GCC Macro Daily(Beta Mode)

Oil Flows Amid Hormuz Tensions

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.20 | +0.74% |

| MSCI Saudi | 38.73 | +0.96% |

| MSCI UAE | 19.57 | +0.41% |

| DFM General | 5,902.21 | -0.50% |

| MSCI Qatar | 19.18 | +0.16% |

| MSCI Kuwait | 38.76 | +0.21% |

| Brent Crude | 105.24 | +3.90% |

| WTI Crude | 99.70 | +4.49% |

| Gold | 4,693.60 | -0.57% |

| USD/SAR | 3.75 | +1.32% |

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.44% |

| Bitcoin | 81,143.59 | +0.59% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

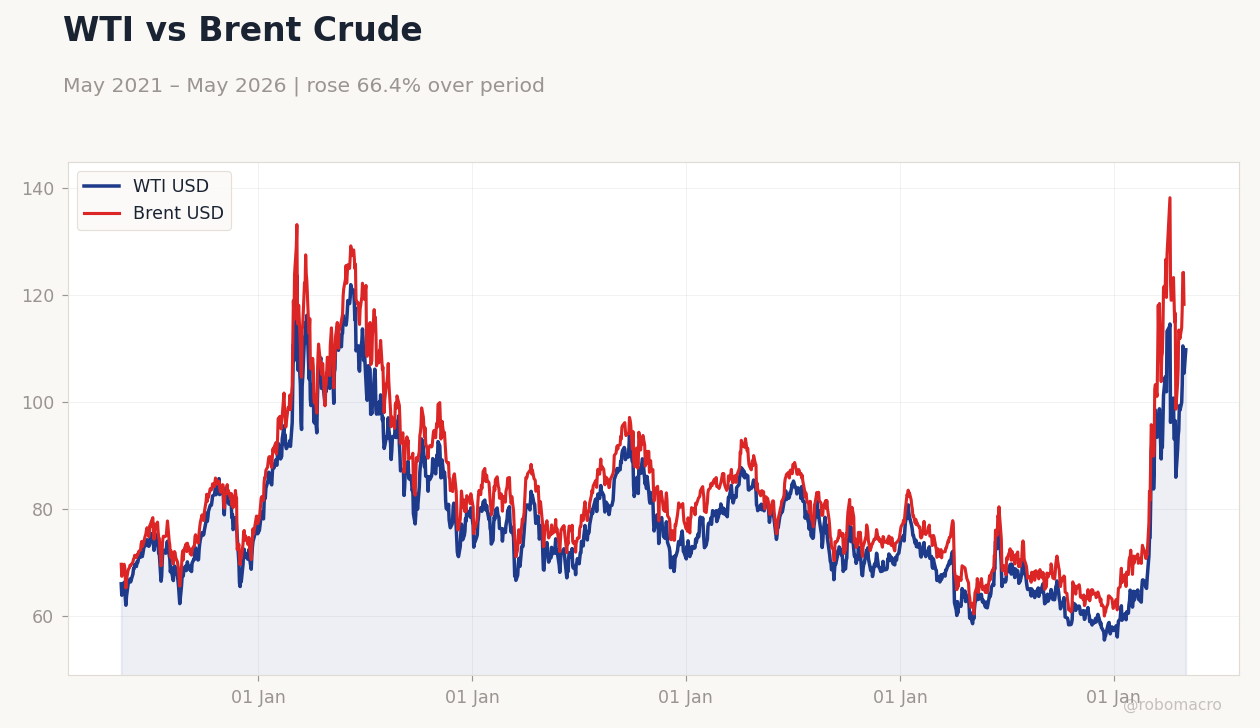

WTI vs Brent Crude | Type: macro_line | WTI USD: 109.8 (2026-05-04) | Range: 55.44–123.6 | Trend(6pt): 65.96,91.77,81.64,72.84,108.6,109.8 | Brent USD: 118.3 (2026-05-01) | Range: 59.93–138.2 | Trend(6pt): 69.62,100.3,87.55,77.11,124.2,118.3

WTI vs Brent Crude | Type: macro_line | WTI USD: 109.8 (2026-05-04) | Range: 55.44–123.6 | Trend(6pt): 65.96,91.77,81.64,72.84,108.6,109.8 | Brent USD: 118.3 (2026-05-01) | Range: 59.93–138.2 | Trend(6pt): 69.62,100.3,87.55,77.11,124.2,118.3

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- GCC oil producers navigated Strait of Hormuz risks, with Aramco and Adnoc shipping crude despite Iranian threats, boosting Brent to $105.24 (+3.90%).

- Regional equities mixed; Saudi Aramco rose 0.74% while DFM General fell 0.50%, reflecting oil gains offsetting broader caution.

- Geopolitical stability held, with no escalations in Red Sea or Yemen, supporting steady FX pegs and interbank rates.

Yesterday's Recap

Saudi Arabia's Aramco Trading Co. successfully moved crude cargoes through the Strait of Hormuz amid Iranian threats, contributing to a 3.90% rise in Brent crude to $105.24, which bolstered fiscal outlooks across the GCC. UAE's Adnoc also shipped oil via the strait, helping MSCI UAE gain 0.41% to 19.57, though the DFM General Index dipped 0.50% to 5,902.21 on profit-taking in non-oil sectors.

Qatar's LNG tanker initiated a Hormuz crossing, aligning with a 0.16% uptick in MSCI Qatar to 19.18, as markets anticipated resumed Gulf shipments. Saudi Aramco shares climbed 0.74% to 27.20, driven by elevated oil prices enhancing dividend prospects, while MSCI Saudi advanced 0.96% to 38.73. Kuwait's MSCI index rose 0.21% to 38.76, supported by stable basket-pegged dinar dynamics despite a -0.44% change in USD/KWD to 0.31.

No major macro data releases occurred across the GCC, keeping focus on energy market resilience. Overall, GCC sovereign CDS spreads remained unchanged, signaling contained risk premia from Hormuz tensions.

The Day Ahead

With no scheduled data releases across the GCC, attention turns to ongoing Strait of Hormuz monitoring, where any Iranian response to US proposals could impact oil transit and prices. Saudi Arabia and UAE may provide updates on refinery operations amid summer demand preparations. Qatar's LNG activities could see informal briefings, with focus on export strategies.

Kuwait's central bank might comment on basket peg stability, given recent USD/KWD fluctuations. Broader GCC equity trading will likely track Brent movements, with Aramco and regional ETFs sensitive to global energy news. Oman and Bahrain remain quiet, but any OPEC+ signals on production cuts could influence fiscal planning.

Other Economic Notes

GCC economies continue prioritizing non-oil diversification, with Saudi Arabia's Vision 2030 advancing through increased energy-transition investments. Fiscal balances benefit from Brent above $100, supporting sovereign wealth funds in Qatar and Kuwait amid steady FX reserves. Broader themes include rising regional refinery runs to meet power demands, while Oman focuses on LNG import strategies to offset gas supply challenges.