Eurozone Macro Daily(Beta Mode)

Dutch Confidence Beats as PMIs Loom

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,248.79 | -0.99% |

| DAX | 25,044.19 | +0.44% |

| CAC 40 | 8,335.65 | -0.77% |

| EUR/USD | 1.14 | -0.20% |

| EUR/GBP | 0.86 | -0.52% |

| EUR/JPY | 184.65 | -0.21% |

| Gold | 4,131.40 | -1.21% |

| Brent Crude | 76.70 | -1.54% |

| Bitcoin | 62,972.85 | -1.53% |

| German 2Y Bund | - | - |

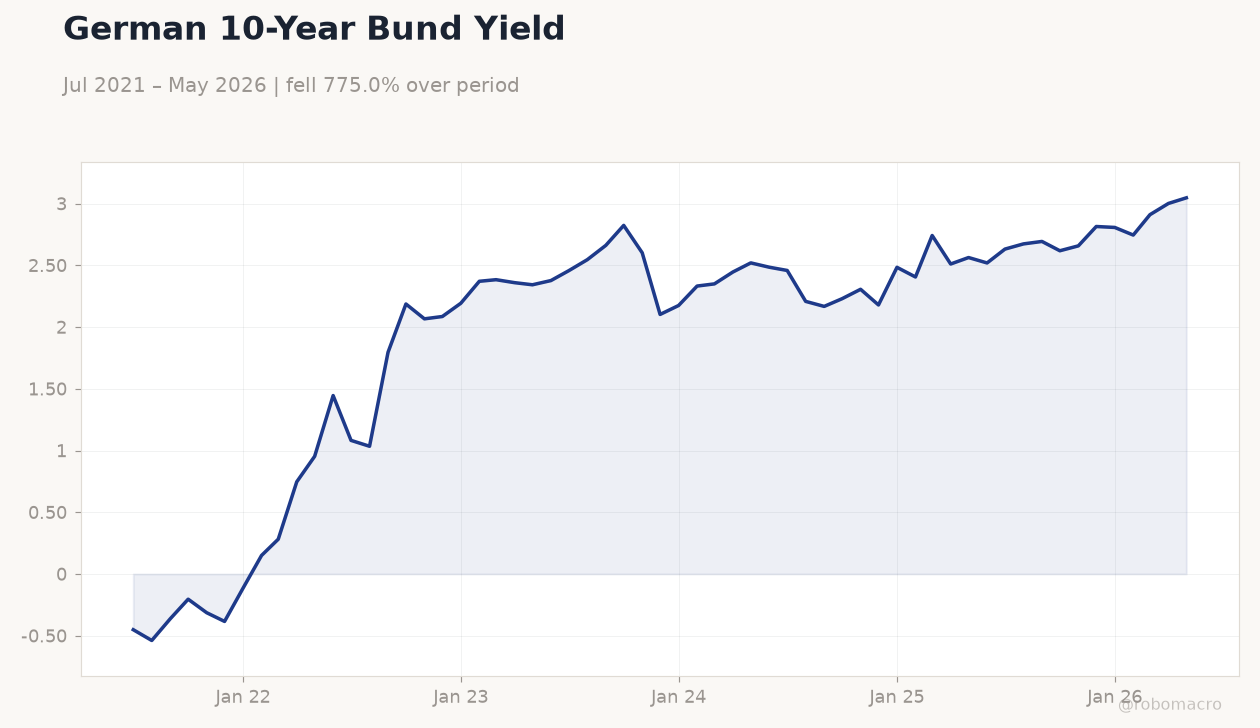

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

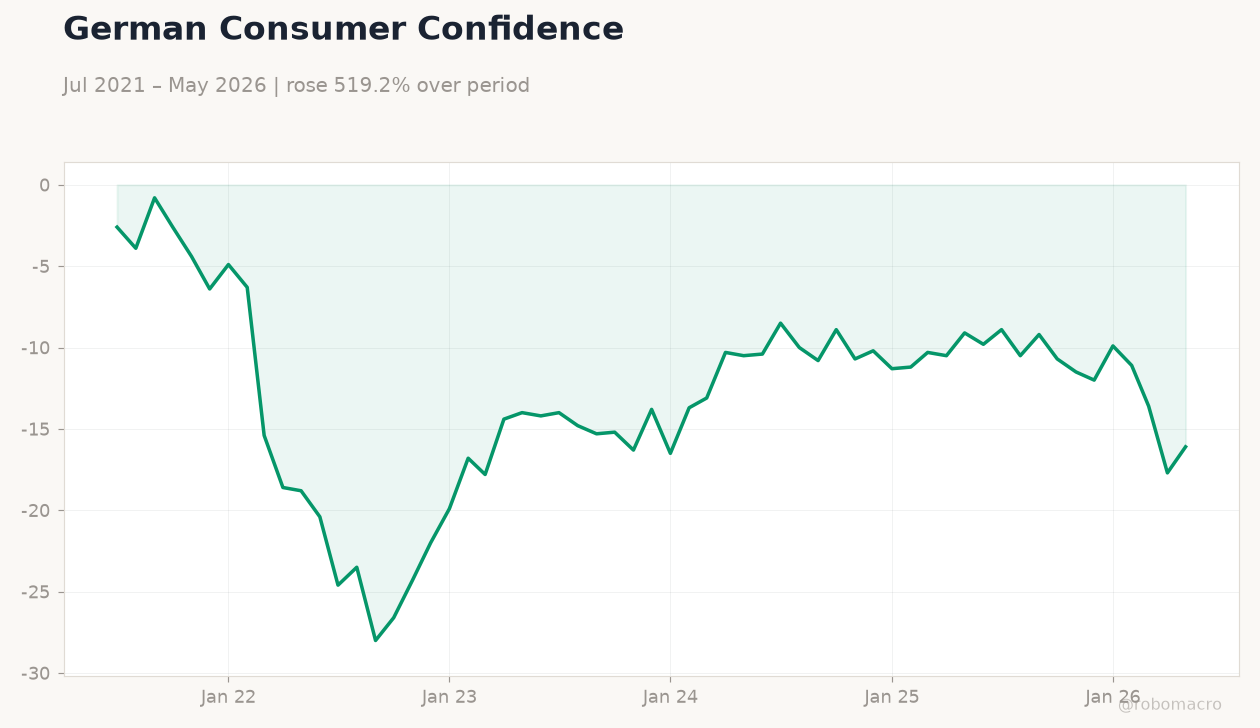

| Consumer Confidence Index | -46 | - | -39 |

German 10-Year Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,3.046

German 10-Year Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,3.046

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 102 | 101 | 22:45 |

| S&P Global Composite PMI Flash | 44.90 | 46 | 23:15 |

| S&P Global Manufacturing PMI Flash | 49.70 | 50 | 23:15 |

| S&P Global Services PMI Flash | 44.30 | 45.50 | 23:15 |

| S&P Global Manufacturing PMI Flash | 50.10 | 50.50 | 23:30 |

| S&P Global Composite PMI Flash | 48.80 | 49.90 | 23:30 |

| S&P Global Services PMI Flash | 48.10 | 49 | 23:30 |

| Trade Balance | -4,400m | - | 00:00 |

| Ifo Business Climate | 84.90 | 85.60 | 00:00 |

| GFK Consumer Confidence Index | -29.80 | -28 | 22:00 |

- Netherlands consumer confidence improved sharply to -39.0 in June, signalling reduced household pessimism.

- French and German flash PMIs due today, with markets expecting modest rebounds in services and manufacturing.

