Other Economic Notes

GCC economies prioritize non-oil diversification through frameworks like Saudi Vision 2030 and UAE 2050, channeling investments into tourism, defense, and renewables to counter oil price swings. Fiscal challenges arise from geopolitical risks, such as Iranian attacks on UAE and Houthi threats, raising sovereign credit premia and disrupting energy flows. Advances in LNG projects, including Qatar's North Field expansion and UAE's defense hub, aim to strengthen export resilience and draw foreign capital.

Regional PMI trends show mixed non-oil activity, with Saudi growth offsetting contractions elsewhere, while foreign inflows signal investor confidence recovery.

Global Macro News

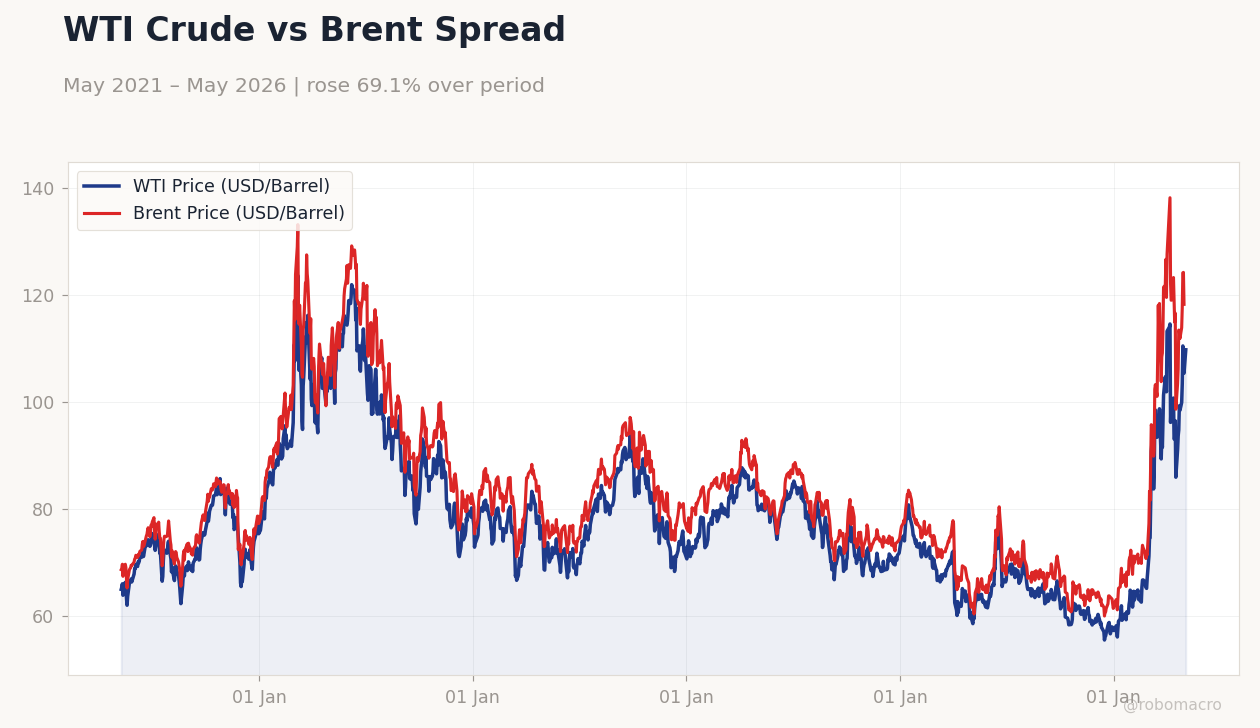

Crude prices plunged, with Brent down 7.33% to 101.82 and WTI off 6.45% to 95.67, straining GCC oil-reliant budgets but possibly curbing global inflation. Geopolitical strains intensified from Iranian attacks on UAE, prompting GCC condemnations and pushes for a US-Iran MOU to halt strikes and foster energy trade, including LNG and LPG links. Gold rose 3.49% to 4,714.60 as a haven asset.

USD strength bolstered GCC pegs, with USD/SAR up 1.70% to 3.75, USD/AED up 0.03% to 3.67, and USD/KWD down 0.02% to 0.31. Bitcoin edged 0.21% higher to 81,100.19 amid crypto steadiness. OPEC+ eyes post-cut decisions to steady markets, while US LNG demand aids Qatar and UAE shipments, as seen in Adnoc's Hormuz exports and Pakistan's spot bids.

Broader shifts include US-Qatar jet deals and Japanese-UAE health partnerships, influencing regional alliances and trade.

