GCC Macro Daily(Beta Mode)

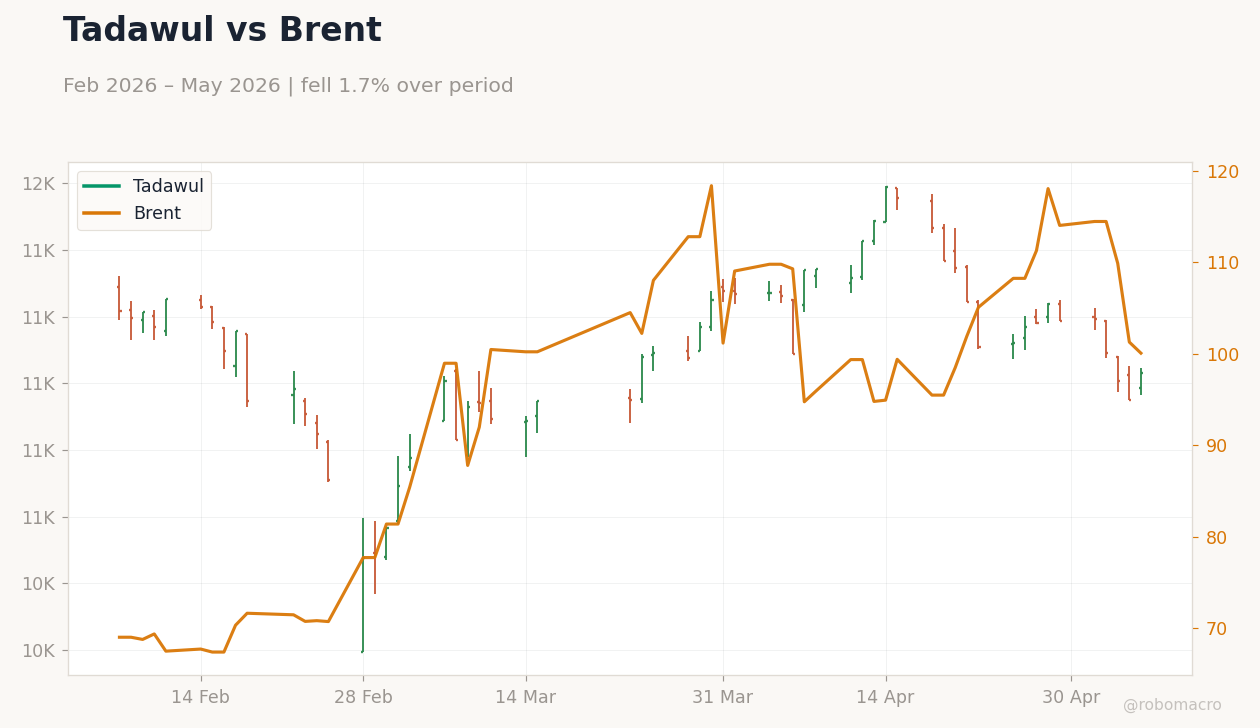

GCC Stocks Rise on Oil Amid Hormuz Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.20 | +0.74% |

