Eurozone Macro Daily(Beta Mode)

Divergent PMI Prints Pressure Eurozone Assets

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,230.55 | -1.28% |

| DAX | 25,044.19 | +0.44% |

| CAC 40 | 8,340.71 | -0.71% |

| EUR/USD | 1.14 | -0.51% |

| EUR/GBP | 0.86 | -0.13% |

| EUR/JPY | 183.72 | -0.49% |

| Gold | 4,106.80 | -0.56% |

| Brent Crude | 76.41 | -0.87% |

| Bitcoin | 62,782.36 | +0.18% |

| German 2Y Bund | - | - |

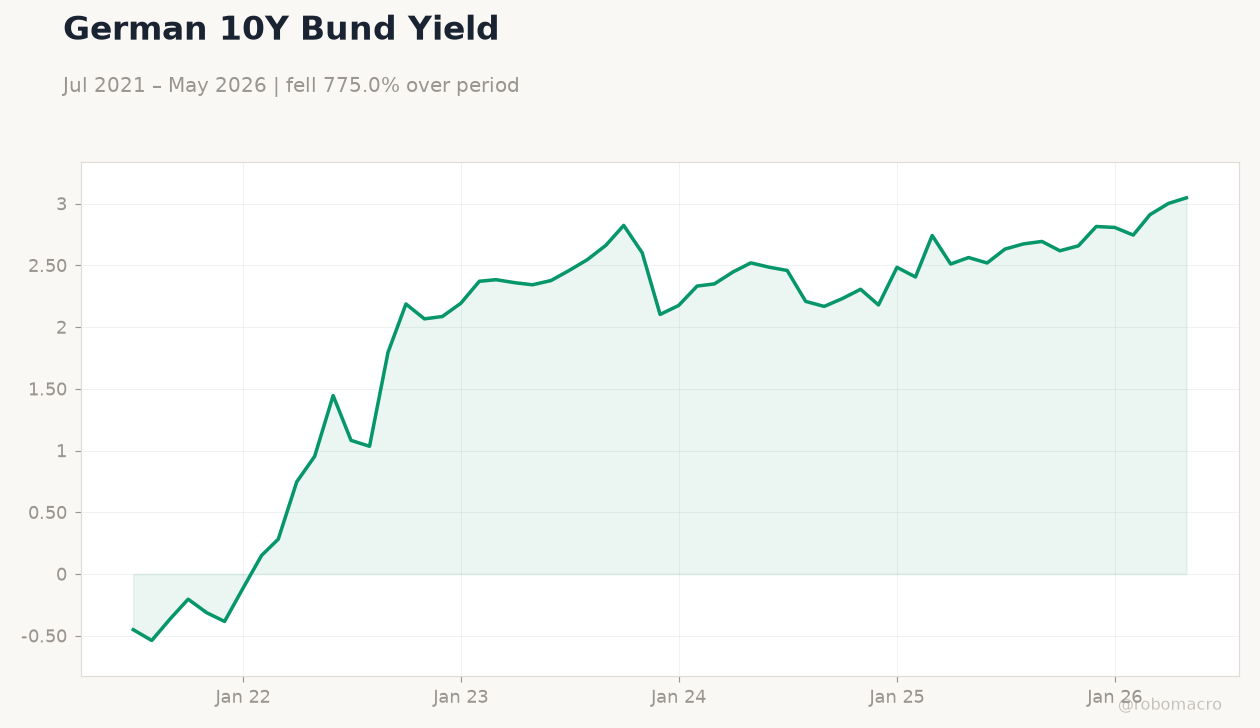

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

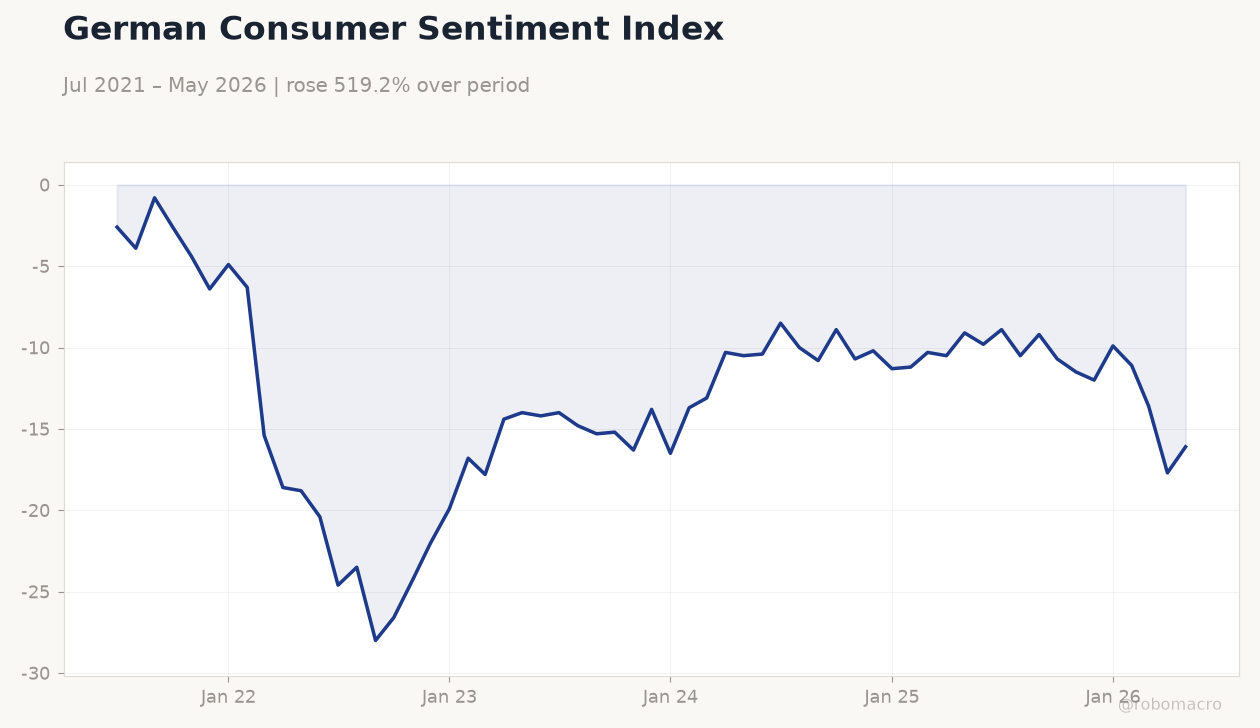

| Consumer Confidence Index | -46 | - | -39 |

| Business Confidence Index | 102 | 101 | 100 |

| S&P Global Composite PMI Flash | 44.90 | 46 | 47.60 |

| S&P Global Manufacturing PMI Flash | 49.70 | 50 | 50.70 |

| S&P Global Services PMI Flash | 44.30 | 45.50 | 47.40 |

| S&P Global Manufacturing PMI Flash | 50.10 | 50.50 | 50 |

| S&P Global Composite PMI Flash | 48.80 | 49.90 | 48 |

| S&P Global Services PMI Flash | 48.10 | 49 | 46.80 |

| Trade Balance | -4,400m | - | -5,200m |

German Consumer Sentiment Index | Type: macro_line | Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

German Consumer Sentiment Index | Type: macro_line | Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Ifo Business Climate | 84.90 | 85.60 | 00:00 |

| GFK Consumer Confidence Index | -29.80 | -27.50 | 22:00 |

| Consumer Confidence Index | 82 | 84 | 22:45 |

| Business Confidence Index | 87.90 | - | 01:00 |

| Consumer Confidence Index | 93.40 | - | 01:00 |

| Unemployment Benefit Claims | -9,000 | - | 02:00 |

- French S&P Global Composite PMI rose to 47.6 in June flash, beating consensus of 46.0, while German Composite fell to 48.0 versus 49.9 expected.

- Euro Stoxx 50 declined 1.28% to 6,230.55 and EUR/USD dropped 0.51% to 1.14 amid mixed regional data.

- German 10-year Bund yield climbed 1.52% to 3.05% as ECB Deposit Rate held at 2.25%.

Yesterday's Recap