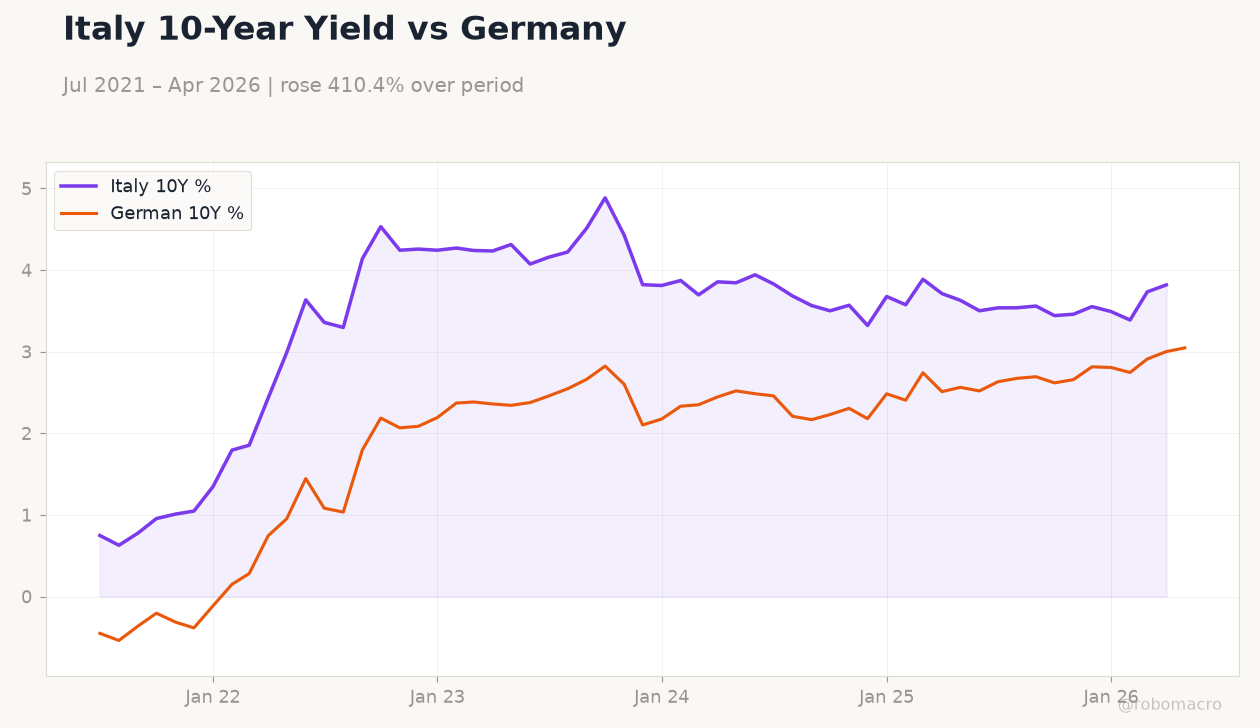

- German 10-year Bund yields rose 1.52% to 3.05% while Euro Stoxx 50 fell 0.99% amid mixed equity moves.

Yesterday's Recap

Dutch consumer confidence rose to -39.0 from -46.0, marking the strongest reading in several months and reflecting easing concerns over energy costs. No other high-impact Eurozone releases occurred on 22 June. Euro Stoxx 50 declined 0.99% to 6,248.79 while the DAX gained 0.44% to 25,044.19, highlighting divergent national equity performance.

The CAC 40 fell 0.77%. EUR/USD slipped 0.20% to 1.14 and EUR/GBP dropped 0.52% to 0.86. German 10-year Bund yields increased 1.52% to 3.05%, pushing swap markets to price fewer ECB cuts by year-end.

Brent crude fell 1.54% to 76.70, reducing imported inflation risks for the bloc.

The Day Ahead

French business confidence and S&P Global flash PMIs for manufacturing, services and composite are scheduled for release this evening, with consensus pointing to small gains from May levels. German manufacturing and composite PMIs follow shortly after, expected to show continued expansion above 50. Spain will publish its May trade balance, while the German Ifo Business Climate index and GfK consumer confidence are set for 24 June.

The ECB Bank Lending Survey is also due, offering fresh insight into credit conditions across member states. No Governing Council speeches are listed.

Other Economic Notes

Germany’s planned increase in its stake in defence group KNDS to 40% underscores deeper Franco-German industrial cooperation ahead of the firm’s expected IPO. RWE’s 4.75 billion euro capital raise to enlarge its Amprion stake highlights ongoing grid investment needs amid the energy transition. Broader euro-area unemployment remains at 6.70%, supporting the view that labour markets have stabilised despite subdued growth.

EU finance ministers continue technical work on expanding the ESM firewall without immediate market implications.