GCC Macro Daily(Beta Mode)

Oil Rises on Attacks, Saudi Eyes Tokenization

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.70 | -0.79% |

| MSCI Saudi | 38.29 | -0.62% |

| MSCI UAE | 18.92 | -0.63% |

| DFM General | 5,609.58 | -2.19% |

| MSCI Qatar | 18.68 | -0.37% |

| MSCI Kuwait | 37.96 | -0.33% |

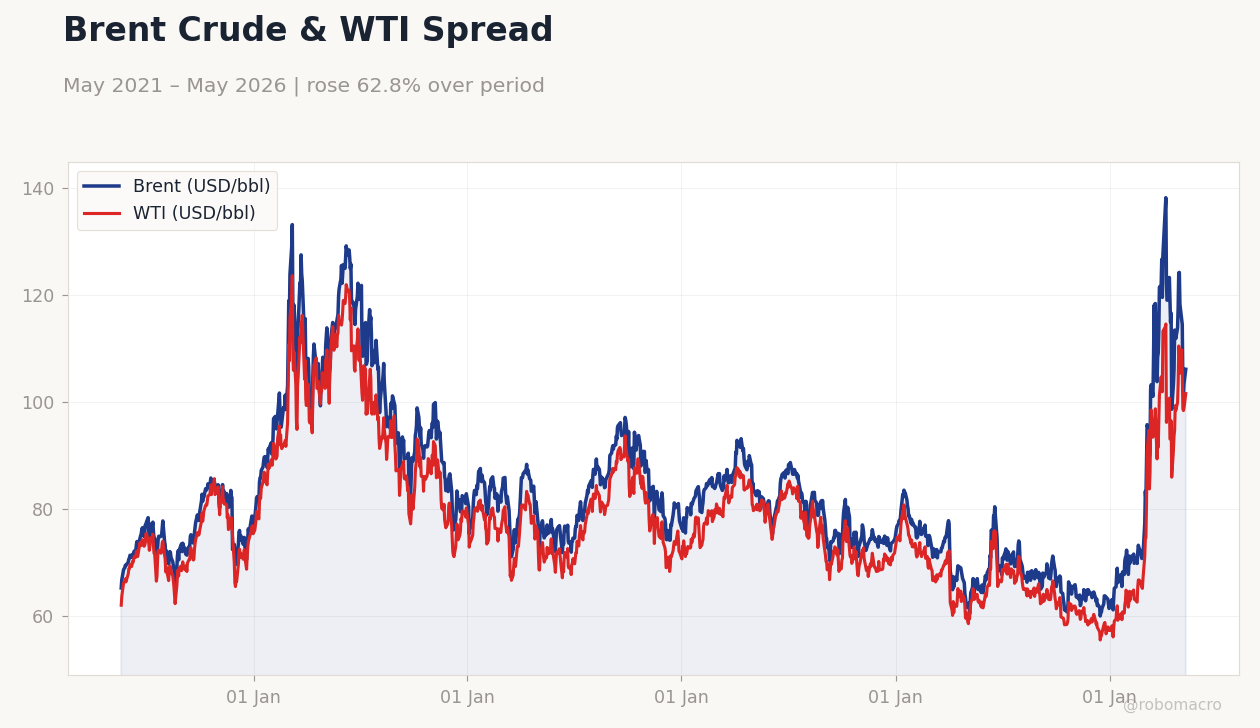

| Brent Crude | 109.86 | +0.55% |

| WTI Crude | 102.84 | -2.45% |

| Gold | 4,553.80 | -0.04% |

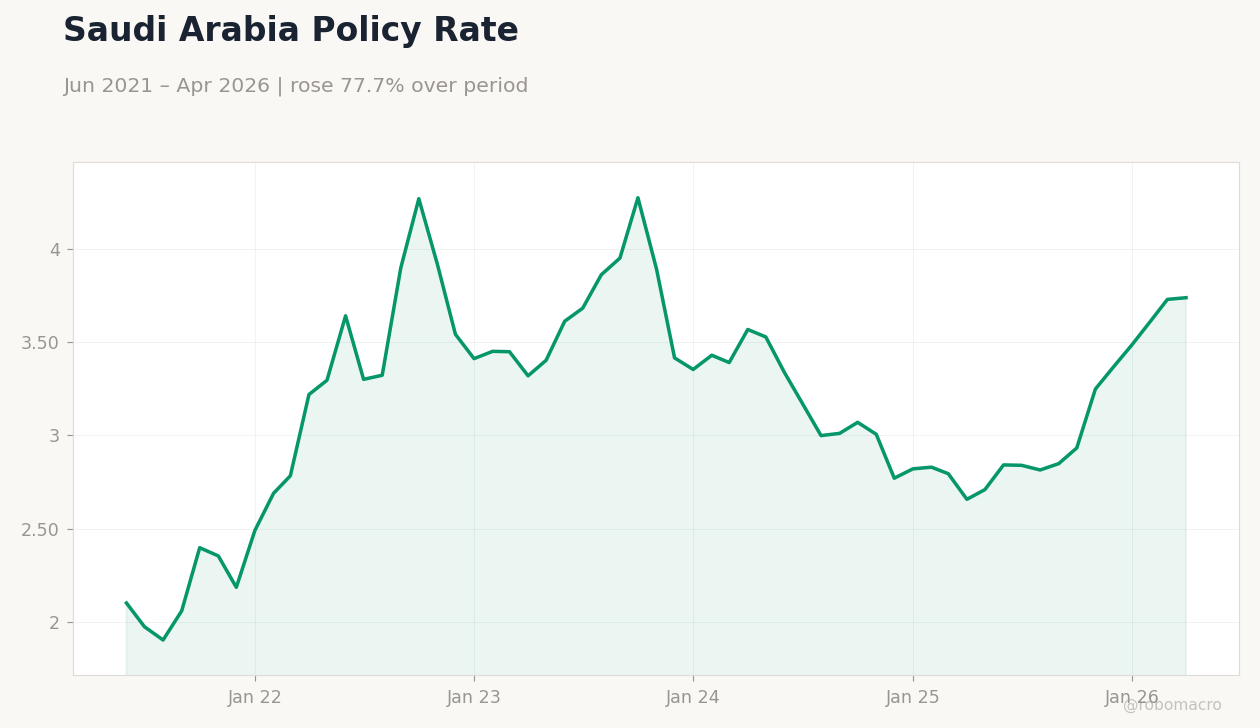

| USD/SAR | 3.75 | -0.34% |

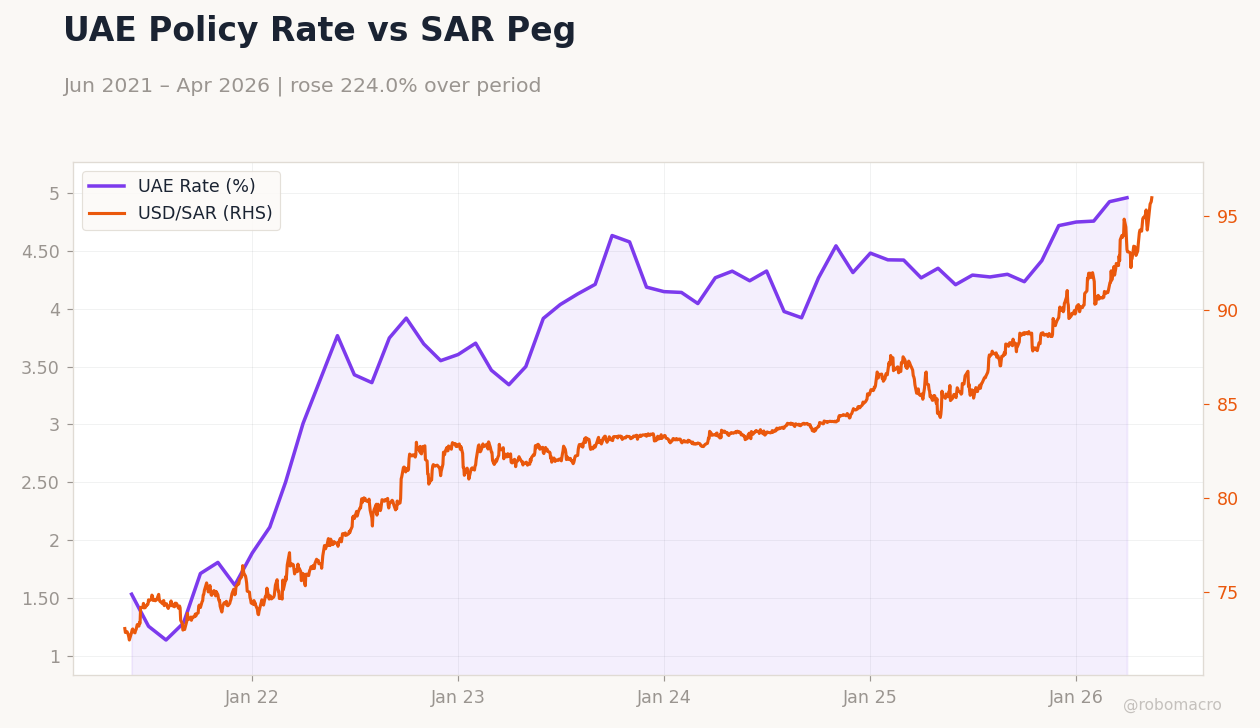

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.47% |

| Bitcoin | 76,534.50 | -1.16% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude & WTI Spread | Type: macro_line | Brent (USD/bbl): 106.1 (2026-05-11) | Range: 59.93–138.2 | Trend(5pt): 65.18,98.25,84.09,76.23,106.1 | WTI (USD/bbl): 101.6 (2026-05-11) | Range: 55.44–123.6 | Trend(6pt): 61.95,92.24,75.85,72.73,98.87,101.6

