Other Economic Notes

GCC economies continue pushing non-oil diversification, with Saudi Arabia advancing Vision 2030 initiatives like green hydrogen despite war disruptions. UAE retailers are innovating supply chains, using land routes from Europe to bypass maritime blockades and ensure food availability. Fiscal pressures from volatile oil prices are prompting Oman and Bahrain to ramp up renewable investments as a hedge against hydrocarbon reliance.

Broader themes include adapting to inflation risks from Strait of Hormuz tensions, with plastics and fuel costs rising globally, affecting export revenues.

Global Macro News

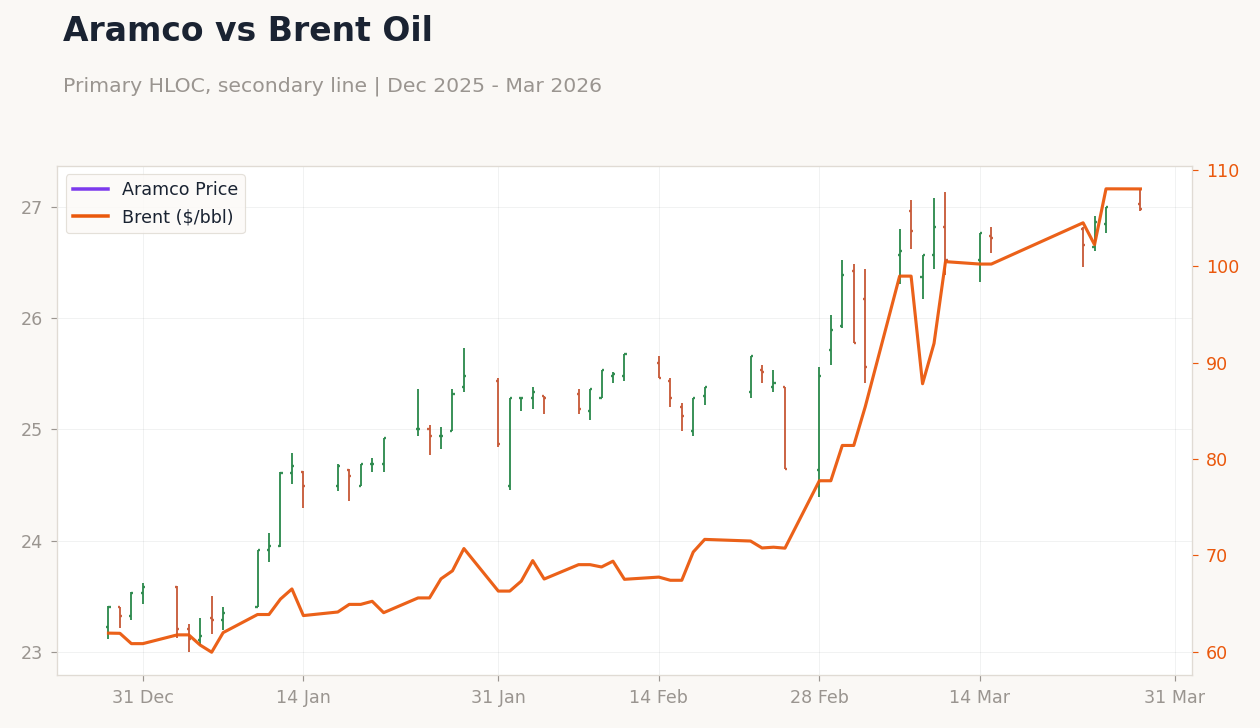

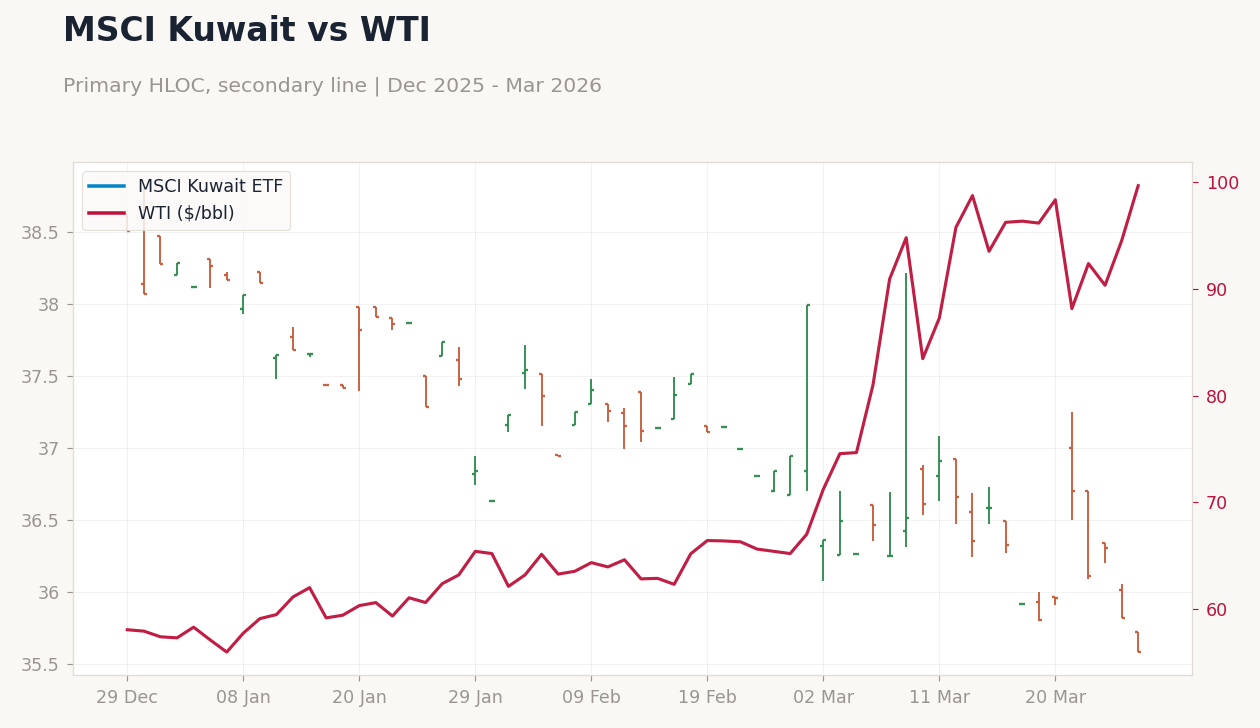

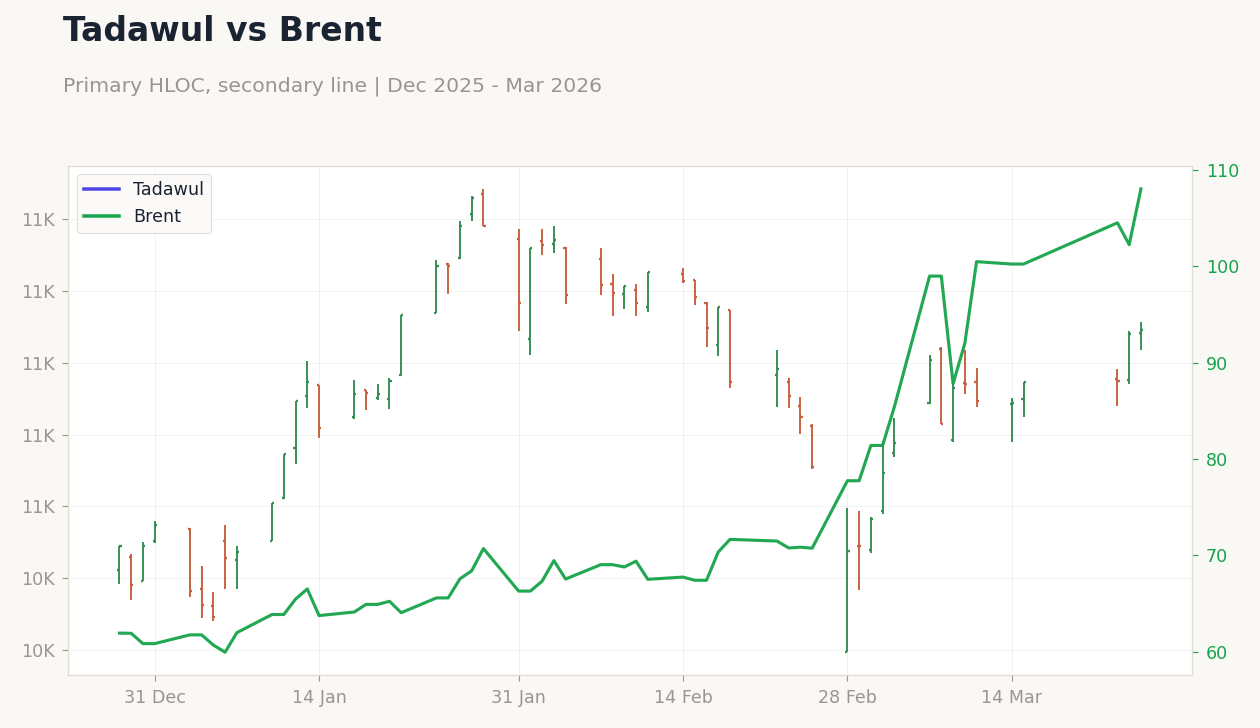

The Middle East conflict dominates global macro, with Iran's Strait of Hormuz threats fueling inflation fears in plastics and fuels, straining GCC oil exports. China's teapot refineries face margin squeezes