Eurozone Macro Daily(Beta Mode)

French PMIs Beat as German Ifo Holds

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,241.85 | +0.44% |

| DAX | 24,824.50 | +0.34% |

| CAC 40 | 8,386.30 | +0.01% |

| EUR/USD | 1.14 | -0.20% |

| EUR/GBP | 0.86 | -0.06% |

| EUR/JPY | 183.88 | -0.40% |

| Gold | 4,000.50 | +0.26% |

| Brent Crude | 72.98 | -1.03% |

| Bitcoin | 61,716.50 | +1.18% |

| German 2Y Bund | - | - |

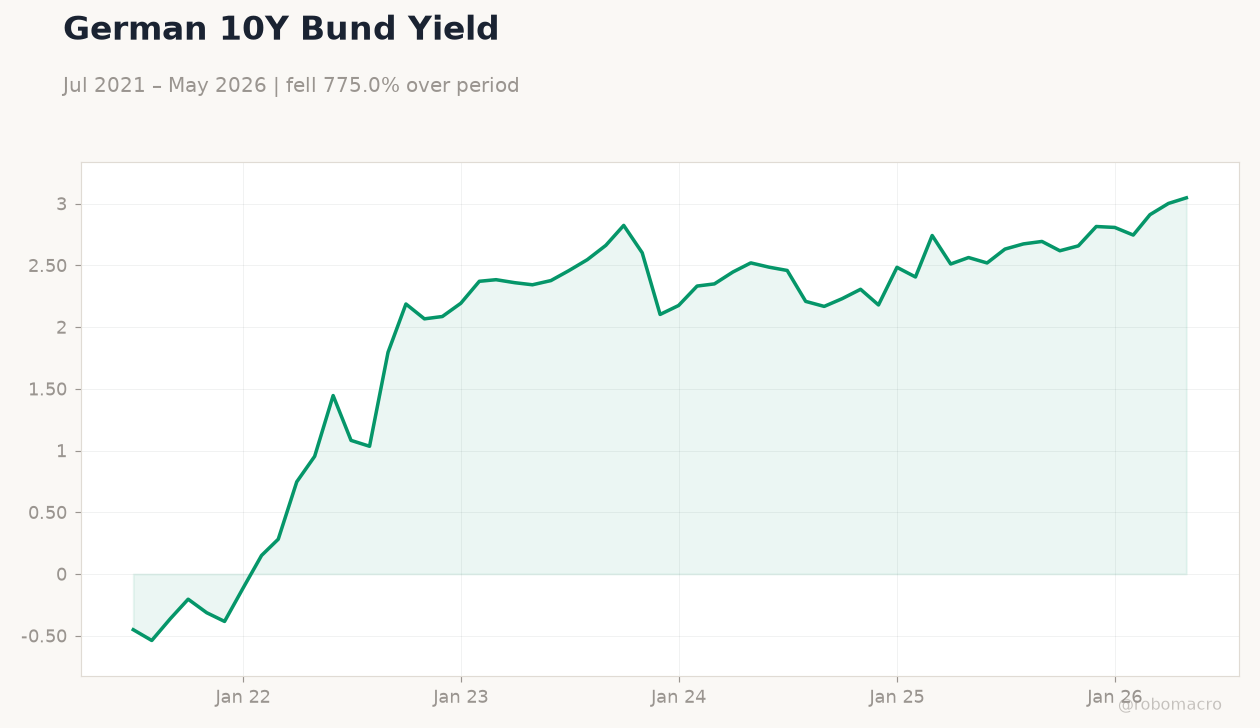

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | -46 | - | -39 |

| Business Confidence Index | 102 | 101 | 100 |

| S&P Global Composite PMI Flash | 44.90 | 46 | 47.60 |

| S&P Global Manufacturing PMI Flash | 49.70 | 50 | 50.70 |

| S&P Global Services PMI Flash | 44.30 | 45.50 | 47.40 |

| S&P Global Manufacturing PMI Flash | 50.10 | 50.50 | 50 |

| S&P Global Composite PMI Flash | 48.80 | 49.90 | 48 |

| S&P Global Services PMI Flash | 48.10 | 49 | 46.80 |

| Trade Balance | -4,400m | - | -5,200m |

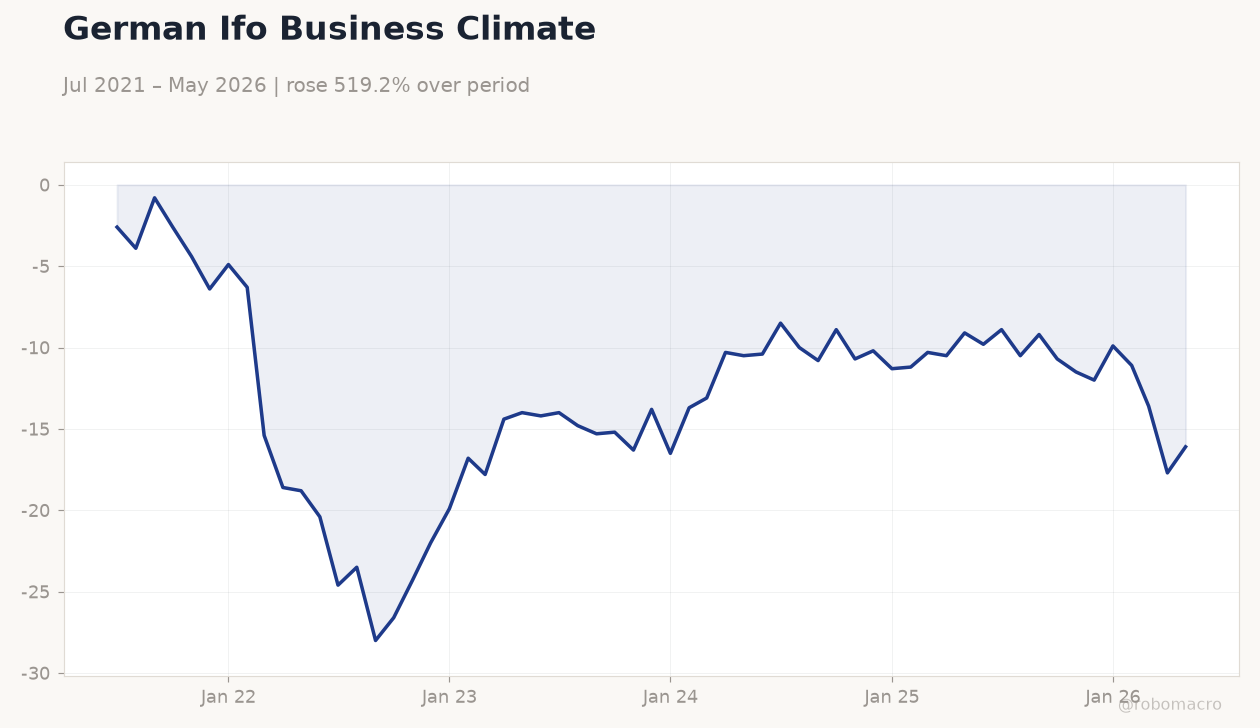

| Ifo Business Climate | 85 | 85.60 | 85.60 |

German Ifo Business Climate | Type: macro_line | Business Climate Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

German Ifo Business Climate | Type: macro_line | Business Climate Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Consumer Confidence Index | 82 | 84 | 22:45 |

| Business Confidence Index | 87.90 | - | 01:00 |

| Consumer Confidence Index | 93.40 | - | 01:00 |

| Unemployment Benefit Claims | -9,000 | - | 02:00 |

- French S&P Global Composite PMI rose to 47.6, beating consensus of 46

- German Ifo Business Climate matched consensus at 85.6 while GfK consumer confidence improved to -29.2

- Euro Stoxx 50 gained 0.44% and DAX rose 0.34% as EUR/USD fell 0.20% to 1.14

Yesterday's Recap

