GCC Macro Daily(Beta Mode)

GCC Stocks Mixed as Oil Rises

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 24.96 | -3.03% |

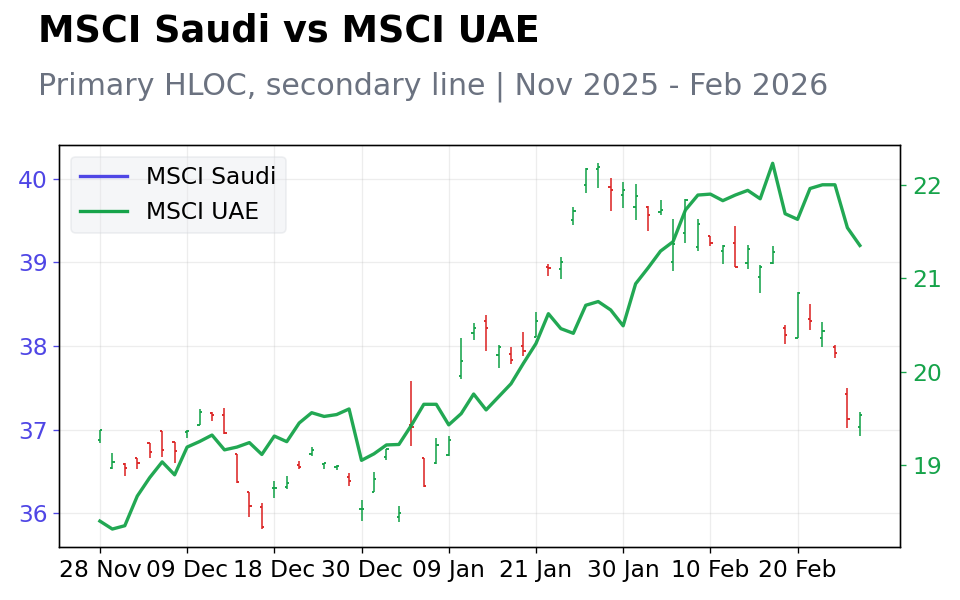

| MSCI Saudi | 37.17 | +0.11% |

| MSCI UAE | 21.35 | -0.88% |

| DFM General | 6,503.50 | -1.83% |

| MSCI Qatar | 19.46 | -0.31% |

| MSCI Kuwait | 37.99 | +2.84% |

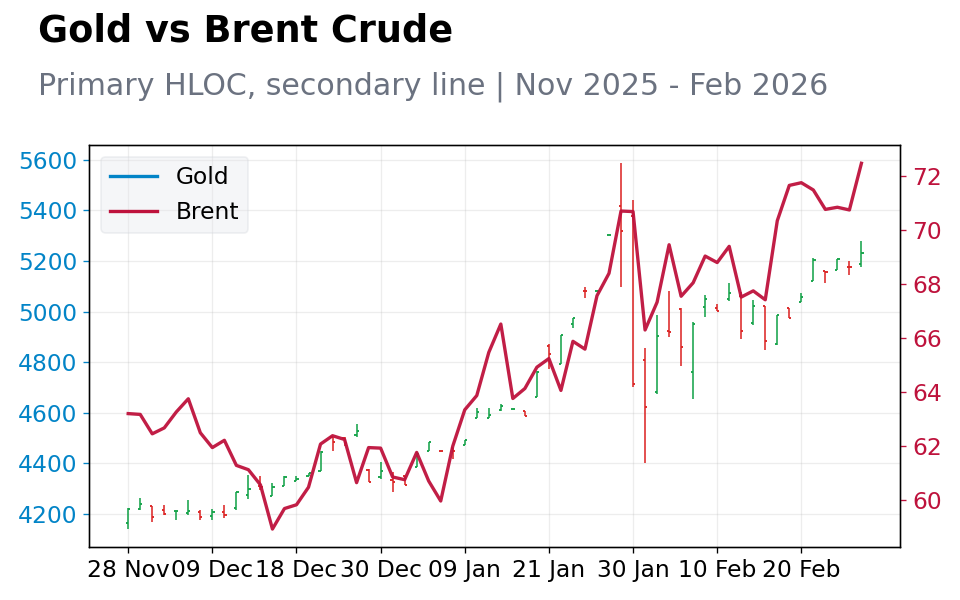

| Brent Crude | 72.48 | +2.45% |

| WTI Crude | 67.02 | +2.78% |

| Gold | 5,230.50 | +1.04% |

| USD/SAR | 3.75 | +0.12% |

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.24% |

| Bitcoin | 66,692.09 | +1.23% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Brent crude surged 2.45% to $72.48/bbl on stable Gulf geopolitics, enhancing fiscal prospects for Saudi Arabia and UAE.

- Saudi Aramco dropped 3.03% despite MSCI Saudi's 0.11% gain, with UAE and Qatar indices declining modestly.

- Kuwait's MSCI climbed 2.84% amid local optimism, while pegged currencies showed limited volatility.

Yesterday's Recap

Geopolitical stability persisted in the GCC, with Saudi Arabia and Qatar mediating de-escalation in the Afghanistan-Pakistan conflict, mitigating risks to regional security and supporting oil transit through the Strait of Hormuz. In Saudi Arabia, the Tadawul experienced mixed trading, with Saudi Aramco declining 3.03% to 24.96 amid profit-taking, though the MSCI Saudi index rose 0.11% to 37.17 on broader energy sector strength. UAE markets softened, with the MSCI UAE down 0.88% to 21.35 and DFM General falling 1.83% to 6,503.50, weighed by real estate and tech sectors despite no key data releases.

Qatar's MSCI decreased 0.31% to 19.46, reflecting caution in LNG-related stocks, while Kuwait's MSCI advanced 2.84% to 37.99 on banking sector positivity. Oil prices offered support, with Brent up 2.45% and WTI rising 2.78%, bolstering fiscal positions in Oman and Bahrain, where indices stayed muted without significant shifts. Overall, GCC sovereign CDS spreads narrowed slightly on the oil recovery, emphasizing crude's pivotal role in regional macro dynamics.

The Day Ahead

Absent scheduled data releases in the GCC, markets are expected to track global oil developments and any OPEC+ updates on production quotas, particularly affecting Saudi Arabia's fiscal strategy. UAE participants may watch Dubai's property market for non-oil growth indicators under diversification initiatives like Vision 2050. Qatar might focus on LNG export deals, while Kuwait monitors its basket-pegged dinar for stability.

Sentiment in Oman and Bahrain will likely depend on Brent movements, with potential for subdued trading without major catalysts. Anticipate low volatility in interbank rates such as SAIBOR and EIBOR, in line with Federal Reserve policy outlooks.

Other Economic Notes

GCC economies maintain emphasis on non-oil diversification, with Saudi Arabia's Vision 2030 progressing via initiatives like hosting the 2026 Dakar Rally, showcasing tourism opportunities. Oil continues as the primary driver, with yesterday's price increases strengthening fiscal balances but highlighting exposure to global demand fluctuations. Sovereign credit ratings for UAE and Qatar are supported by robust reserve levels, while Oman and Bahrain prioritize debt management within pegged currency frameworks.