GCC Macro Daily(Beta Mode)

Moody’s Affirms Saudi Aa3 Rating as Brent Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

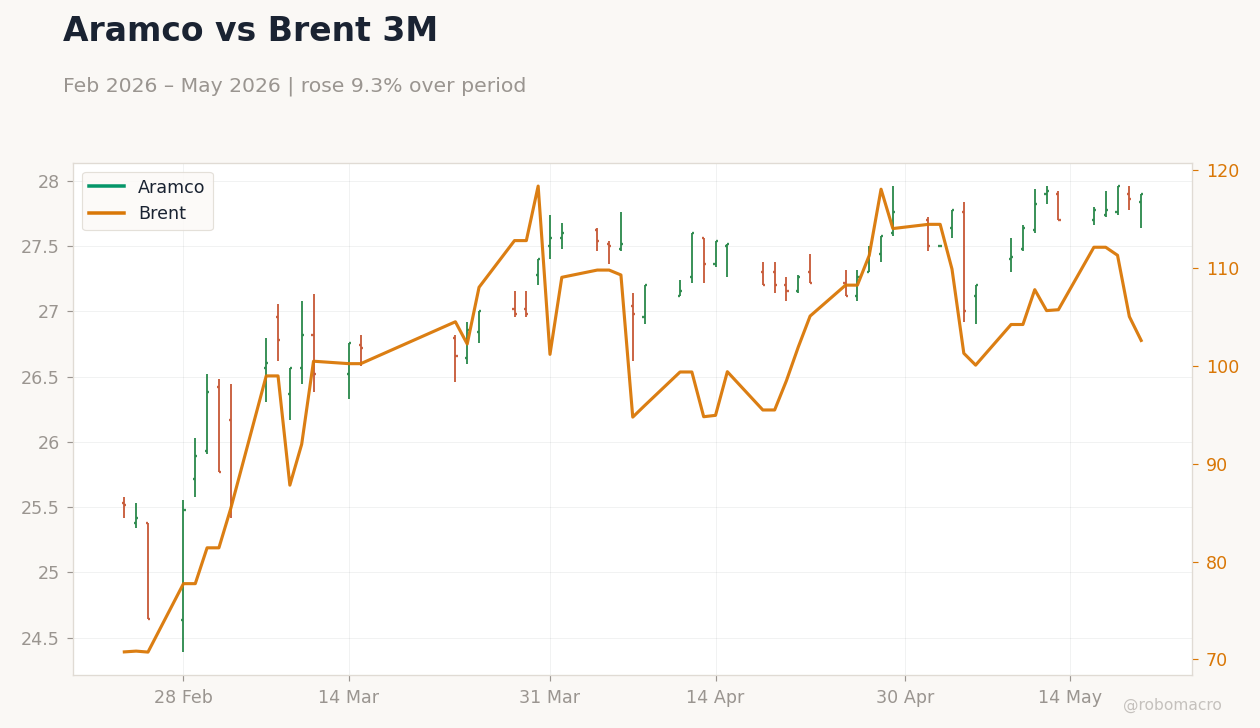

| Saudi Aramco | 27.90 | +0.14% |

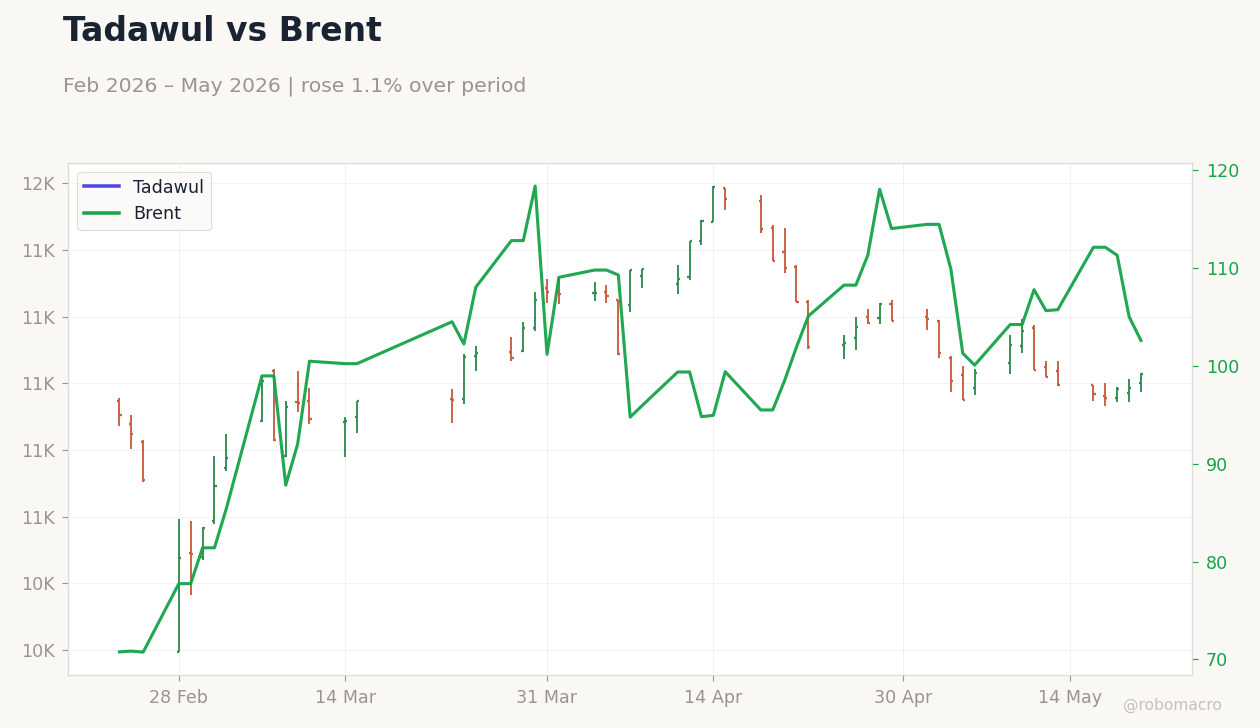

| MSCI Saudi | 38.64 | -0.08% |

| MSCI UAE | 18.92 | -0.71% |

| DFM General | 5,692.82 | +0.57% |

| MSCI Qatar | 18.62 | +0.08% |

| MSCI Kuwait | 37.67 | +0.20% |

| Brent Crude | 100.21 | -3.22% |

| WTI Crude | 96.60 | +0.00% |

| Gold | 4,523.20 | +0.05% |

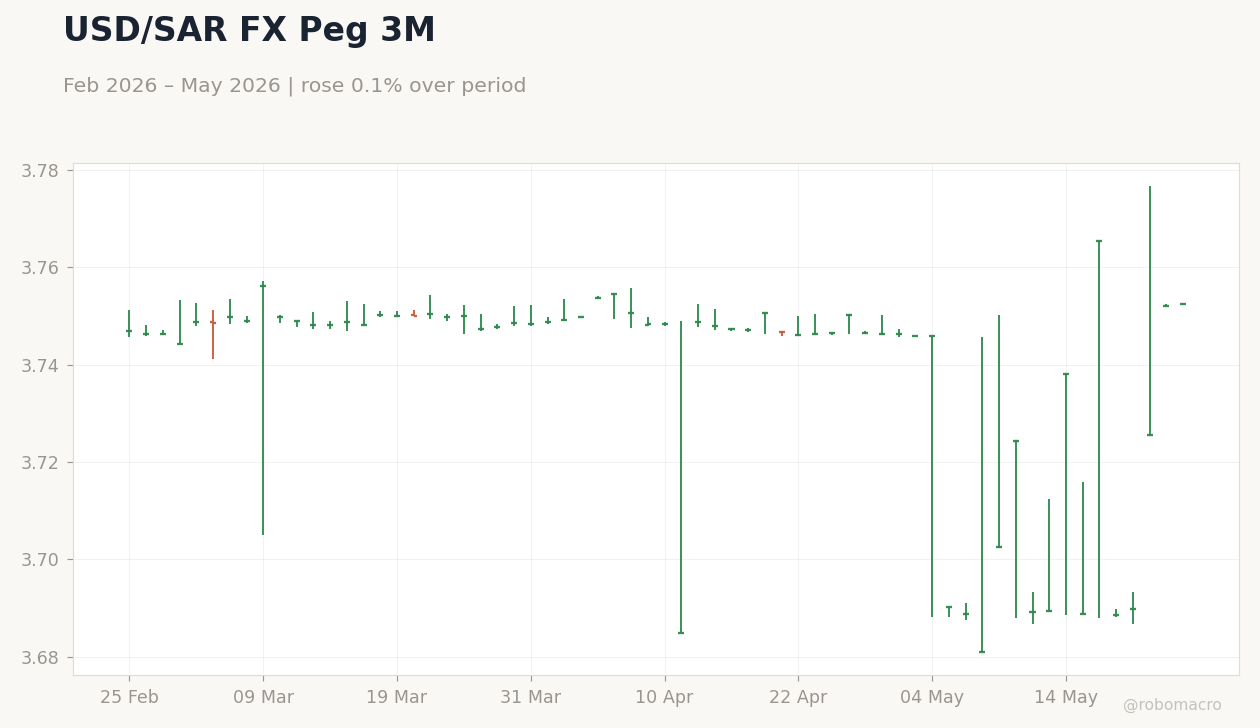

| USD/SAR | 3.75 | +0.01% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.73% |

| Bitcoin | 77,036.48 | +0.47% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/SAR FX Peg 3M | Type: market_hloc | USD/SAR: 3.753 (2026-05-25) | Range: 3.681–3.765 | Trend(5pt): 3.747,3.75,3.748,3.746,3.753

USD/SAR FX Peg 3M | Type: market_hloc | USD/SAR: 3.753 (2026-05-25) | Range: 3.681–3.765 | Trend(5pt): 3.747,3.75,3.748,3.746,3.753

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Moody’s affirms Saudi Arabia’s Aa3 and Kuwait’s A1 ratings with stable outlooks on resilience.