Brent Crude & WTI Spread | Type: macro_line | Brent (USD/bbl): 106.1 (2026-05-11) | Range: 59.93–138.2 | Trend(5pt): 65.18,98.25,84.09,76.23,106.1 | WTI (USD/bbl): 101.6 (2026-05-11) | Range: 55.44–123.6 | Trend(6pt): 61.95,92.24,75.85,72.73,98.87,101.6

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Drone strikes near UAE nuclear plant and Saudi targets push Brent crude higher on supply concerns.

- Saudi Arabia launches first quantum computer and advances $12.5B tokenization of its economy.

- Regional stock indexes decline while Eid Al Adha confirmed for May 27 amid stable FX pegs.

Yesterday's Recap

Regional markets absorbed geopolitical shocks after drone incidents near Abu Dhabi’s nuclear facility and targets in Saudi Arabia. UAE and Saudi officials condemned the strikes as dangerous escalations. Brent crude rose 0.55 percent to 109.86 dollars per barrel while WTI fell 2.45 percent to 102.84.

Saudi Aramco declined 0.79 percent to 27.70 and MSCI Saudi slipped 0.62 percent; DFM General dropped 2.19 percent. MSCI UAE fell 0.63 percent, MSCI Qatar 0.37 percent and MSCI Kuwait 0.33 percent. Aramco unveiled Saudi Arabia’s first quantum computer.

Riyadh advanced a 12.5 billion dollar tokenization program to modernize capital markets. UAE and Saudi authorities confirmed the moon sighting, setting Dhul Hijjah to begin Monday and Eid Al Adha for 27 May. Riyad Bank partnered with Mastercard on new corporate cards.

GCC currencies held steady with USD/SAR at 3.75 and USD/AED at 3.67. Gold was little changed at 4,553.80 while Bitcoin fell 1.16 percent.

