GCC Macro Daily(Beta Mode)

UAE Announces OPEC Exit Amid Hormuz Crisis

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.26 | +0.52% |

| MSCI Saudi | 38.97 | -0.28% |

| MSCI UAE | 19.46 | +0.00% |

| DFM General | 5,857.83 | -0.22% |

| MSCI Qatar | 19.10 | -0.78% |

| MSCI Kuwait | 38.83 | -0.10% |

| Brent Crude | 103.87 | -4.03% |

| WTI Crude | 99.06 | +2.79% |

| Gold | 4,611.90 | -1.36% |

| USD/SAR | 3.75 | +0.11% |

| USD/AED | 3.67 | +0.02% |

| USD/KWD | 0.31 | -0.30% |

| Bitcoin | 76,518.00 | -1.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent vs WTI Crude Prices | Type: macro_line | Brent $/bbl: 103.4 (2026-04-20) | Range: 59.93–138.2 | Trend(5pt): 67.73,109.6,90.14,80,103.4 | WTI $/bbl: 91.06 (2026-04-20) | Range: 55.44–123.6 | Trend(5pt): 63.5,97.74,89.35,76.79,91.06

Brent vs WTI Crude Prices | Type: macro_line | Brent $/bbl: 103.4 (2026-04-20) | Range: 59.93–138.2 | Trend(5pt): 67.73,109.6,90.14,80,103.4 | WTI $/bbl: 91.06 (2026-04-20) | Range: 55.44–123.6 | Trend(5pt): 63.5,97.74,89.35,76.79,91.06

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| GDP Growth Year-over-Year Preliminary | 5 | - | 22:00 |

- UAE announces exit from OPEC and OPEC+ effective May 1, aligning with long-term energy strategy amid Hormuz disruptions and Iran tensions.

- Gulf leaders set to meet in Saudi Arabia to discuss Iran war risks, focusing on regional stability and oil supply security.

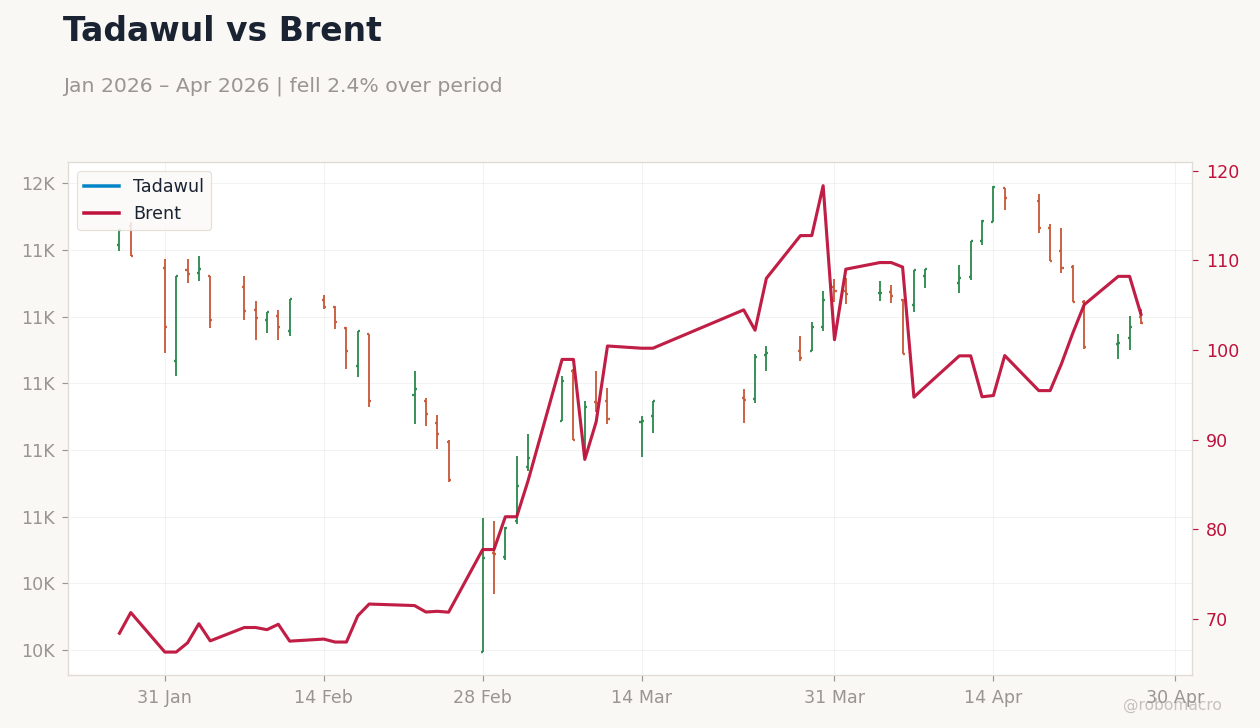

- Oil markets volatile with Brent down 4.03% on supply fears; GCC equities mixed, reflecting energy sector pressures and geopolitical uncertainty.

Yesterday's Recap

GCC markets displayed mixed results on April 27 amid rising geopolitical tensions, with no significant data releases. Saudi Aramco climbed 0.52% to 27.26, supported by steady oil demand despite volatility, while the MSCI Saudi index fell 0.28% to 38.97 due to profit-taking outside energy. UAE's DFM General index dropped 0.22% to 5,857.83, weighed by real estate amid regional risks, with MSCI UAE unchanged at 19.46.

Qatar's MSCI index declined 0.78% to 19.10 on energy exposure, and Kuwait's MSCI eased 0.10% to 38.83 with stable local activity. Brent crude tumbled 4.03% to 103.87, pressured by Hormuz chokepoint concerns affecting tanker flows, while WTI rose 2.79% to 99.06 on U.S. supply factors.

Gold slipped 1.36% to 4,611.90, and Bitcoin fell 1.10% to 76,518.00 in a risk-averse environment. FX moves were modest: USD/SAR up 0.11% to 3.75, preserving peg stability; USD/AED up 0.02% to 3.67; USD/KWD down 0.30% to 0.31 from basket shifts. The UAE's OPEC departure news overshadowed trading, heightening fiscal worries for oil-reliant economies like Saudi Arabia and Bahrain.

The Day Ahead

Saudi Arabia's preliminary Q1 GDP growth year-over-year releases late on April 29 at 22:00 ET, with previous at 5% and no consensus available, offering insights into Vision 2030 non-oil progress. Gulf leaders' summit in Riyadh will address Iran war strategies, potentially impacting oil risk premia and regional CDS spreads. No other key GCC events are slated, but Hormuz traffic monitoring may spark energy market swings.

UAE's new passenger rights and complaint service for travelers could aid tourism, while first Iranian pilgrims arriving for Hajj signal normalized Saudi-Iran ties. Qatar and UAE may issue updates on OPEC shifts, influencing LNG strategies.

Other Economic Notes

GCC diversification efforts advance, with Saudi Arabia's new law capping travel bans at three years to enhance labor mobility and support Vision 2030. UAE's OPEC exit supports its 2050 energy independence goals, emphasizing renewables amid crude volatility. Heavy rains expected across Saudi Arabia may affect infrastructure and logistics through the week.

(cont...)