GCC Central Banks Watch

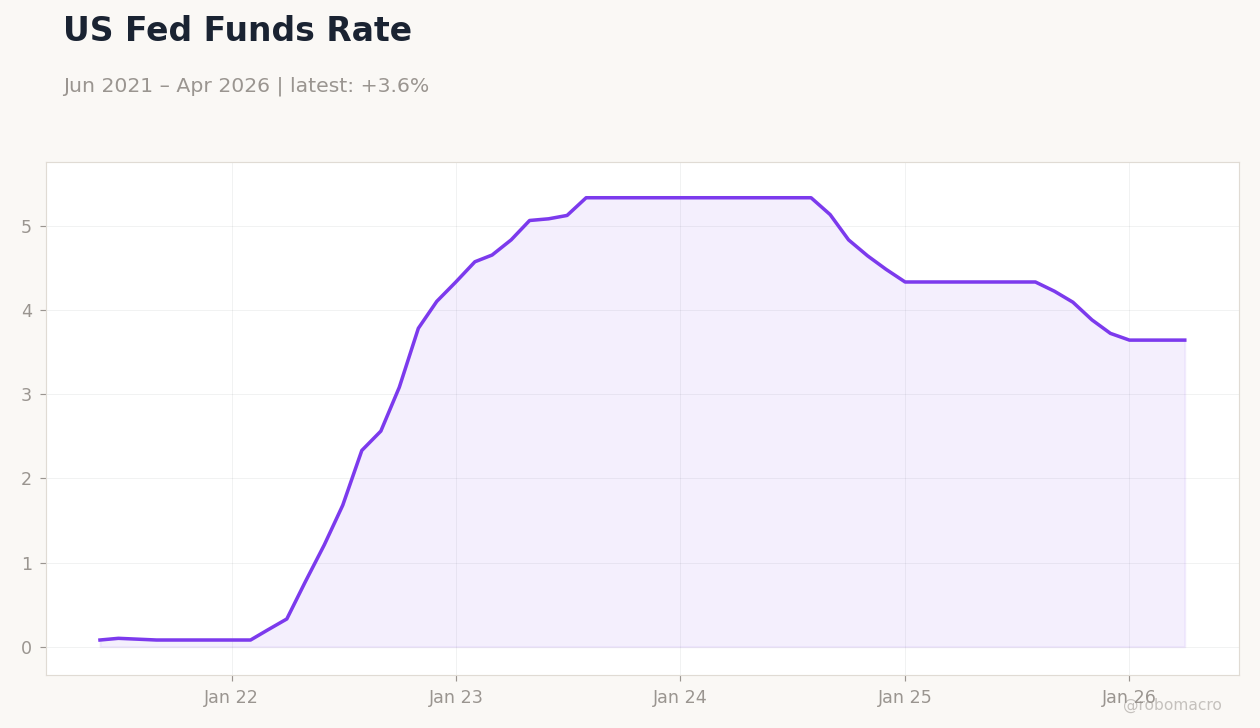

GCC central banks align closely with Fed policy via USD pegs, keeping rates unchanged amid stable interbank rates like SAIBOR and EIBOR. SAMA, CBUAE, QCB, CBK, CBO, and CBB prioritize inflation management and capital stability, with robust FX reserves supported by inflow rebounds. Saudi's deficit prompts SAMA vigilance on fiscal impacts without imminent changes.

Qatar's QCB leverages LNG liquidity, while Oman's CBO and Bahrain's CBB focus on diversification against oil volatility. Kuwait's basket peg allows minor flexibility, as USD/KWD dipped slightly. Overall, synchronized stances limit divergences, with all monitoring Fed cues for potential adjustments.

WTI Crude vs Brent Spread | Type: macro_line | WTI Price (USD/Barrel): 109.8 (2026-05-04) | Range: 55.44–123.6 | Trend(5pt): 64.92,91.29,81.64,73.52,109.8 | Brent Price (USD/Barrel): 118.3 (2026-05-01) | Range: 59.93–138.2 | Trend(5pt): 68.61,97.99,87.55,76.49,118.3

WTI Crude vs Brent Spread | Type: macro_line | WTI Price (USD/Barrel): 109.8 (2026-05-04) | Range: 55.44–123.6 | Trend(5pt): 64.92,91.29,81.64,73.52,109.8 | Brent Price (USD/Barrel): 118.3 (2026-05-01) | Range: 59.93–138.2 | Trend(5pt): 68.61,97.99,87.55,76.49,118.3