from high crude prices, potentially curbing demand for GCC barrels and pressuring Brent. Ukraine signed a drone expertise deal with Saudi Arabia and bolstered ties with Qatar, UAE, and Jordan via Zelenskyy's visits, signaling new defense alliances amid regional attacks.

Houthi rebels claimed missile strikes on Israel and entered the fray with attacks on Saudi bases, injuring at least 15 U.S. personnel in Iranian-linked incidents. Pakistan is set to host U.S.-Iran talks involving Saudi Arabia, Turkey, and Egypt, amid Trump considerations for ground troops, heightening uncertainty.

Yemen's Houthis escalated by targeting Israel, while UAE's main aluminum smelter sustained significant damage from attacks, disrupting production. Abu Dhabi's Zayed International Airport operates at reduced capacity due to ongoing threats, with warnings for Dubai hubs. Retailers in the UAE are sourcing goods via alternative routes, like overland from London, to mitigate shortages.

The war, now a month old, is fostering long-term demand destruction, inflation, and recession risks, as noted at energy forums. Renewables are gaining appeal, though GCC transitions vary by economic structure and trade ties. Gold climbed 0.64% to 4,520.80 on safe-haven demand, while Bitcoin gained 1.08% to 67,035.66, largely detached from GCC fundamentals.

These dynamics expose GCC vulnerabilities to energy shocks and U.S. policy shifts.

Brent vs WTI Crude Prices | Type: macro_line | Brent ($/bbl): 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.52,120.8,97.1,73.19,118.4,103.8 | WTI ($/bbl): 89.33 (2026-03-23) | Range: 55.44–123.6 | Trend(6pt): 59.19,109.1,91.16,70.31,96.11,89.33

Brent vs WTI Crude Prices | Type: macro_line | Brent ($/bbl): 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(6pt): 63.52,120.8,97.1,73.19,118.4,103.8 | WTI ($/bbl): 89.33 (2026-03-23) | Range: 55.44–123.6 | Trend(6pt): 59.19,109.1,91.16,70.31,96.11,89.33