Eurozone Macro Daily(Beta Mode)

Eurozone Inflation Eases to 2.8%, DAX Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Euro Stoxx 50 | 6,287.45 | +0.08% |

| DAX | 24,995.81 | +1.50% |

| CAC 40 | 8,374.38 | +0.44% |

| EUR/USD | 1.14 | -0.05% |

| EUR/GBP | 0.86 | -0.70% |

| EUR/JPY | 184.12 | -0.80% |

| Gold | 4,084.40 | +0.40% |

| Brent Crude | 71.03 | -0.75% |

| Bitcoin | 60,099.33 | +0.16% |

| German 2Y Bund | - | - |

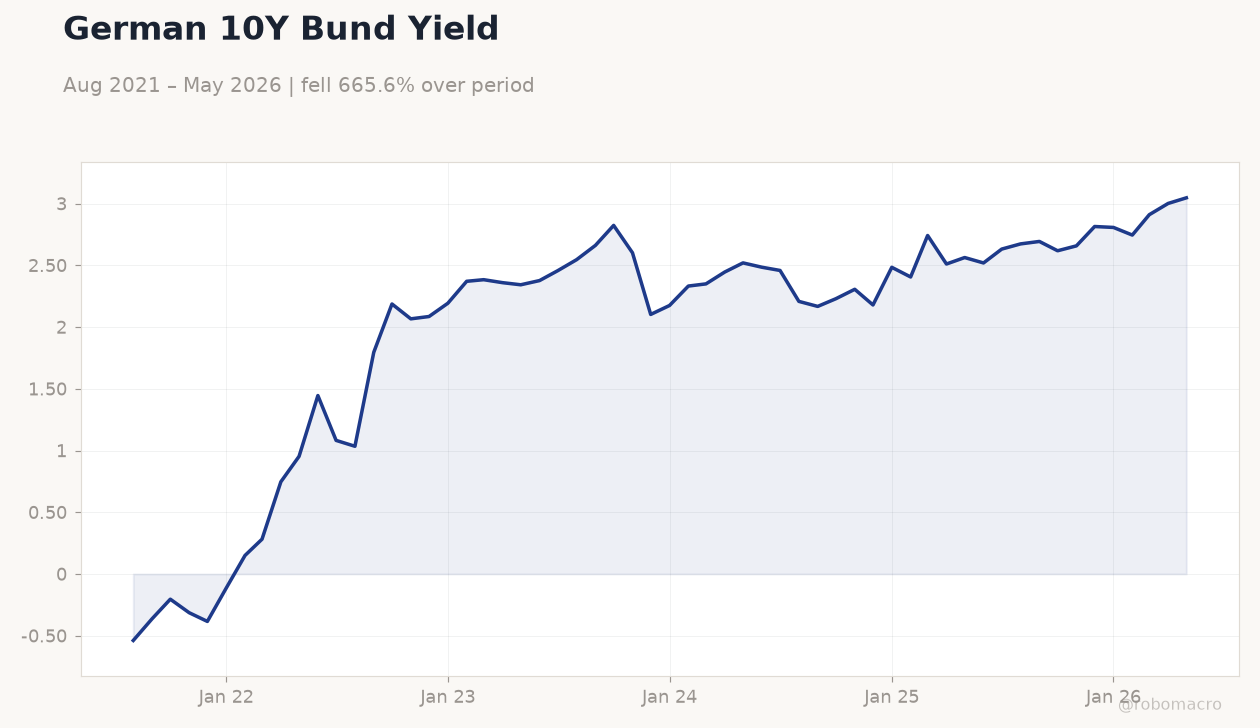

| German 10Y Bund | 3.05% | +1.52% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Inflation Rate Month-over-Month Preliminary | 0.10 | - | 0.60 |

