GCC Macro Daily(Beta Mode)

GCC Equities Slip on Drone Threats

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.70 | -0.79% |

| MSCI Saudi | 38.29 | -0.62% |

| MSCI UAE | 18.92 | -0.63% |

| DFM General | 5,708.78 | -0.46% |

| MSCI Qatar | 18.68 | -0.37% |

| MSCI Kuwait | 37.96 | -0.33% |

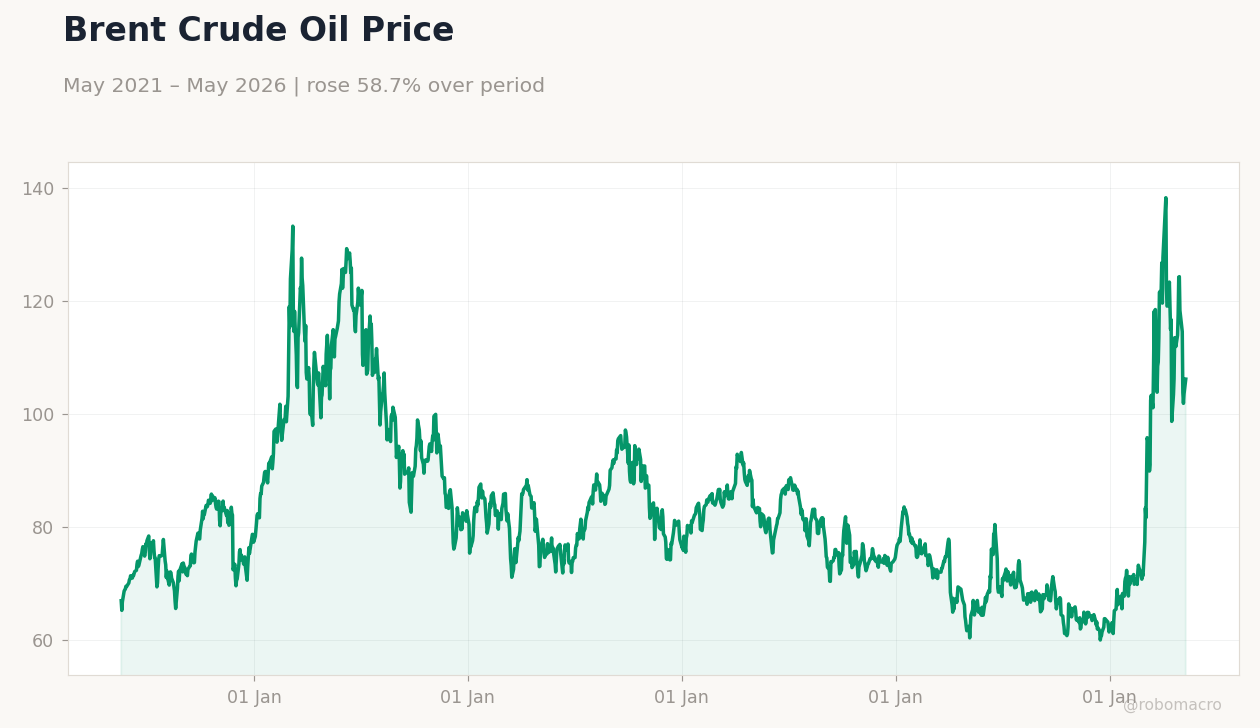

| Brent Crude | 111.31 | +1.88% |

| WTI Crude | 103.27 | -2.04% |

| Gold | 4,535.00 | -0.46% |

| USD/SAR | 3.75 | +1.73% |

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.55% |

| Bitcoin | 76,789.87 | -1.72% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

GCC Oil Export Proxy | Type: macro_line | WTI USD/bbl: 101.6 (2026-05-11) | Range: 55.44–123.6 | Trend(6pt): 63.28,94.86,77.96,71.32,98.38,101.6 | Brent USD/bbl: 106.1 (2026-05-11) | Range: 59.93–138.2 | Trend(6pt): 66.88,103.7,83.66,74.68,103.5,106.1

GCC Oil Export Proxy | Type: macro_line | WTI USD/bbl: 101.6 (2026-05-11) | Range: 55.44–123.6 | Trend(6pt): 63.28,94.86,77.96,71.32,98.38,101.6 | Brent USD/bbl: 106.1 (2026-05-11) | Range: 59.93–138.2 | Trend(6pt): 66.88,103.7,83.66,74.68,103.5,106.1

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Saudi and UAE equities declined modestly amid drone attack condemnations and regional security concerns.

- Brent crude rose 1.88% to $111.31 while WTI fell 2.04%, highlighting supply risk premia.

- Saudi Arabia accelerated blockchain tokenization plans targeting trillions in economic assets by 2030.

Yesterday's Recap

Saudi Arabia and the UAE both condemned drone attacks targeting energy infrastructure and the Barakah nuclear plant perimeter, with Saudi leadership reaffirming solidarity with Abu Dhabi. Regional equity markets posted modest losses, with MSCI Saudi falling 0.62% to 38.29, MSCI UAE down 0.63% to 18.92, and DFM General declining 0.46% to 5,708.78. Saudi Aramco shares dropped 0.79% to 27.70 despite Brent crude climbing to 111.31 on heightened supply concerns.

The MSCI Qatar and MSCI Kuwait indices eased 0.37% and 0.33% respectively. USD/SAR rose 1.73% while USD/KWD fell 0.55%. Saudi authorities advanced plans to tokenize large segments of the economy through a $12.5 billion initiative aimed at bringing trillions on-chain by 2030.

No major macroeconomic data releases occurred across the GCC on May 16.

The Day Ahead

UAE officials are expected to accelerate oil pipeline projects designed to bypass the Strait of Hormuz amid ongoing regional tensions. Saudi Arabia will release further details on its Umrah season calendar for 1448 AH and continue tokenization feasibility work. Qatar’s North Field LNG expansion Phase 2 remains on track for first gas in late 2026.

Kuwait plans to expand its online work-permit renewal system. Broader OPEC+ production caps stay in focus for all six members.

Other Economic Notes

Saudi Arabia’s economy continues to demonstrate resilience through Vision 2030 diversification, attracting both traditional and new partners despite external shocks. UAE efforts to expand non-oil sectors and bypass chokepoints via new pipelines support long-term energy security. Regional sovereign CDS spreads remained stable, reflecting contained risk premia even as geopolitical vigilance stays elevated.

Iraq’s participation in GCC-led pipeline strategies further underscores collective moves to reduce Hormuz exposure.

Global Macro News

Global energy markets face intensifying supply pressure from US-Iran tensions and Houthi activity in the Red Sea. Japan’s energy shock is pushing inflation above GDP growth according to ING analysis. <i>↓ p.2</i>