GCC Macro Daily(Beta Mode)

Oil Slumps, GCC Non-Oil Resilient

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.50 | +0.00% |

| MSCI Saudi | 38.73 | -1.48% |

| MSCI UAE | 18.98 | -2.52% |

| DFM General | 5,729.07 | -0.88% |

| MSCI Qatar | 18.89 | +0.48% |

| MSCI Kuwait | 38.37 | -0.75% |

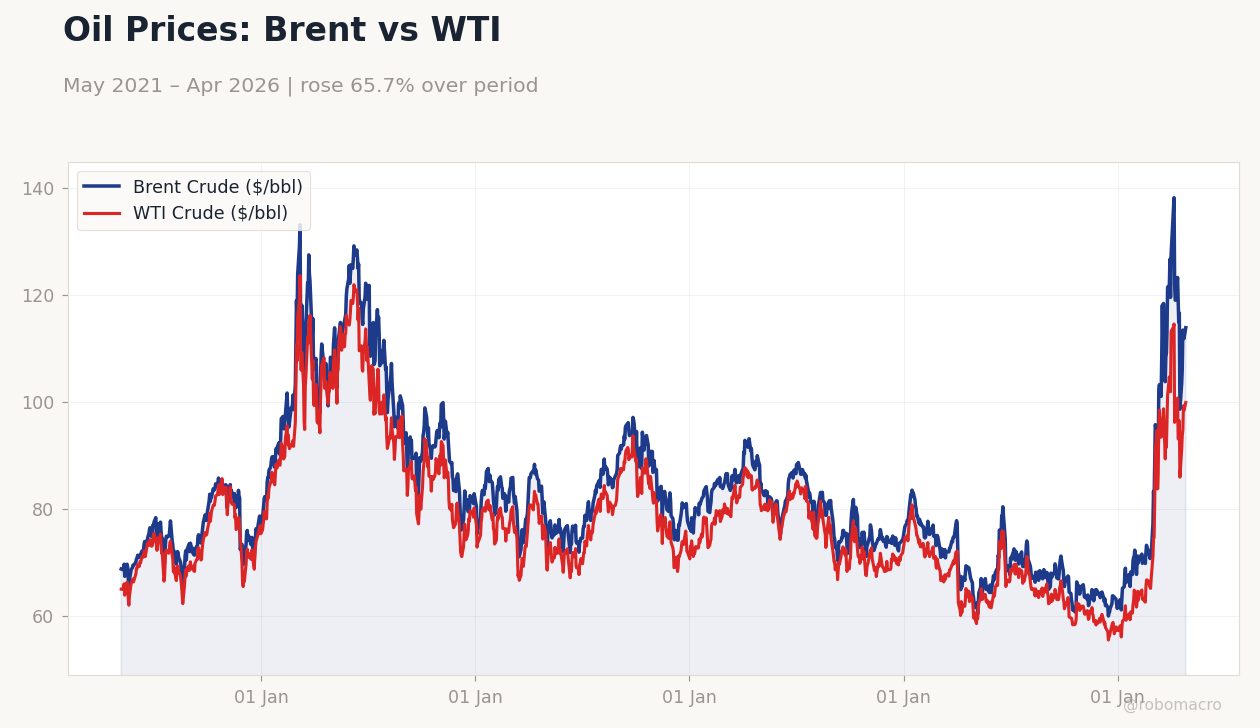

| Brent Crude | 108.14 | -5.51% |

| WTI Crude | 100.70 | -5.37% |

| Gold | 4,646.10 | +2.80% |

| USD/SAR | 3.75 | +1.69% |

| USD/AED | 3.67 | +0.02% |

| USD/KWD | 0.31 | -0.36% |

| Bitcoin | 81,379.74 | +1.94% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