French business confidence slipped to 100 from 102, yet S&P Global Manufacturing PMI climbed to 50.7 and Services PMI jumped to 47.4, both exceeding forecasts. German Manufacturing PMI edged down to 50.0 against 50.5 consensus while Composite PMI fell to 48.0 and Services PMI dropped to 46.8. Netherlands Consumer Confidence improved to -39.0 from -46.0.

Spain posted a wider trade deficit of EUR 5.2 billion. Euro Stoxx 50 and CAC 40 fell while DAX rose 0.44%; EUR crosses weakened across the board and Brent Crude declined 0.87% to 76.41. German 10-year Bund yields rose as markets digested the divergent PMI prints.

The Day Ahead

German Ifo Business Climate is due at 00:00 ET with consensus at 85.6 after 84.9 previously. GFK Consumer Confidence follows at 22:00 ET, expected to improve to -27.5 from -29.8. French Consumer Confidence is forecast at 84 versus 82 prior.

Italian Business and Consumer Confidence indices print at 01:00 ET. French Unemployment Benefit Claims close the session at 02:00 ET. Markets will focus on the Ifo print for fresh signals on German momentum.

Other Economic Notes

Germany is advancing plans to raise the retirement age beyond 67 and expand compulsory pension contributions to address long-term fiscal pressures. Occupational pension schemes among DAX and MDAX firms show varying employer contributions, with larger groups offering more generous top-ups. Eurozone unemployment stands at 6.70%, providing a stable backdrop but limited wage pressure.

Broader fiscal discussions among EU ministers signal modest loosening in the next MFF envelope for 2027-28.

Global Macro News

An ECB official noted that Middle East tensions are weighing on eurozone growth while adding upside risks to inflation. UK post-Brexit political churn continues to draw European media attention, with London retaining dominance as a financial centre despite regulatory shifts. CATL’s launch of a sodium-ion battery storage system in Munich highlights European supply-chain diversification efforts.

<i>↓ p.2</i>