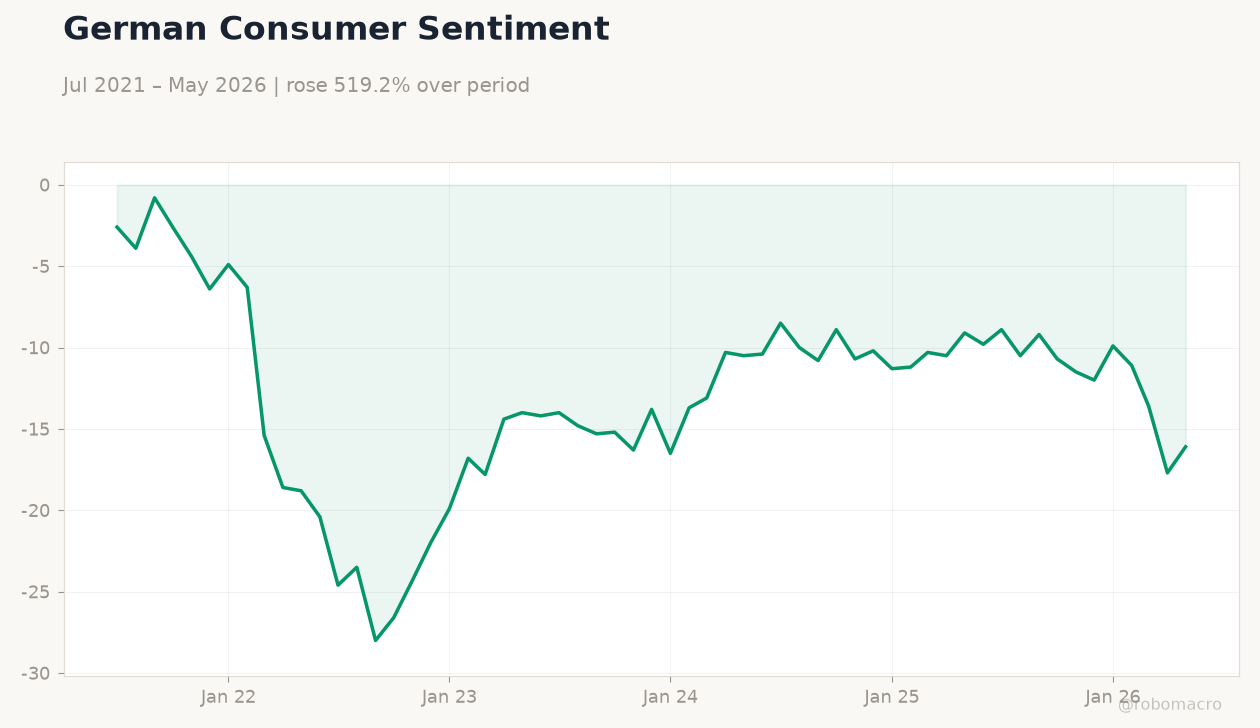

| Consumer Confidence Index | -46 | - | -39 |

German 10Y Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,3.046

German 10Y Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,3.046

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 102 | - | 22:45 |

| S&P Global Composite PMI Flash | 44.90 | - | 23:15 |

| S&P Global Manufacturing PMI Flash | 49.70 | 50.40 | 23:15 |

| S&P Global Services PMI Flash | 44.30 | 45.90 | 23:15 |

| S&P Global Manufacturing PMI Flash | 50.10 | 50 | 23:30 |

| S&P Global Composite PMI Flash | 48.80 | - | 23:30 |

| S&P Global Services PMI Flash | 48.10 | 48.70 | 23:30 |

| Trade Balance | -4,400m | - | 00:00 |

| Ifo Business Climate | 84.90 | 85.60 | 00:00 |

| GFK Consumer Confidence Index | -29.80 | -28 | 22:00 |

- Dutch consumer confidence improved sharply to -39.0 in June from -46.0 prior, signalling modest household resilience.

- German 10-year Bund yields climbed 1.52% to 3.05% as markets priced reduced ECB easing odds.

- French and German flash PMIs due today will test whether the modest euro-area recovery is broadening beyond Germany.

Yesterday's Recap

Netherlands June consumer confidence rose to -39.0, beating the prior -46.0 reading and marking the strongest print since late 2024. Euro Stoxx 50 fell 0.48% to 6,293.13 while the DAX gained 0.44% to 25,044.19 and the CAC 40 slipped 0.55% to 8,421.14. German 10-year Bund yields increased 1.52% to 3.05% amid thin holiday-thinned trading.

EUR/USD held steady at 1.15, EUR/GBP rose 0.32% to 0.87 and EUR/GBP advanced 0.20% to 185.19. Brent crude declined 1.03% to $79.03 per barrel and gold eased 0.33% to $4,210.20. No ECB speakers appeared and markets took the isolated Dutch data release as neutral for near-term policy pricing.

The Day Ahead

France will release June business confidence and S&P Global flash PMIs for manufacturing, services and composite at 22:45-23:15 ET, with consensus pointing to modest rebounds in manufacturing and services. Germany follows at 23:30 ET with its own S&P Global manufacturing, services and composite flashes, led by the high-impact manufacturing print. Spain reports its May trade balance at midnight ET.

Wednesday brings the closely watched German Ifo business climate and GfK consumer confidence prints, both expected to edge higher. Italian business and consumer confidence figures close the week on Thursday.

Other Economic Notes

Bundesbank analysis shows Germany’s potential growth is increasingly constrained by demographic shrinkage and slower labour-force expansion. Producer prices are rising again after the expiry of fuel subsidies, threatening to push headline inflation above 3% later this year. German goods exports recorded their first annual increase in three years in 2025, supported by stronger demand from non-euro markets.

Solar generation has already saved Germany €20 billion in energy import costs since 2020, reducing external vulnerability. US authorities have opened a trade investigation into German pharmaceutical pricing, raising the risk of new tariffs on a key export sector.