Yesterday's Recap

Geopolitical risks intensified with a drone attack on a Saudi Arabian pipeline, eliminating 10% of the kingdom's oil export capacity, as reported by Middle East Eye and Financial Post. However, exports from the key Red Sea port remained stable for now, mitigating immediate supply shocks. Saudi Arabia's economy showed resilience amid the Iran war, Strait of Hormuz disruptions, and oil price volatility, according to Al Arabiya English.

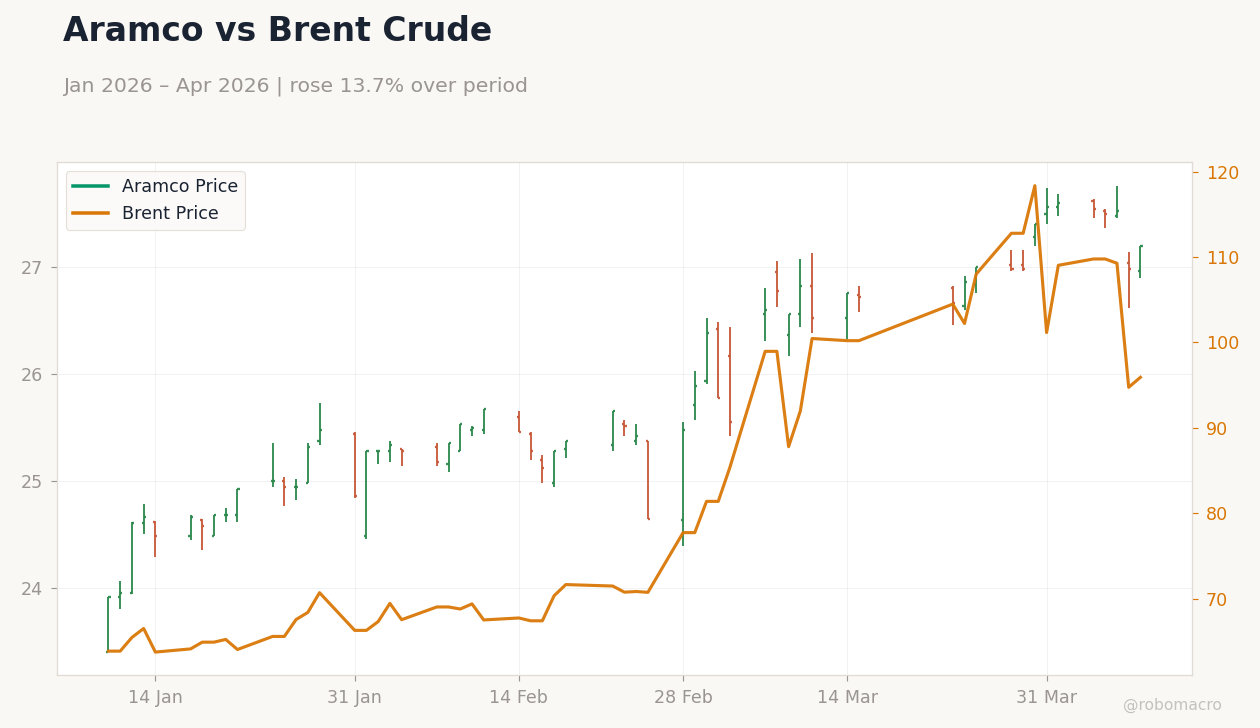

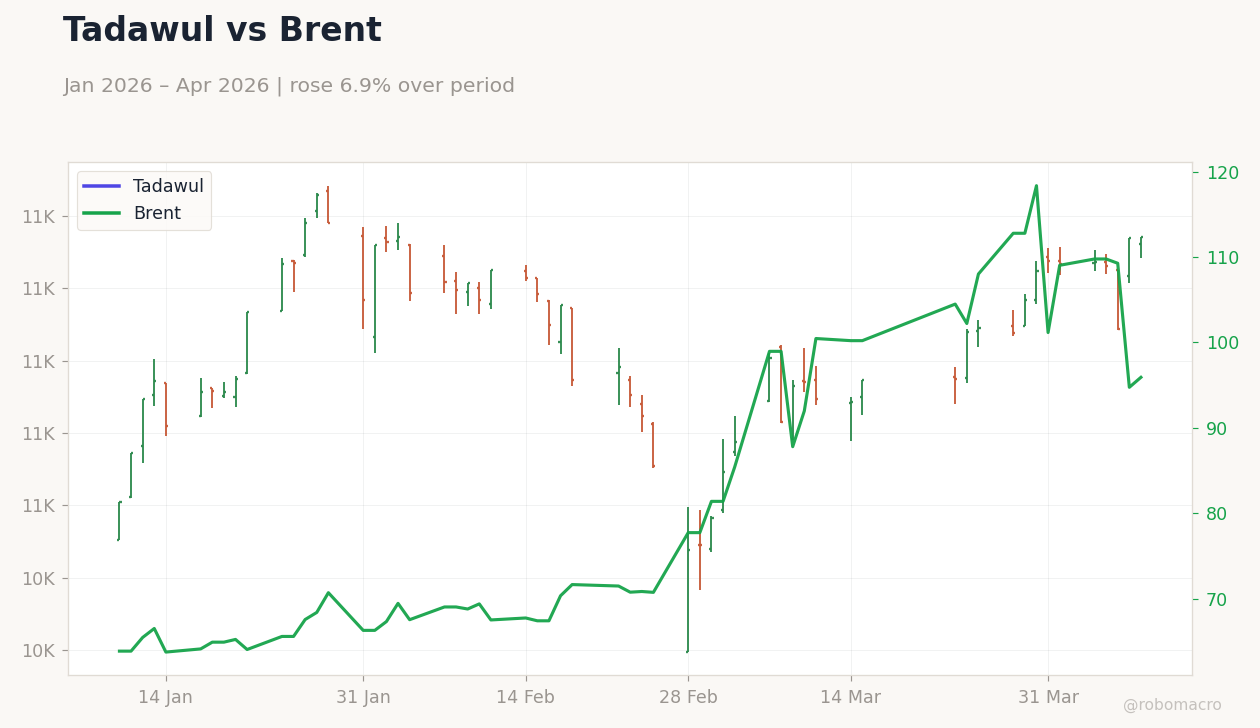

In markets, Saudi Aramco climbed 0.82% to 27.20, boosting the MSCI Saudi index by 0.15%. The DFM General in UAE rose 0.38%, but the MSCI UAE index fell 1.49% due to regional volatility. Qatar's MSCI index advanced 1.28%, while Kuwait's dipped 0.13%.

Brent crude declined 0.75% to 95.20, and WTI fell 1.33% to 96.57, reflecting contained de-escalation signals despite the attack. Gold eased 0.63% to 4,761.90, and Bitcoin gained 0.83% to 73,585.24. Currency pairs were stable, with USD/SAR up 0.11% to 3.75, USD/AED up 0.03% to 3.67, and USD/KWD down 0.75% to 0.31.

Other GCC markets, including Oman and Bahrain, saw limited activity with no major shifts reported.

The Day Ahead