French S&P Global Manufacturing PMI climbed to 50.7 and Services PMI reached 47.4, both exceeding forecasts and lifting the Composite reading. German Manufacturing PMI slipped to 50.0 while Composite and Services readings fell to 48.0 and 46.8, missing expectations. The Netherlands Consumer Confidence Index improved to -39.0 from -46.0.

Germany’s Ifo Business Climate rose to 85.6, meeting the consensus, and GfK Consumer Confidence came in at -29.2. Spain’s Trade Balance widened to -5.2 billion euros. Euro Stoxx 50 and DAX posted modest gains while the German 10-year Bund yield climbed 1.52% to 3.05%.

EUR crosses weakened across the board. French business confidence edged down to 100 from 102 while the Netherlands data showed clear improvement.

The Day Ahead

France will release its Consumer Confidence Index and Unemployment Benefit Claims data. Italy is scheduled to publish Business and Consumer Confidence readings. Markets will monitor any follow-through from yesterday’s French PMI strength and German Ifo stability.

The releases may influence short-term Bund yield movements and EUR crosses. No major ECB speakers are listed for today.

Other Economic Notes

Eurozone unemployment stands at 6.70%. The ECB Deposit Rate remains at 2.25%. Recent data show divergent momentum between France and Germany, with services activity improving in France while German readings softened.

Broader fiscal and structural themes, including pension reform discussions in Germany, continue to shape medium-term growth expectations without immediate market impact. Heat-driven energy demand added mild upward pressure on inflation risks in southern member states.

Global Macro News

ECB staff noted that an Iran-related energy shock could reduce Eurozone growth by 0.4%. ECB’s Schnabel stated that further rate hikes may still be required to reach the 2% inflation target. EU lawmakers approved draft rules advancing the digital euro project.

<i>↓ p.2</i>