GCC Macro Daily(Beta Mode)

Oil Slumps, Saudi Stocks Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.60 | +1.62% |

| MSCI Saudi | 40.19 | +1.26% |

| MSCI UAE | 19.57 | +1.98% |

| DFM General | 5,719.50 | +0.90% |

| MSCI Qatar | 19.17 | -1.06% |

| MSCI Kuwait | 37.63 | +0.87% |

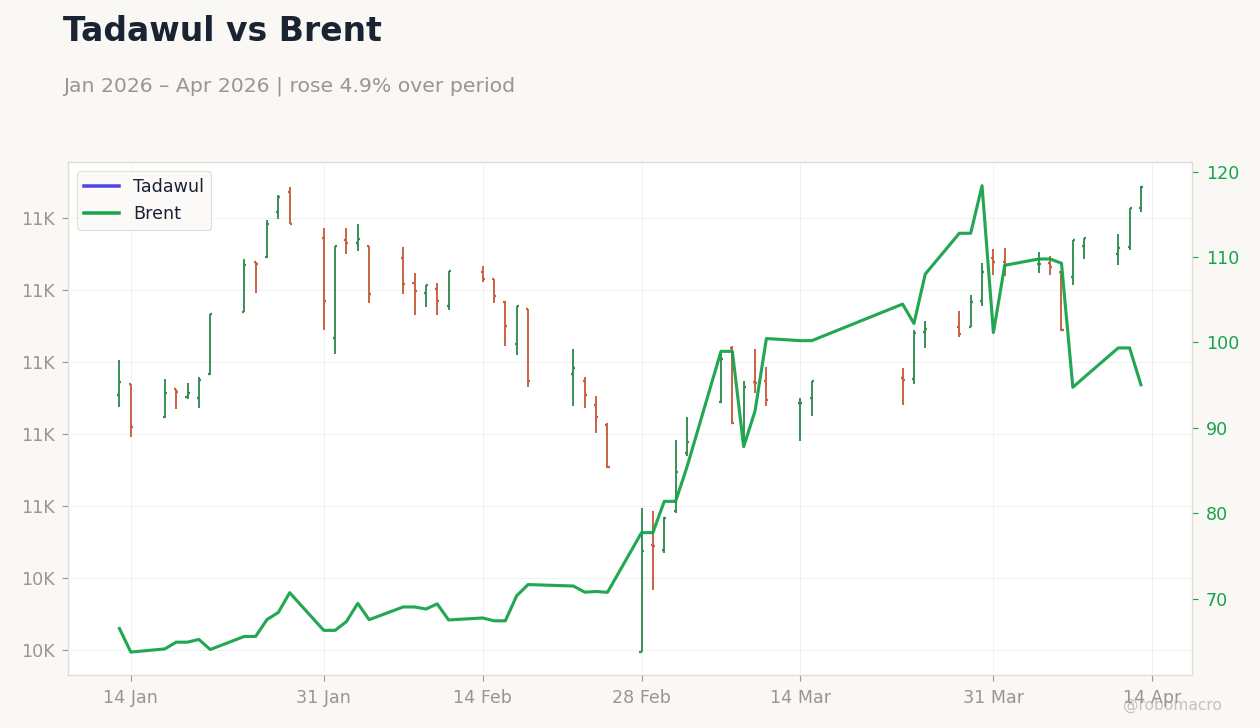

| Brent Crude | 95.13 | -4.26% |

| WTI Crude | 91.00 | -8.16% |

| Gold | 4,851.90 | +2.31% |

| USD/SAR | 3.75 | +0.09% |

| USD/AED | 3.67 | +0.01% |

| USD/KWD | 0.31 | +0.01% |

| Bitcoin | 74,352.50 | -0.18% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