The Day Ahead

Traders will watch for further security statements from UAE and Saudi officials. Volumes are expected to stay light ahead of the Eid Al Adha holiday. Saudi tokenization efforts and Aramco’s quantum project should sustain corporate news flow.

Energy firms will track OPEC+ compliance and any quota adjustments. Investors remain focused on the fiscal effects of Brent prices above 100 dollars for 2026 GCC budgets.

Other Economic Notes

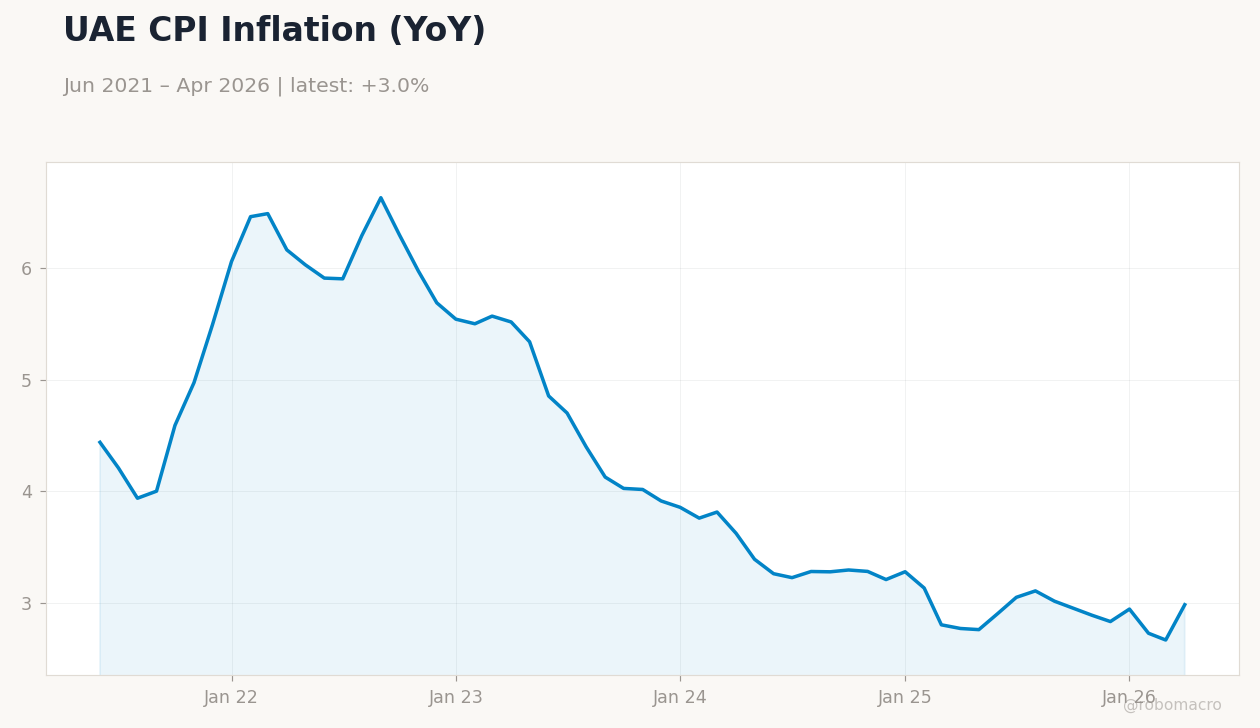

GCC economies continue non-oil diversification under Vision 2030 and UAE 2050 plans, with sovereign funds directing capital into digital infrastructure. Elevated oil prices bolster fiscal balances yet underscore exposure to Strait of Hormuz risks. Iraq and several GCC states are expanding overland pipelines and LNG facilities to ease chokepoint dependence.

Private-sector credit growth receives support from new corporate card products and banking partnerships.

Global Macro News

Energy security worries rose after strikes near UAE nuclear infrastructure, lifting oil volatility and renewing attention on alternative supply routes. <i>↓ p.2</i>