Yesterday's Recap

Saudi Arabia's defense ministry reported intercepting 35 drones overnight and additional drones plus a ballistic missile in the eastern region, attributed to potential Houthi or Iranian proxies, with no damage to oil infrastructure but highlighting ongoing security threats. This follows multiple similar incidents, including more drone interceptions east of the country. The World Economic Forum postponed its Jeddah summit due to regional conflict, impacting global investment sentiment toward the GCC.

Reports suggest Saudi Arabia may be nearing involvement in the Iran conflict, escalating tensions, though the kingdom denies favoring prolonged war. UAE markets displayed divergence: the DFM General index jumped +4.15% to 5,697.71, buoyed by real estate and consumer optimism, contrasting with MSCI UAE's -2.85% drop to 18.07. Saudi Aramco fell -1.48% to 26.66, aligning with energy sector pressures as Brent crude plunged -5.78% to 98.45 and WTI dipped -0.80% to 91.61.

MSCI Saudi eased -0.37% to 37.72, MSCI Qatar declined -2.52% to 18.21, and MSCI Kuwait slipped -1.60% to 36.11, reflecting caution over geopolitical risks. Heavy rains struck UAE's Sharjah, Dubai, and Abu Dhabi, prompting police to lower speed limits and implement safety measures, potentially disrupting short-term economic activity. Qatar lifted remote work rules for private sector employees, signaling a return to office-based operations.

No macroeconomic data releases occurred across the GCC, keeping attention on security developments and commodity volatility.

The Day Ahead

No scheduled economic data releases or events in the GCC calendar, directing focus to potential updates on Saudi security measures post-interceptions, which could influence oil risk premiums and sovereign spreads. Monitoring for any escalation in Iran tensions, including threats to seize Bahrain and UAE coastlines or strike regional water infrastructure, remains key for Strait of Hormuz stability and energy flows. UAE may issue further guidance on rain-related disruptions, affecting transportation in major emirates.

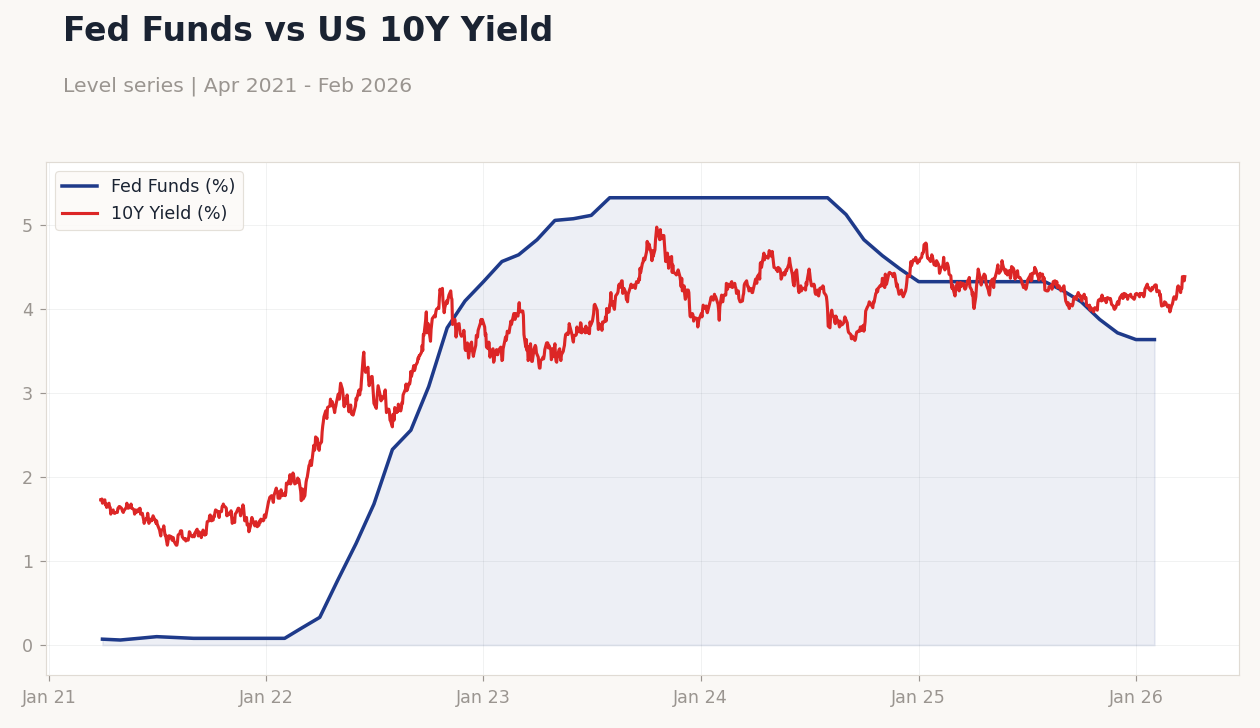

Qatar could provide details on implementing the remote work policy shift, aiding non-oil sector productivity. Globally, oil market dynamics and any US Fed signals will be watched, given GCC currency pegs to the USD.

Fed Funds vs US 10Y Yield | Type: macro_line | Fed Funds (%): 3.64 (2026-02-01) | Range: 0.06–5.33 | Trend(6pt): 0.07,1.21,5.33,4.83,3.72,3.64 | 10Y Yield (%): 4.39 (2026-03-24) | Range: 1.19–4.98 | Trend(5pt): 1.73,3.09,4.35,4.5,4.39

Fed Funds vs US 10Y Yield | Type: macro_line | Fed Funds (%): 3.64 (2026-02-01) | Range: 0.06–5.33 | Trend(6pt): 0.07,1.21,5.33,4.83,3.72,3.64 | 10Y Yield (%): 4.39 (2026-03-24) | Range: 1.19–4.98 | Trend(5pt): 1.73,3.09,4.35,4.5,4.39