No economic data releases are scheduled for GCC countries, shifting focus to geopolitical developments. Monitoring of the Strait of Hormuz standoff continues, with potential updates on Iran's naval activities and mine threats that could further impact oil transit. Saudi Arabia may issue statements on pipeline repair timelines and export recovery, influencing Aramco sentiment and Vision 2030 diversification.

UAE authorities could discuss tourism mitigation strategies amid projected $32bn regional losses from the Iran conflict, alongside flight resumptions to Dubai, Abu Dhabi, and Amman. Qatar's tourism sector may highlight responses to competition from Saudi Arabia and UAE, including visa extensions for stranded travelers to support recovery in Doha. Kuwait could see minor FX adjustments tied to its dinar basket peg, while Oman and Bahrain monitor energy supply chains.

Markets will watch for Yemen-related escalations or Red Sea shipping issues that might elevate risk premia.

Brent vs WTI Crude Prices | Type: macro_line | Brent Price: 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(5pt): 62.38,114,91.37,77.84,127.6 | WTI Price: 114 (2026-04-06) | Range: 55.44–123.6 | Trend(5pt): 59.7,104.6,88.81,73.79,114

Brent vs WTI Crude Prices | Type: macro_line | Brent Price: 127.6 (2026-04-02) | Range: 59.93–133.2 | Trend(5pt): 62.38,114,91.37,77.84,127.6 | WTI Price: 114 (2026-04-06) | Range: 55.44–123.6 | Trend(5pt): 59.7,104.6,88.81,73.79,114