GCC Macro Daily(Beta Mode)

Gulf Strikes Hit Energy, Oil Plunges

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.40 | +1.56% |

| MSCI Saudi | 39.75 | +2.47% |

| MSCI UAE | 18.65 | +4.54% |

| DFM General | 5,448.07 | -1.14% |

| MSCI Qatar | 18.60 | +2.22% |

| MSCI Kuwait | 36.14 | +1.57% |

| Brent Crude | 95.25 | -13.23% |

| WTI Crude | 96.23 | -14.39% |

| Gold | 4,836.20 | +3.85% |

| USD/SAR | 3.75 | +0.01% |

| USD/AED | 3.67 | -0.03% |

| USD/KWD | 0.31 | +0.00% |

| Bitcoin | 71,319.74 | +3.57% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

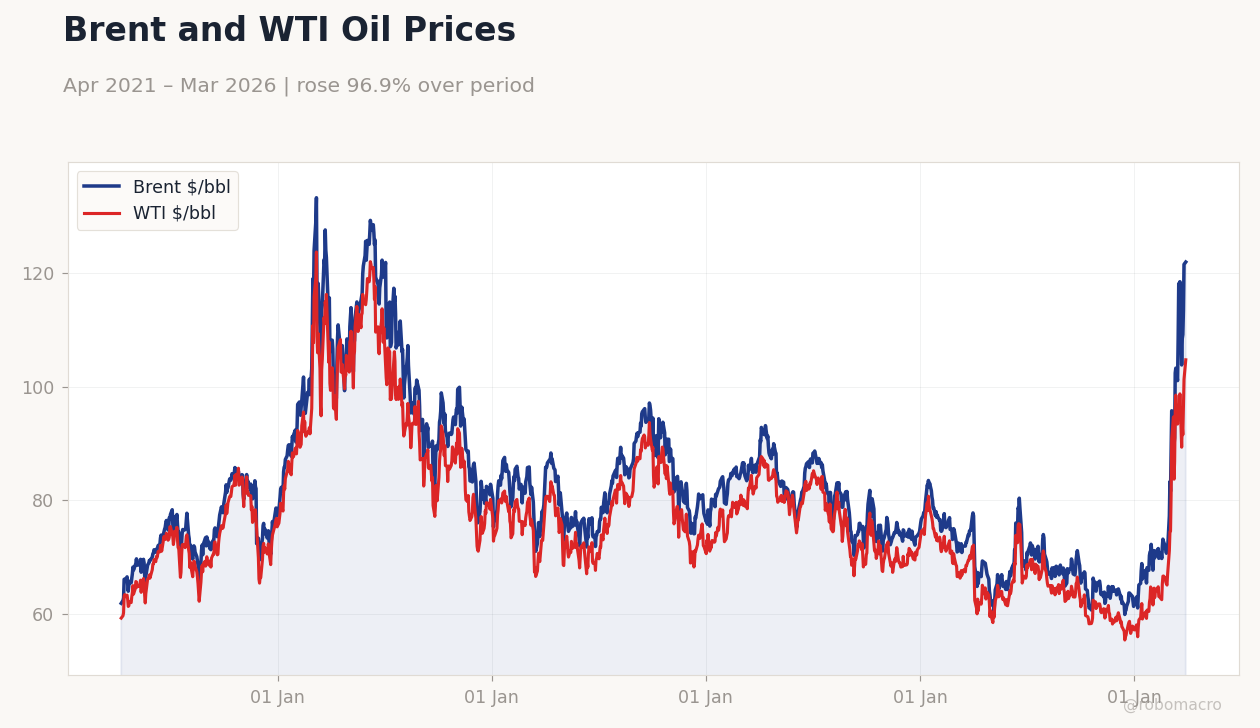

Brent and WTI Oil Prices | Type: macro_line | Brent $/bbl: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(6pt): 61.89,108.5,89.83,74.58,121.5,121.9 | WTI $/bbl: 104.7 (2026-03-30) | Range: 55.44–123.6 | Trend(6pt): 59.29,101.5,93.67,70.38,101.3,104.7

Brent and WTI Oil Prices | Type: macro_line | Brent $/bbl: 121.9 (2026-03-30) | Range: 59.93–133.2 | Trend(6pt): 61.89,108.5,89.83,74.58,121.5,121.9 | WTI $/bbl: 104.7 (2026-03-30) | Range: 55.44–123.6 | Trend(6pt): 59.29,101.5,93.67,70.38,101.3,104.7

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Iranian attacks disrupt UAE, Kuwait facilities and 17% of Qatar LNG amid Hormuz tensions.

- Saudi hikes Asian oil premiums to records despite Brent's 13.23% drop.

- GCC stocks mostly rise, led by UAE and Saudi, on diversification efforts.

Yesterday's Recap

Geopolitical risks intensified as Saudi Arabia intercepted seven missiles, with debris near energy sites, while Qatar reported four wounded, including a child, from missile fragments. UAE handled a drone incident near a telecom building in Fujairah. Despite tensions, Saudi Aramco climbed 1.56% to 27.40, lifting MSCI Saudi by 2.47%.

MSCI UAE jumped 4.54% on news of Dh6 billion highway and mass transit plans linking Dubai, Sharjah, and Ajman, though DFM General fell 1.14%. MSCI Qatar rose 2.22% amid LNG disruptions, with two tankers attempting Hormuz passage and force majeure declared on some exports. MSCI Kuwait gained 1.57% despite strikes on local plants.

Brent crude plunged 13.23% to 95.25 and WTI fell 14.39% to 96.23 on supply fears, while gold surged 3.85% to 4,836.20 as a safe haven. Bitcoin advanced 3.57% to 71,319.74. Saudi non-oil progress included SME financing emphasis and Saudization of 69 administrative roles.

First Kazakh halal products arrived in Saudi Arabia, boosting ties.

The Day Ahead

No scheduled economic releases in the GCC, giving markets time to assess Iranian strikes and Hormuz disruptions. Watch for updates on Saudi oil export redirections, as per IMF, to support revenues. UAE infrastructure reviews could lift construction and transport stocks.

Qatar's LNG force majeure may influence global energy prices, alongside Italian PM Meloni's visit highlighting Gulf ties. Potential security statements from Oman or Bahrain could arise, though unlisted. Oil volatility remains critical for GCC fiscal health, with focus on any tanker movements through Hormuz.

Other Economic Notes

Saudi Arabia advances non-oil diversification via core SME financing and Saudization expansions to 69 administrative professions, aligning with Vision 2030 to cut oil reliance. UAE's Dh6 billion plans for highways and mass transit between Dubai, Sharjah, and Ajman aim to enhance connectivity, trade, and tourism. GCC-wide, halal trade grows with Kazakh products entering Saudi markets, strengthening food security.

Saudi film sector expands through AlUla initiatives, diversifying entertainment. Pakistan's repayment of matured UAE loan deposits bolsters bilateral financial links.