Eurozone Macro Daily(Beta Mode)

French PMI Beat Offsets Soft German Data

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,241.63 | -0.41% |

| DAX | 24,740.36 | -0.62% |

| CAC 40 | 8,400.44 | -0.37% |

| EUR/USD | 1.14 | +0.31% |

| EUR/GBP | 0.86 | +0.05% |

| EUR/JPY | 184.00 | +0.18% |

| Gold | 4,043.40 | +0.32% |

| Brent Crude | 73.61 | -2.19% |

| Bitcoin | 60,329.74 | +1.02% |

| German 2Y Bund | - | - |

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Consumer Confidence Index | -46 | - | -39 |

| Business Confidence Index | 102 | 101 | 100 |

| S&P Global Composite PMI Flash | 44.90 | 46 | 47.60 |

| S&P Global Manufacturing PMI Flash | 49.70 | 50 | 50.70 |

| S&P Global Services PMI Flash | 44.30 | 45.50 | 47.40 |

| S&P Global Manufacturing PMI Flash | 50.10 | 50.50 | 50 |

| S&P Global Composite PMI Flash | 48.80 | 49.90 | 48 |

| S&P Global Services PMI Flash | 48.10 | 49 | 46.80 |

| Trade Balance | -4,400m | - | -5,200m |

| Ifo Business Climate | 85 | 85.60 | 85.60 |

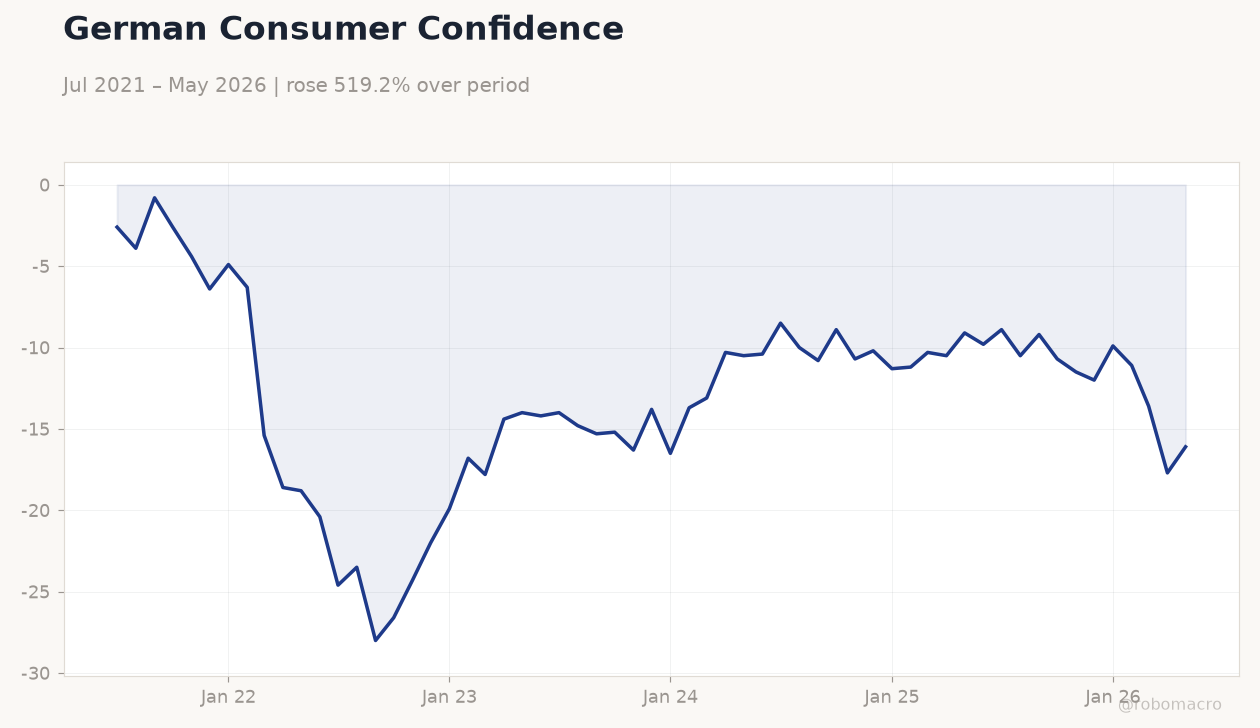

German Consumer Confidence | Type: macro_line | Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

German Consumer Confidence | Type: macro_line | Index: -16.1 (2026-05-01) | Range: -28–-0.8 | Trend(6pt): -2.6,-28,-16.3,-11.3,-13.6,-16.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Business Confidence Index | 87.90 | 88.40 | 01:00 |

| Consumer Confidence Index | 93.40 | 94.50 | 01:00 |

| Unemployment Benefit Claims | -9,000 | - | 02:00 |

- French S&P Global Composite PMI rose to 47.6 in June, beating consensus of 46.0, while German manufacturing PMI edged down to 50.0.

