Yesterday's Recap

Geopolitical risks intensified as Saudi Arabia intercepted and destroyed seven drones and one additional drone over the past few hours, amid ongoing threats. Attacks targeted facilities across the region, including a UAE gas plant hit by debris, resulting in one Egyptian killed and four injured, and Emirates Global Aluminium warning of up to a year for full output restoration at a key Abu Dhabi facility. A Kuwait oil refinery was also hit in the latest Iran-linked incidents, with IRGC actions reportedly targeting iconic bridges in Bahrain, Kuwait, Saudi Arabia, UAE, Jordan, and Egypt to disrupt economy, tourism, and logistics.

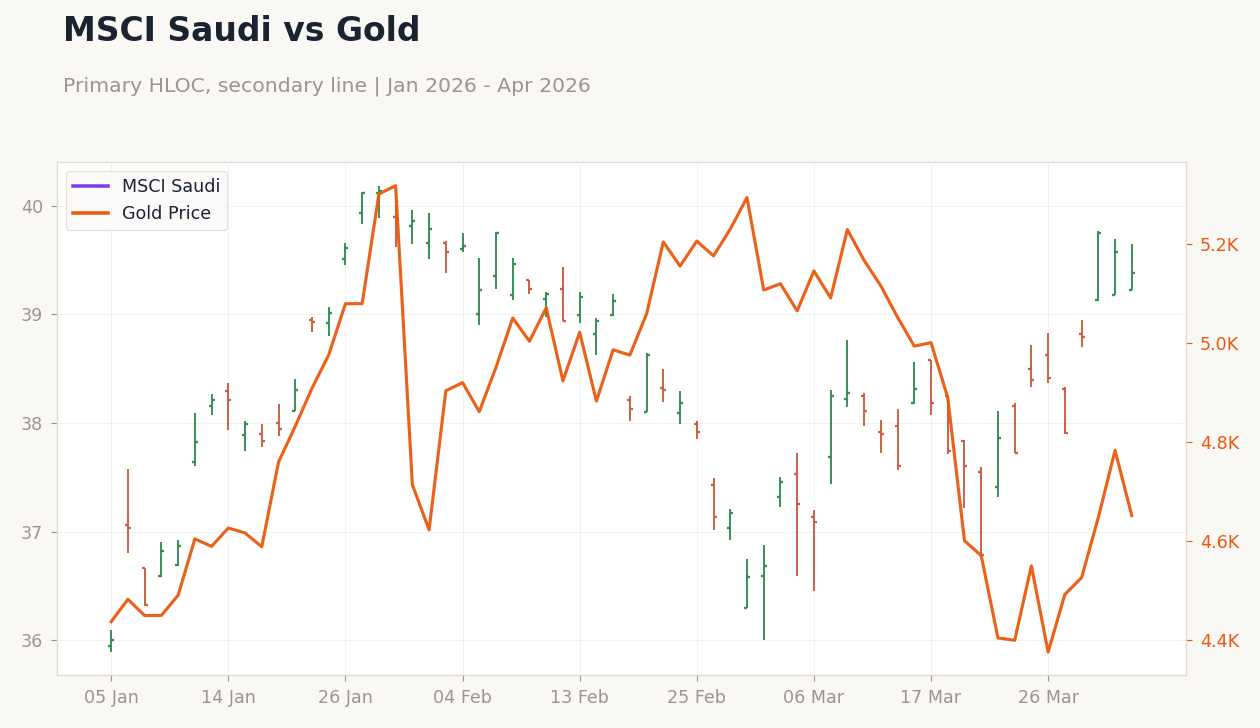

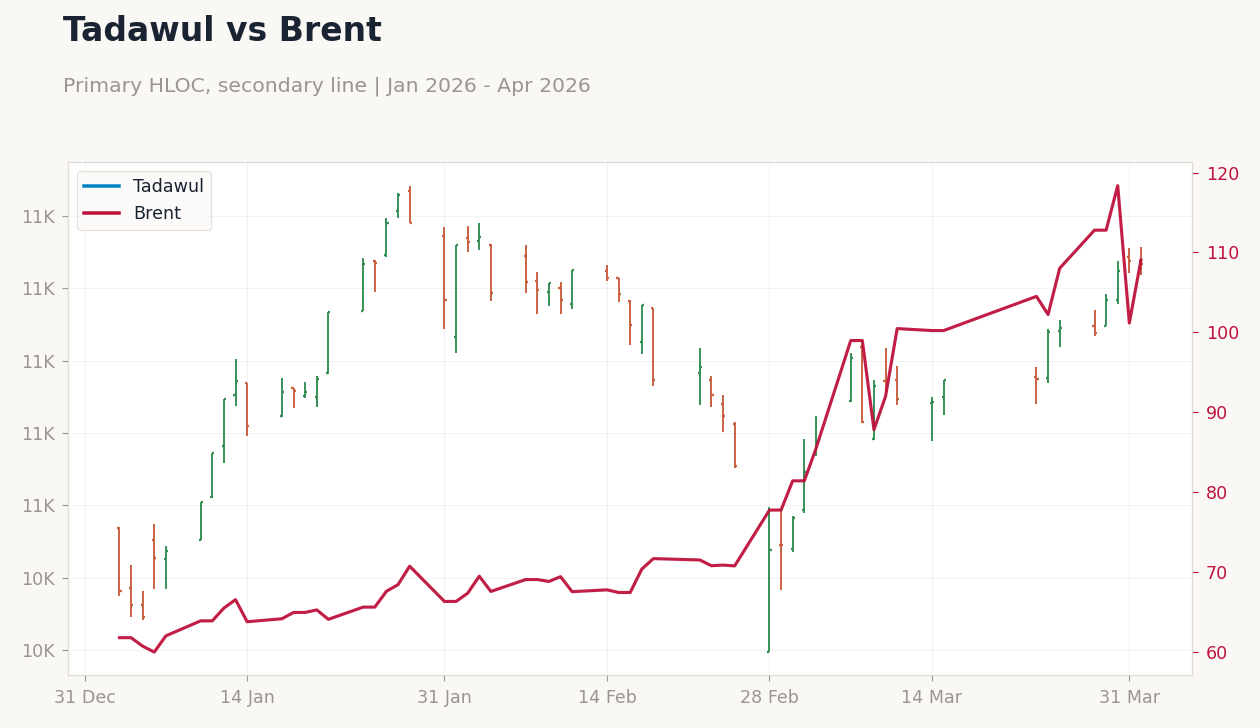

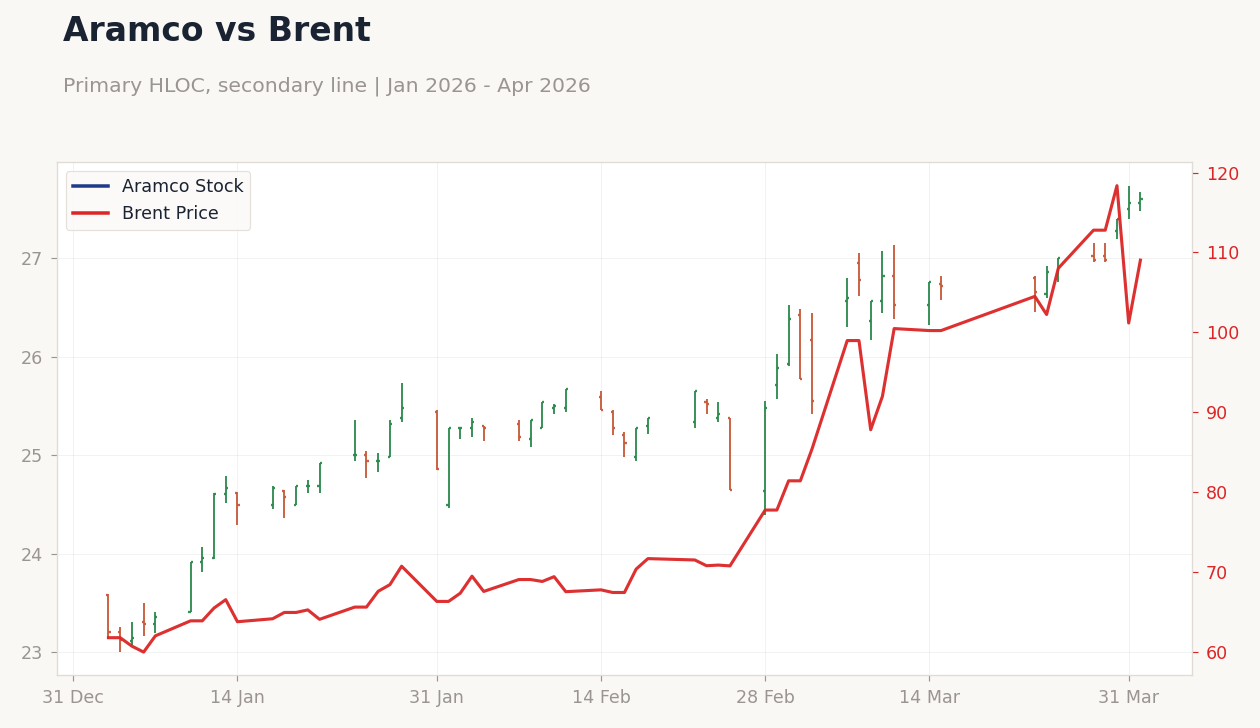

Saudi Sadara petrochemical giant halted all production, creating a plastics chokepoint. Saudi Aramco shares rose 1.56% to 27.40, driving the MSCI Saudi index up 2.47% to 