| Inflation Rate Year-over-Year Preliminary | 3.20 | 3.20 | 3.20 |

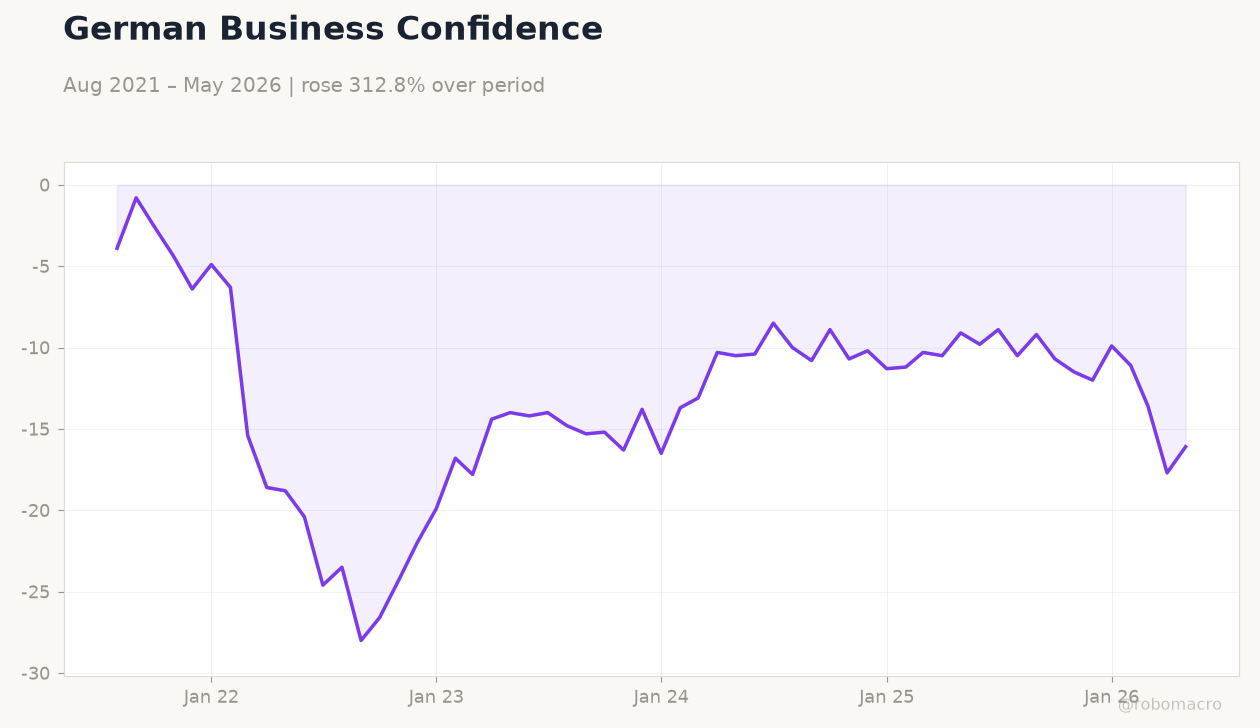

| Business Confidence Index | -3.70 | - | -2.40 |

| Retail Sales Month-over-Month | -0.40 | -0.10 | 1.10 |

| Retail Sales Year-over-Year | -0.60 | 0 | 1.80 |

| Inflation Rate Year-over-Year Preliminary | 2.40 | 2.10 | 1.80 |

| Inflation Rate Month-over-Month Preliminary | 0.10 | 0 | -0.20 |

| Headline Unemployment Rate | 6.30 | 6.30 | 6.30 |

| Unemployed Persons Level | 3.0m | - | 3.0m |

| Unemployment Level Change | -12,000 | 10,000 | -1,000 |

German 10Y Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.5386,2.187,2.102,2.405,3.001,3.046

German 10Y Bund Yield | Type: macro_line | Yield %: 3.046 (2026-05-01) | Range: -0.5386–3.046 | Trend(6pt): -0.5386,2.187,2.102,2.405,3.001,3.046

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Headline Unemployment Rate | 5.10 | 5.10 | 00:00 |

| Industrial Production Month-over-Month | 0.10 | -0.30 | 22:45 |

| S&P Global Services PMI | - | 50.90 | 23:15 |

| S&P Global Services PMI | - | - | 23:45 |

| Retail Sales Month-over-Month | 0 | 0.10 | 00:00 |

- Eurozone headline inflation slowed to 2.8% in June, below consensus, with core measures also moderating across major states.

- German retail sales rebounded sharply while Spanish manufacturing PMI contracted, highlighting uneven growth momentum.

- Equities advanced led by DAX gains of 1.5% as Bund yields rose modestly and EUR crosses eased against major peers.

Yesterday's Recap

French preliminary CPI fell to 1.8% year-over-year and -0.2% month-over-month, undershooting forecasts and reinforcing disinflation. German inflation printed at 2.3% year-over-year and -0.3% month-over-month, while Italian CPI eased to 3.0% year-over-year. Spanish inflation held at 3.2% year-over-year but rose 0.6% month-over-month.

