Eurozone Macro Daily(Beta Mode)

Inflation Data to Test ECB Rate Path

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,236.08 | +0.23% |

| DAX | 24,994.83 | +1.03% |

| CAC 40 | 8,376.16 | -0.10% |

| EUR/USD | 1.14 | +0.39% |

| EUR/GBP | 0.86 | +0.17% |

| EUR/JPY | 184.50 | +0.37% |

| Gold | 4,077.70 | -0.02% |

| Brent Crude | 72.94 | +1.32% |

| Bitcoin | 59,949.76 | +0.70% |

| German 2Y Bund | - | - |

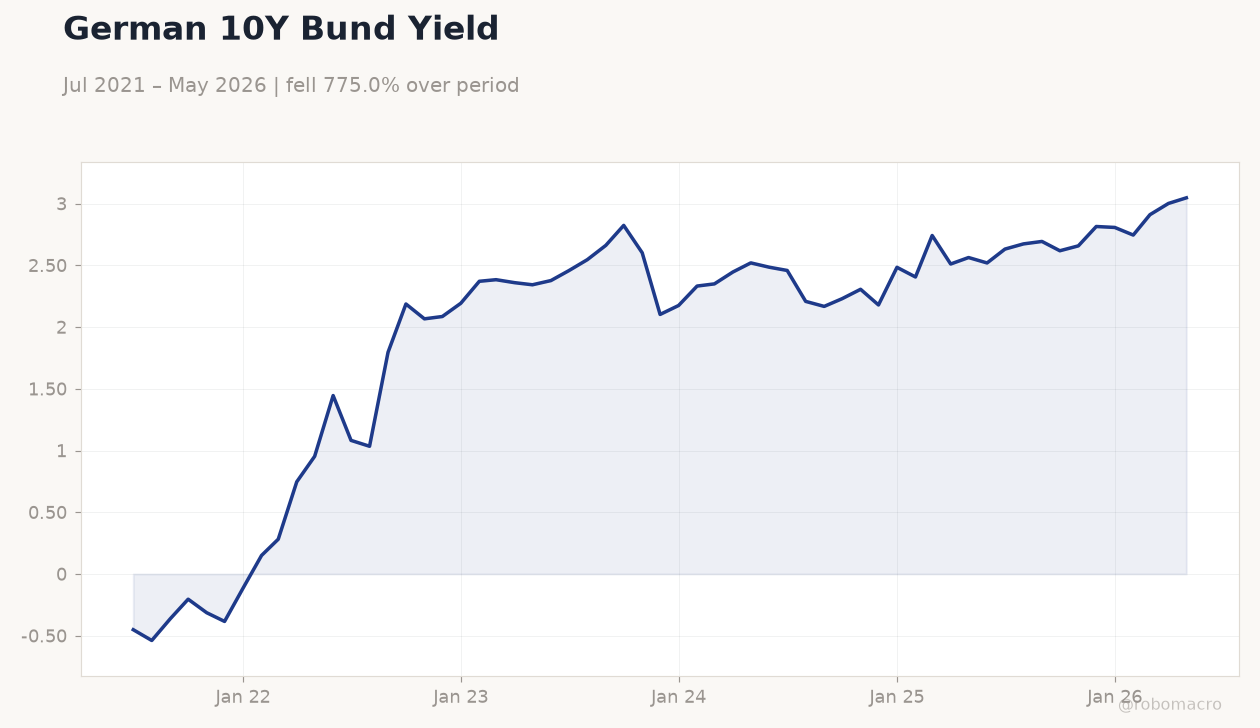

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

German 10Y Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,3.046

German 10Y Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.4514,1.795,2.601,2.484,2.91,3.046

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Inflation Rate Month-over-Month Preliminary | 0.10 | - | 23:00 |

| Inflation Rate Year-over-Year Preliminary | 3.20 | 3.20 | 23:00 |

| Business Confidence Index | -3.70 | - | 02:00 |

| Retail Sales Month-over-Month | -0.30 | 0 | 22:00 |

| Retail Sales Year-over-Year | -0.30 | 0 | 22:00 |

| Inflation Rate Year-over-Year Preliminary | 2.40 | - | 22:45 |

| Inflation Rate Month-over-Month Preliminary | 0.10 | 0 | 22:45 |

| Headline Unemployment Rate | 6.30 | 6.40 | 23:55 |

| Unemployed Persons Level | 3.0m | - | 23:55 |

| Unemployment Level Change | -12,000 | 8,000 | 23:55 |

- German and French June inflation prints due today will test ECB 2.25% deposit rate path

- DAX rises 1.03% while Euro Stoxx 50 gains 0.23% on firmer sentiment

- EUR/USD advances 0.39% to 1.14 amid mixed European equity moves

Yesterday's Recap

Equity markets showed modest gains with the DAX climbing 1.03% to 24,994.83 and Euro Stoxx 50 adding 0.23% to 6,236.08, while CAC 40 slipped 0.10% to 8,376.16. EUR/USD rose 0.39% to 1.14 and EUR/JPY gained 0.37% to 184.50. German 10-year Bund yields increased 1.52% to 3.05%.

No Eurozone data releases occurred on 28 June. News highlighted German industry relocation risks and heatwave effects on economic activity in Germany and France. Brent crude rose 1.32% to 72.94, supporting energy-sensitive sectors.

Bitcoin gained 0.70% to 59,949.76.

The Day Ahead

Spanish June inflation rate year-over-year preliminary is expected at 3.2% alongside month-over-month figures. German retail sales month-over-month consensus stands at 0% after a prior -0.3% print. French June inflation year-over-year preliminary follows the prior 2.4% reading.

German headline unemployment rate is forecast at 6.4% versus 6.3% previously. Italian June inflation year-over-year preliminary and German June inflation year-over-year preliminary at 2.5% consensus complete the high-impact releases. Markets will parse these prints for implications on the 2.25% ECB deposit rate trajectory.

Other Economic Notes

German companies signal further job cuts despite improving Ifo sentiment, with surveys indicating up to 100,000 positions at risk from relocation abroad. Heatwaves across Germany and France threaten productivity and raise excess death counts, adding downside risks to Q3 growth. EU finance ministers extended fiscal rule suspension to end-2026, easing near-term austerity pressure on member states.

German carmakers prepare additional cutbacks following Volkswagen’s earlier 50,000-job plan. Labor market data show persistent caution among firms even as business confidence edges higher.

Global Macro News

OPEC+ supply discipline lifted Brent crude 1.32%, supporting euro-area energy importers. US-Canada-Mexico coordination on trade and migration indirectly affects euro cross rates via dollar strength. South Korea and Swiss CPI releases scheduled alongside eurozone prints will shape global rate expectations.

<i>↓ p.2</i>