| MSCI Saudi | 38.73 | +0.96% |

| MSCI UAE | 19.57 | +0.41% |

| DFM General | 5,902.21 | -0.50% |

| MSCI Qatar | 19.18 | +0.16% |

| MSCI Kuwait | 38.76 | +0.21% |

| Brent Crude | 101.29 | +1.23% |

| WTI Crude | 95.42 | +0.64% |

| Gold | 4,720.40 | +0.44% |

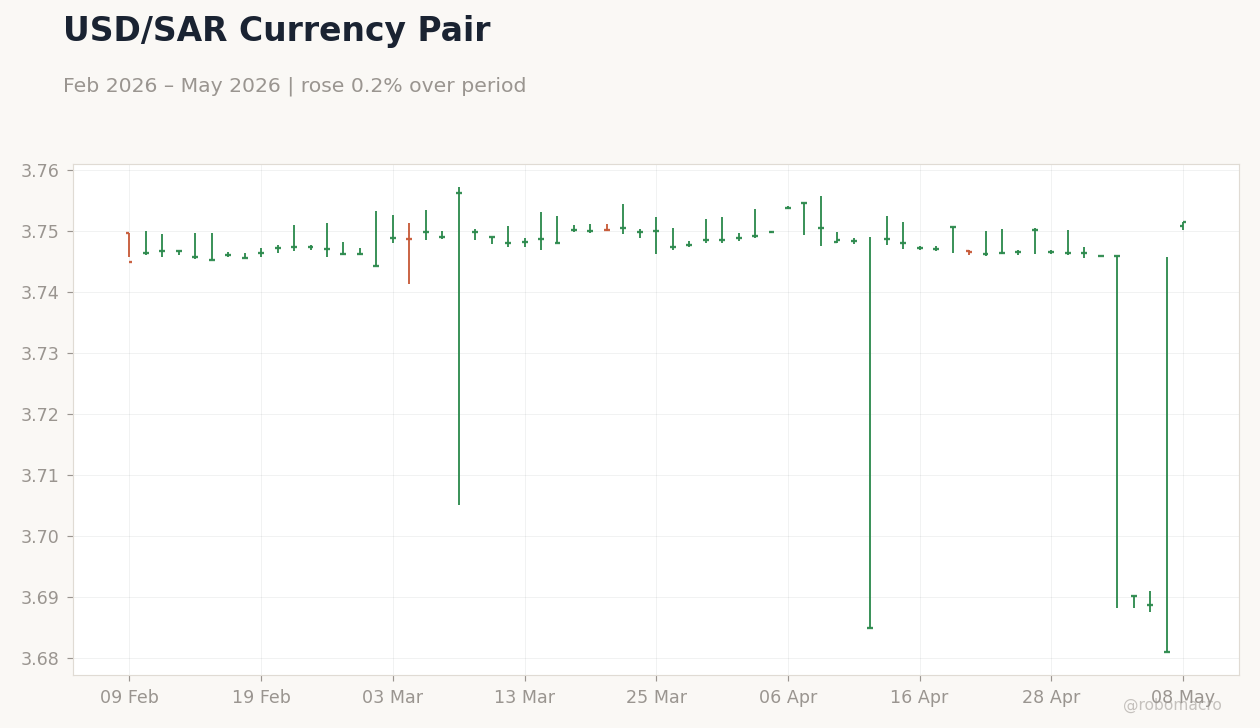

| USD/SAR | 3.75 | +1.91% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.44% |

| Bitcoin | 80,751.46 | +0.70% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

DFM General Index | Type: market_hloc | DFM Index: 5902 (2026-05-08) | Range: 5289–6774 | Trend(6pt): 6774,6197,5518,5930,5932,5902

DFM General Index | Type: market_hloc | DFM Index: 5902 (2026-05-08) | Range: 5289–6774 | Trend(6pt): 6774,6197,5518,5930,5932,5902

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- GCC equities advanced modestly with Brent crude up 1.23% to $101.29, driven by Strait of Hormuz tensions despite continued tanker traffic.

- Saudi Aramco gained 0.74% to 27.20, MSCI Saudi rose 0.96%, reflecting energy sector support from geopolitical risks.

- UAE indices mixed with MSCI UAE +0.41% but DFM -0.50%; Qatar and Kuwait up slightly, FX pegs showed minor shifts.

Yesterday's Recap

GCC equity markets ended May 8 with modest gains, fueled by rising oil prices amid Strait of Hormuz tensions, where Aramco and Adnoc routed crude cargoes despite Iranian threats. Saudi Arabia's Tadawul advanced, with Aramco up 0.74% to 27.20, bolstered by Brent's 1.23% increase to $101.29, emphasizing the kingdom's dependence on energy revenues. UAE markets were uneven, MSCI UAE up 0.41% to 19.57 while DFM General fell 0.50% to 5,902.21, supported by non-oil activities.

Qatar's MSCI index rose 0.16% to 19.18, aided by LNG export resilience as a tanker crossed Hormuz. Kuwait's MSCI gained 0.21% to 38.76, with USD/KWD down 0.44% to 0.31 due to its basket peg. No key economic data was released in the GCC, but sovereign CDS spreads stayed stable, indicating contained risks.

Oil trends prevailed, with WTI up 0.64% to $95.42, highlighting regional vulnerability to chokepoints.

The Day Ahead

No economic data releases are scheduled for May 9 in the GCC, shifting focus to Hormuz traffic monitoring, where disruptions could affect Saudi and UAE exports. Updates on Qatar's LNG shipments will be key, testing the US-Iran ceasefire. Oman and Bahrain may evaluate oil price effects on budgets, given higher breakevens.

Informal OPEC+ talks could arise if Brent volatility continues, impacting Saudi and UAE quotas. Kuwait's central bank may comment on interbank rates amid peg dynamics. The quiet calendar stresses geopolitical oversight over data events.

Other Economic Notes

GCC diversification progresses, with Saudi Vision 2030 boosting non-oil sectors like tourism and tech, though oil income is crucial at current Brent levels. UAE advances in renewables and hydrogen, enhancing its energy transition role despite Hormuz threats. Fiscal breakevens differ—Saudi around $85, higher for Oman and Bahrain—requiring strong crude prices for budget support.

Global Macro News

Oil markets stay volatile from US-Iran clashes straining the Hormuz ceasefire, with Brent's gain adding supply risk premia that aid GCC finances. US added 115,000 jobs in April despite tensions, supporting demand for GCC energy. China's April export records and wider US surplus may sustain Asian appetite for Saudi crude and Qatari LNG.

<i>↓ p.2</i>