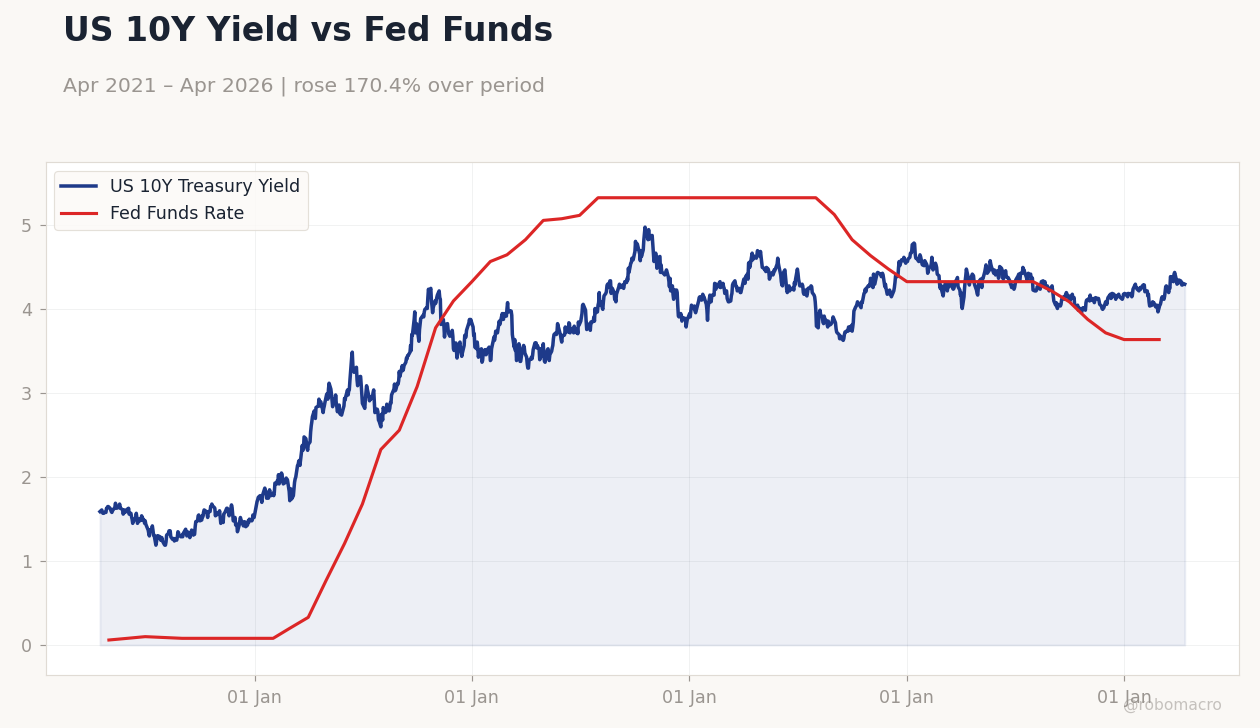

US 10Y Yield vs Fed Funds | Type: macro_line | US 10Y Treasury Yield: 4.3 (2026-04-13) | Range: 1.19–4.98 | Trend(6pt): 1.59,2.96,4.58,4.68,4.29,4.3 | Fed Funds Rate: 3.64 (2026-03-01) | Range: 0.06–5.33 | Trend(5pt): 0.06,1.68,5.33,4.64,3.64

US 10Y Yield vs Fed Funds | Type: macro_line | US 10Y Treasury Yield: 4.3 (2026-04-13) | Range: 1.19–4.98 | Trend(6pt): 1.59,2.96,4.58,4.68,4.29,4.3 | Fed Funds Rate: 3.64 (2026-03-01) | Range: 0.06–5.33 | Trend(5pt): 0.06,1.68,5.33,4.64,3.64

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Brent and WTI crude prices tumbled amid Iran conflict fallout and global energy market shifts, weighing on GCC revenues.

- Saudi equities advanced on Aramco gains and IMF growth optimism, while Qatar markets dipped.

- Headlines featured Saudi diversification pushes and regional diplomacy on Iran tensions.

Yesterday's Recap

GCC equities displayed mixed results, with Saudi markets outperforming on corporate strength and economic projections. Saudi Aramco climbed 1.62% to 27.60, lifting the MSCI Saudi index 1.26%, fueled by robust volumes and the IMF's 3.1% growth estimate for Saudi Arabia in 2026. UAE indices rose, with MSCI UAE up 1.98% and DFM General gaining 0.90%, aided by healthcare initiatives like Burjeel Hospital's Korean Pavilion in Abu Dhabi.

Qatar's MSCI index fell 1.06%, pressured by industrials amid LNG discussions. Kuwait's MSCI advanced 0.87%, with Oman and Bahrain showing little change absent key data. Oil markets dominated sentiment, as Brent dropped 4.26% to 95.13 and WTI slid 8.16% to 91.00, tied to Middle East tensions and revised outlooks.

Saudi expat remittances dipped to $3.34 billion in February, hinting at softer non-oil momentum.

The Day Ahead

With no significant economic releases on the GCC calendar for today or tomorrow, attention turns to geopolitical updates. Markets will watch for outcomes from talks among Turkey, Pakistan, Saudi Arabia, and Egypt on the Iran conflict, potentially easing oil risk premiums. Qatar's call to prioritize de-escalation in the Strait of Hormuz could support stable LNG routes.

UAE-Uzbekistan dialogues on new economy sectors may spur partnership news, enhancing diversification views. Saudi Arabia's new financial control law enforcement in the public sector could improve fiscal oversight, bolstering investor trust. Expect subdued trading unless fresh oil or regional developments emerge.

Other Economic Notes

Saudi Arabia's creative economy initiatives, including ties with Indonesia and Sanabil's $8 billion investment drive, align with Vision 2030's shift from oil reliance amid price volatility. The IMF's 3.1% 2026 growth forecast highlights reform resilience, though GCC faces challenges from remittance drops and energy fluctuations. UAE's healthcare expansions and Dubai's cultural events, like Vaisakhi celebrations and flag-themed exhibits, underscore tourism and services as key growth areas, mitigating oil exposure.