- Brent drops 3.22% to 100.21 while Saudi Aramco rises 0.14% and DFM gains 0.57%.

- GCC FX pegs hold steady with USD/SAR at 3.75 and USD/KWD at 0.31 amid quiet data calendar.

Yesterday's Recap

Saudi equity markets posted modest gains despite the sharp Brent decline, with Aramco advancing to 27.90 on volume and MSCI Saudi easing just 0.08%. The DFM General index climbed 0.57% while MSCI UAE fell 0.71%, reflecting divergent real-estate and banking performance in the UAE. Moody’s affirmed Saudi Arabia’s Aa3 rating, citing sustained non-oil momentum and Vision 2030 progress alongside fiscal buffers.

Kuwait received parallel A1 affirmation from Moody’s, underscoring similar diversification strength. Saudi authorities continue managing inflation pressures tied to regional geopolitical shocks, with price trends diverging across other GCC states. No macro releases emerged from Qatar, Oman or Bahrain.

All currency pegs remained unchanged, including the Kuwaiti dinar’s basket link.

The Day Ahead

The data calendar stays empty across the six GCC economies, shifting attention to Eid Al Adha logistics in the UAE, Qatar and Saudi Arabia. Hajj operations in Saudi Arabia proceed with heat-mitigation measures for pilgrims. Diplomatic engagement continues as Qatar’s emir holds talks with Saudi and UAE leaders on regional stability.

Energy project timelines, including Qatar’s North Field LNG trains and UAE-Saudi overland pipeline coordination with Iraq and Oman, remain on schedule. Markets will monitor any OPEC+ signals ahead of the June JMMC meeting.

Other Economic Notes

Saudi Arabia’s dual oil and non-oil expansion continues to anchor regional growth, supported by Moody’s positive assessment. UAE and Saudi diversification programs advance through green-hydrogen offtake deals and tourism inflows. Inflation management in Saudi Arabia highlights diverging price dynamics within the GCC bloc.

Sovereign credit profiles stay robust, with ample FX reserves backing all peg regimes.

Global Macro News

Brent’s 3.22% drop to 100.21 pressures fiscal balances across oil-dependent GCC states while WTI holds flat. Rising US inflation clouds the Fed path and mechanically constrains GCC monetary settings via dollar pegs. <i>↓ p.2</i>