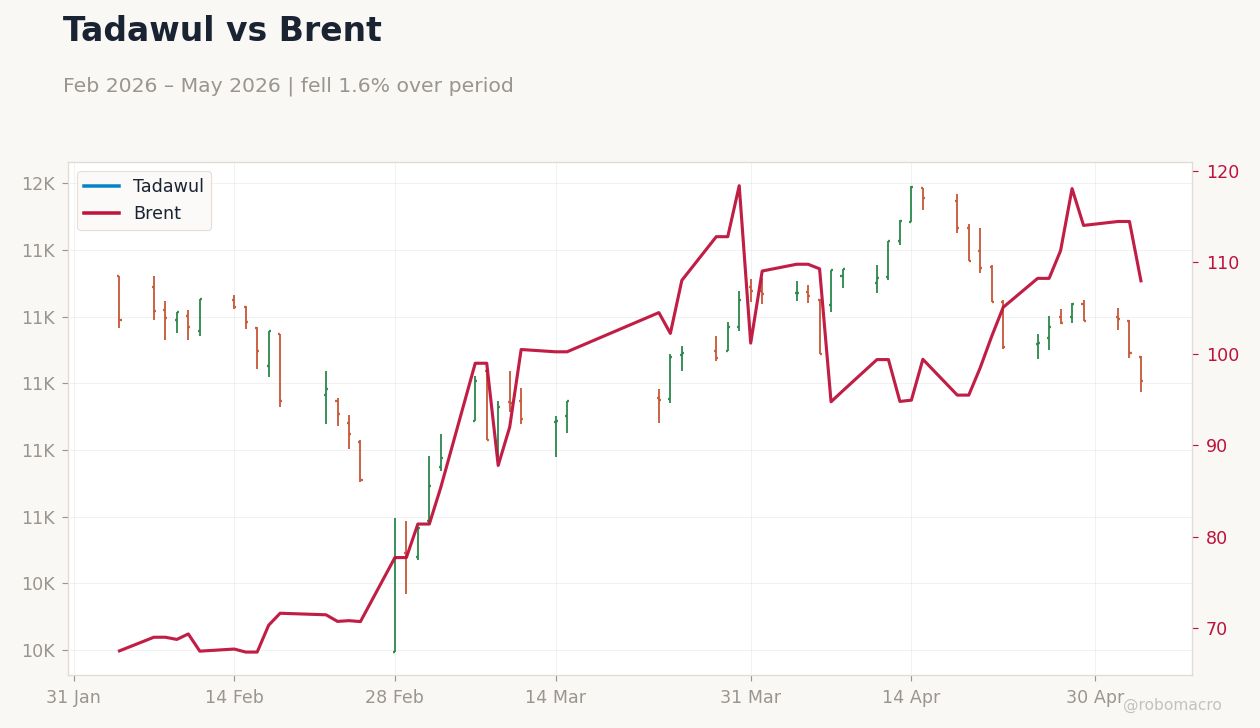

Oil Prices: Brent vs WTI | Type: macro_line | Brent Crude ($/bbl): 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 68.73,106.5,86.82,78.01,113.9 | WTI Crude ($/bbl): 99.89 (2026-04-27) | Range: 55.44–123.6 | Trend(5pt): 64.96,97.14,83.8,74.15,99.89

Oil Prices: Brent vs WTI | Type: macro_line | Brent Crude ($/bbl): 113.9 (2026-04-27) | Range: 59.93–138.2 | Trend(5pt): 68.73,106.5,86.82,78.01,113.9 | WTI Crude ($/bbl): 99.89 (2026-04-27) | Range: 55.44–123.6 | Trend(5pt): 64.96,97.14,83.8,74.15,99.89

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Saudi non-oil revenues up 2% to $30.9bn in Q1 amid tourism boom, offsetting SR125.7bn deficit from lower oil income.

- UAE navigates Iranian attacks with missile warnings, OPEC exit clarifications, PMI easing, and property rebound in Abu Dhabi and Dubai.

- Qatar's non-energy PMI rises to 46.4 in April, easing contraction, while LNG force majeure extends to mid-June.

Yesterday's Recap

Saudi Arabia's non-oil private sector showed growth despite client spending deferrals due to regional conflicts, with non-oil revenues rising 2% to $30.9bn in Q1 and a budget deficit of SR125.7bn on lower oil revenues. UAE equities declined, with MSCI UAE down 2.52% and DFM General off 0.88%, amid Iranian drone strikes, missile warnings, and PMI easing. Qatar's MSCI index gained 0.48%, supported by slower non-energy contraction, though LNG disruptions continue with force majeure extended.

Kuwait's MSCI fell 0.75%, while Saudi Aramco held flat at 27.50. Brent crude dropped 5.51% to $108.14, WTI fell 5.37% to $100.70, pressuring GCC fiscal positions. Gold rose 2.80% to $4,646.10 on safe-haven demand.

FX rates were mixed: USD/SAR up 1.69% to 3.75, USD/AED up 0.02% to 3.67, USD/KWD down 0.36% to 0.31. Bitcoin climbed 1.94% to $81,379.74. Overall, oil weakness dominated sentiment, but non-oil sectors provided some resilience.

The Day Ahead

No major economic data releases are scheduled. Attention turns to geopolitical developments, including UAE's OPEC exit implications and tensions with Iran in the Strait of Hormuz. Saudi Arabia could see updates on Q1 budget impacts and tourism growth projections.

UAE may highlight defence manufacturing deals, digital bank expansions, and AI initiatives in Dubai. Qatar's LNG force majeure extension merits monitoring for export stability. GCC markets will watch Brent crude trends and any Red Sea shipping updates, with potential influences from global energy demand signals like US LNG boosts.

Other Economic Notes

Saudi Arabia solidifies its position as the region's top tourism economy, leading Middle East growth into 2025, with non-oil diversification advancing under Vision 2030. UAE property markets in Abu Dhabi and Dubai rebounded in April despite headwinds, bolstered by defence hub deals and AI pushes. Qatar's non-energy economy contracted for a fifth month but at a slower pace, with PMI at 46.4 reflecting softer declines in orders and output.

Regional dynamics include a growing UAE-Saudi rift and OPEC+ shifts post-UAE exit, potentially affecting energy cooperation. (cont...)