- German Ifo Business Climate held at 85.6, matching expectations, though GfK consumer confidence improved modestly to -29.2.

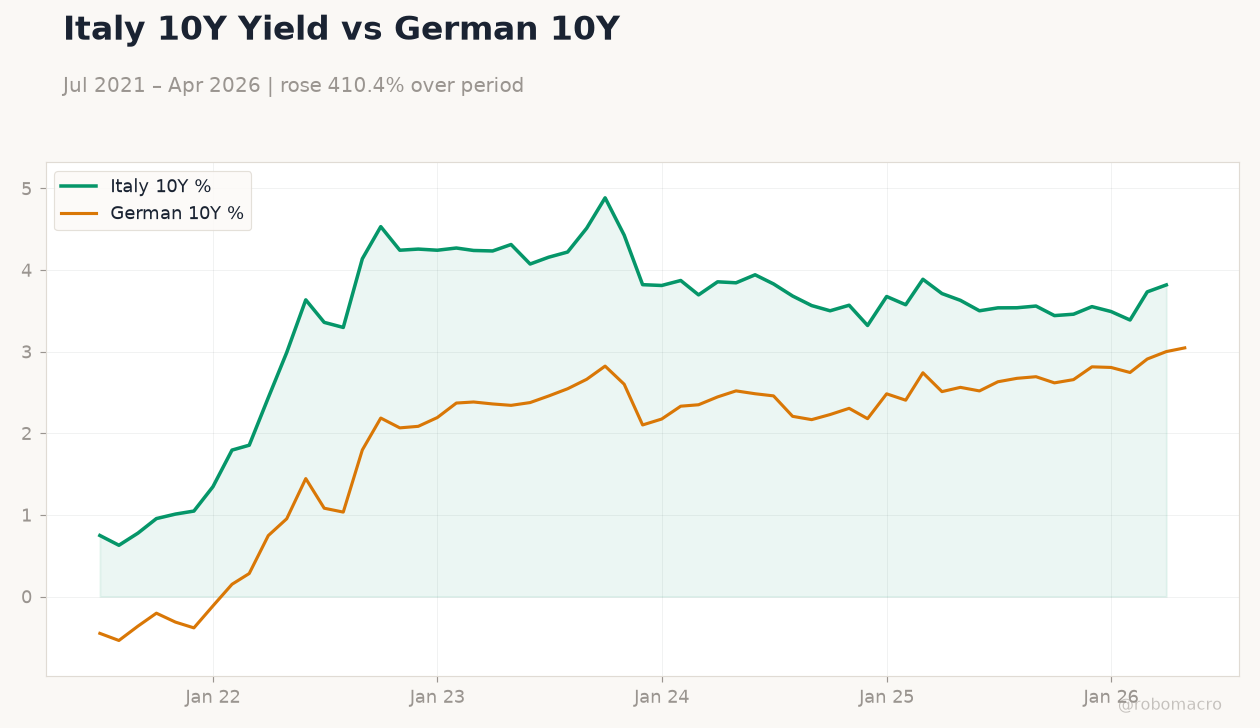

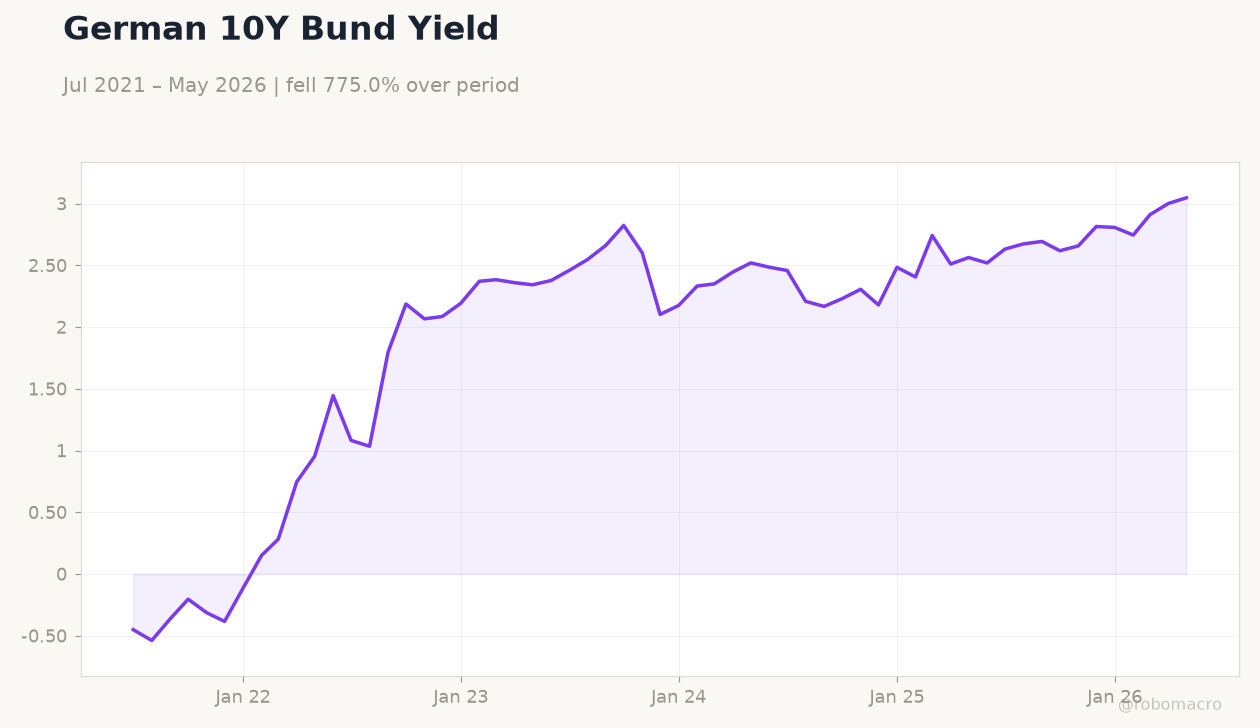

- Euro Stoxx 50 fell 0.41% to 6,241.63 and DAX declined 0.62%, while the 10-year Bund yield climbed 1.52% to 3.05%.

Yesterday's Recap

French business confidence slipped to 100 from 102, yet the S&P Global Composite PMI jumped to 47.6, manufacturing PMI reached 50.7 and services PMI climbed to 47.4, all exceeding forecasts. German manufacturing PMI printed at 50.0 versus 50.5 expected and composite PMI fell to 48.0, while the Ifo Business Climate matched consensus at 85.6. Spanish trade balance widened to -€5.2 billion and Dutch consumer confidence improved to -39.0.

Equities closed lower across the board with Euro Stoxx 50 at 6,241.63 and DAX at 24,740.36. EUR/USD advanced 0.31% to 1.14 while Brent crude dropped 2.19% to $73.61. The German 10-year Bund yield rose to 3.05%.

No ECB speakers appeared in the calendar.

The Day Ahead

Italy releases business and consumer confidence indices at 01:00 ET, with markets watching for any further softening after recent German weakness. France reports unemployment benefit claims at 02:00 ET, providing an early read on labor-market momentum. The releases arrive ahead of month-end positioning and could influence short-term Bund and equity flows.

No major speeches from Governing Council members are scheduled. Traders will also monitor any follow-through from yesterday’s French PMI strength.

Other Economic Notes

Germany’s supplementary pension offerings at leading DAX and MDAX firms remain a focal point for labor-cost discussions ahead of potential retirement-age adjustments. France’s finance minister reaffirmed the 5% deficit target despite watchdog criticism, keeping sovereign-spread volatility contained. Broader euro-area fiscal flexibility talks among EU ministers produced a mildly dovish tone for high-debt periphery bonds.

Energy-transition investment momentum continued at The smarter E Europe exhibition in Munich.

Global Macro News

UK output remains 2-4% below its pre-Brexit trajectory, weighing on euro-area export demand. US-Iran tensions easing reduced oil-price pressure, supporting euro-area disinflation hopes. <i>↓ p.2</i>