39.75, reflecting oil market strength. Brent crude surged 7.78% to 109.03 and WTI climbed 11.41% to 111.54, bolstering fiscal positions across the GCC.

The UAE's DFM General index dipped 0.46% to 5,485.17, but MSCI UAE gained 4.54% to 18.65 amid energy optimism. Qatar's MSCI index advanced 2.22% to 18.60, and Kuwait's MSCI rose 1.57% to 36.14. Gold fell 2.75% to 4,651.50, while Bitcoin edged up 0.33% to 67,150.28.

FX moves were mixed: USD/SAR +0.13% to 3.75, USD/AED flat at 3.67, USD/KWD -0.66% to 0.31.

The Day Ahead

With no major scheduled data releases, attention turns to potential updates on geopolitical developments, including follow-ups on Iranian IRGC actions targeting infrastructure in Bahrain, Kuwait, Saudi Arabia, and the UAE. Italian Prime Minister Giorgia Meloni's visit to Saudi Arabia during her Gulf tour could yield announcements on energy cooperation, potentially influencing bilateral ties. Markets will monitor oil price volatility amid disruptions, with Brent futures sensitive to escalations.

In Qatar, warnings against using emergency alert tones as mobile ringtones highlight minor regulatory notes, but focus remains on LNG stability. UAE schools and KHDA responses to IGCSE, A Level, and IB exam cancellations may affect education trends, as seen in Saudi POS data surges. Overall, a quiet calendar underscores reliance on news flow for directional cues in GCC equities and FX.

Aramco vs Brent | Type: market_hloc | Aramco Stock: 27.6 (2026-04-02) | Range: 23.12–27.6 | Trend(6pt): 23.21,24.92,25.5,25.77,27.4,27.6 | Brent Price: 109 (2026-04-02) | Range: 59.96–118.3 | Trend(6pt): 61.76,67.57,70.35,91.98,101.2,109

Aramco vs Brent | Type: market_hloc | Aramco Stock: 27.6 (2026-04-02) | Range: 23.12–27.6 | Trend(6pt): 23.21,24.92,25.5,25.77,27.4,27.6 | Brent Price: 109 (2026-04-02) | Range: 59.96–118.3 | Trend(6pt): 61.76,67.57,70.35,91.98,101.2,109