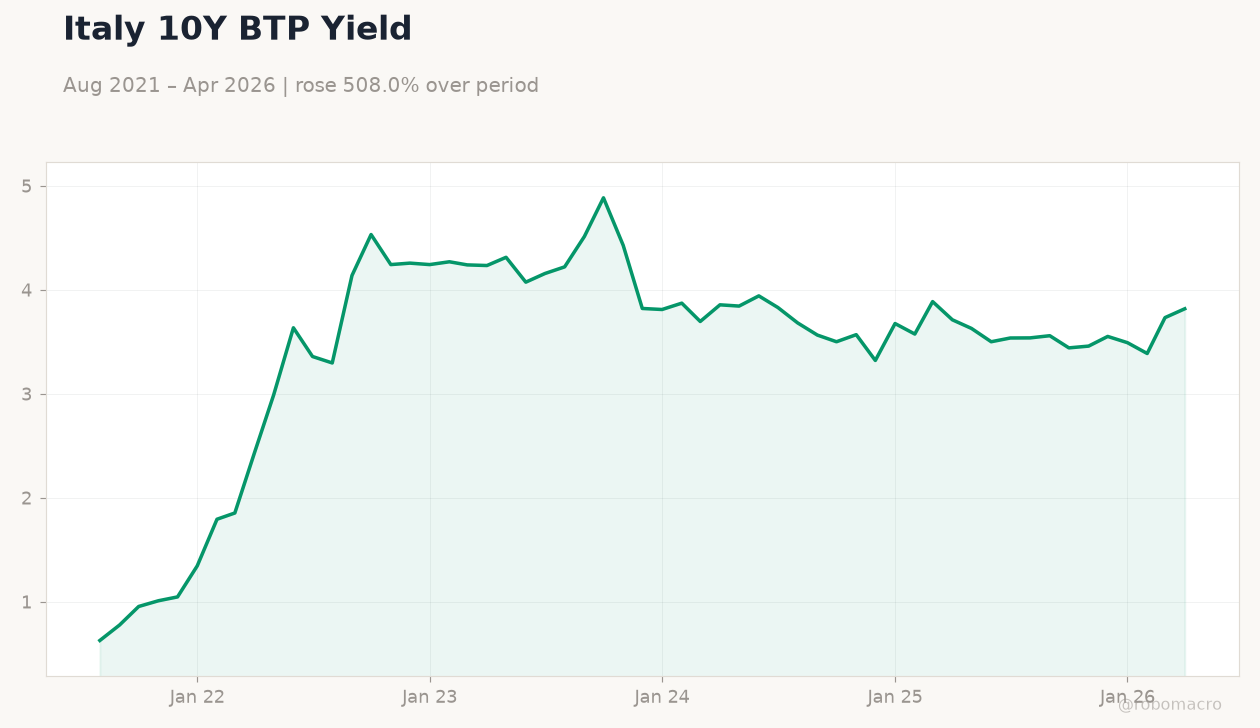

German retail sales jumped 1.1% month-over-month and 1.8% year-over-year, beating expectations, and unemployment stayed at 6.3%. Spanish manufacturing PMI dropped to 49.7, signaling contraction. Markets saw DAX rise 1.50% to 24,995.81, Euro Stoxx 50 edge up 0.08%, and German 10-year Bund yields climb to 3.05%.

EUR/USD slipped 0.05% to 1.14 amid the mixed data.

The Day Ahead

July 2 features sparse Eurozone releases with no tier-one prints scheduled across Germany, France, Italy or Spain. Attention turns to any follow-up remarks from ECB speakers on the latest inflation path. Equity markets are expected to consolidate after yesterday’s selective gains in German stocks.

Fixed-income desks will monitor Bund auction results and any shifts in peripheral spreads. Currency traders eye EUR crosses for direction amid thin economic calendars. Overall sentiment hinges on confirmation that disinflation remains on track without derailing growth.

Other Economic Notes

Disinflation broadened across member states as energy prices stabilized post earlier agreements, supporting the case for steady policy. German labor market resilience contrasted with softening Spanish factory activity, underscoring divergent national cycles. Retail strength in Germany may cushion overall Eurozone consumption even as PMI weakness flags manufacturing risks.

Broader themes point to gradual return toward target inflation without abrupt demand collapse.

Global Macro News

Global disinflation trends reinforced Eurozone moves as U.S. and Asian price data also cooled. Commodity markets saw Brent crude decline 0.75% to $71.03, easing imported inflation pressures.

<i>↓ p.2</i>