GCC Macro Daily(Beta Mode)

Saudi Non-Oil Exports Surge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.22 | -0.15% |

| MSCI Saudi | 39.08 | +0.23% |

| MSCI UAE | 19.46 | +2.05% |

| DFM General | 5,854.19 | +0.69% |

| MSCI Qatar | 19.25 | +0.68% |

| MSCI Kuwait | 38.87 | +0.78% |

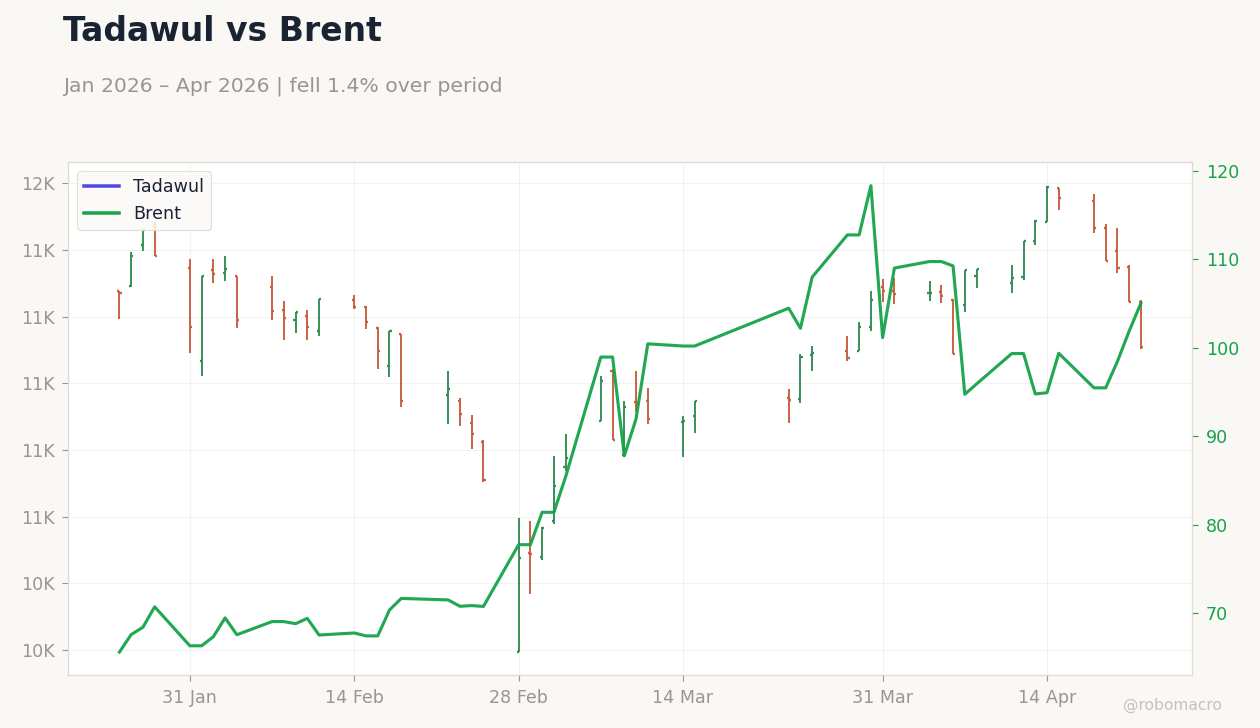

| Brent Crude | 100.27 | -4.80% |

| WTI Crude | 95.30 | +0.95% |

| Gold | 4,733.30 | +0.23% |

| USD/SAR | 3.75 | +0.11% |

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.25% |

| Bitcoin | 79,162.81 | +2.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Price Trend | Type: macro_line | Brent Crude (USD/bbl): 103.4 (2026-04-20) | Range: 59.93–138.2 | Trend(6pt): 67.08,108.2,91.88,81.68,98.63,103.4

Brent Crude Price Trend | Type: macro_line | Brent Crude (USD/bbl): 103.4 (2026-04-20) | Range: 59.93–138.2 | Trend(6pt): 67.08,108.2,91.88,81.68,98.63,103.4

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Year-over-Year Preliminary | 5 | - | 02:00 |

- Saudi non-oil exports rose 15% in February to $8.27bn, advancing Vision 2030 diversification amid mixed oil prices.

- GCC equities showed gains, with MSCI UAE up 2.05% on tourism rebound, while Brent crude fell 4.80% to $100.27.

- Regional security tensions rise with condemnations of drone attacks on Kuwaiti borders from Iraq.

Yesterday's Recap

GCC markets displayed mixed performance on April 25, with UAE equities leading amid real estate and telecom gains; MSCI UAE rose 2.05% and DFM General climbed 0.69% to 5,854.19. Saudi Arabia's MSCI index edged up 0.23% to 39.08, buoyed by banking despite Saudi Aramco dipping 0.15% to 27.22. Qatar and Kuwait posted modest advances, with MSCI Qatar up 0.68% to 19.25 and MSCI Kuwait gaining 0.78% to 38.87.

Brent crude dropped sharply by 4.80% to $100.27, weighing on fiscal outlooks, while WTI increased 0.95% to $95.30. No major data releases occurred, but Saudi non-oil exports climbed 15% in February to $8.27bn per GASTAT, highlighting diversification efforts. Regional security drew focus after drone attacks on Kuwaiti borders from Iraq prompted condemnations from Qatar.

Currency pegs remained stable, with USD/SAR at 3.75 (+0.11%), USD/AED at 3.67 (+0.04%), and USD/KWD at 0.31 (-0.25%). Gold rose 0.23% to $4,733.30, and Bitcoin gained 2.00% to $79,162.81.

The Day Ahead

Attention turns to Saudi Arabia's preliminary GDP growth year-over-year data on April 30 at 02:00 ET, with previous at 5% and no consensus yet, potentially reflecting non-oil progress under Vision 2030. No events are scheduled for today or tomorrow across the GCC, giving markets time to absorb recent export data and oil volatility. Monitoring of regional tensions continues, including potential fallout from drone attacks on Kuwait and Iraq-Saudi pipeline hurdles.

UAE biosecurity deals may bolster agribusiness sentiment, while Qatar's LNG focus could stabilize equities. Gold and Bitcoin provide hedges against oil dependency, with ongoing Strait of Hormuz vigilance amid Iran's drills, though traffic remains unimpeded.

Other Economic Notes

Saudi Arabia's Vision 2030 annual report shows most indicators met targets, with non-oil investments expected to reach SAR 797 billion in 2025, boosting their economic share to 30% and emphasizing private sector roles. Non-oil exports surged 15% in February to $8.27bn, and chemical exports jumped 18% on stronger demand. Challenges include hurdles to the Iraq-Saudi pipeline, potentially affecting energy flows.

UAE advances food security as a "golden age" per SDA, alongside biosecurity cooperation between MOCCAE and ADQCC, and meetings like UAE President with India's NSA. (cont...)