GCC Macro Daily(Beta Mode)

GCC Equities Rise as Brent Crude Falls

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.90 | +0.00% |

| MSCI Saudi | 38.80 | +0.41% |

| MSCI UAE | 19.12 | +1.11% |

| DFM General | 5,757.48 | +1.71% |

| MSCI Qatar | 18.97 | +1.88% |

| MSCI Kuwait | 38.26 | +1.57% |

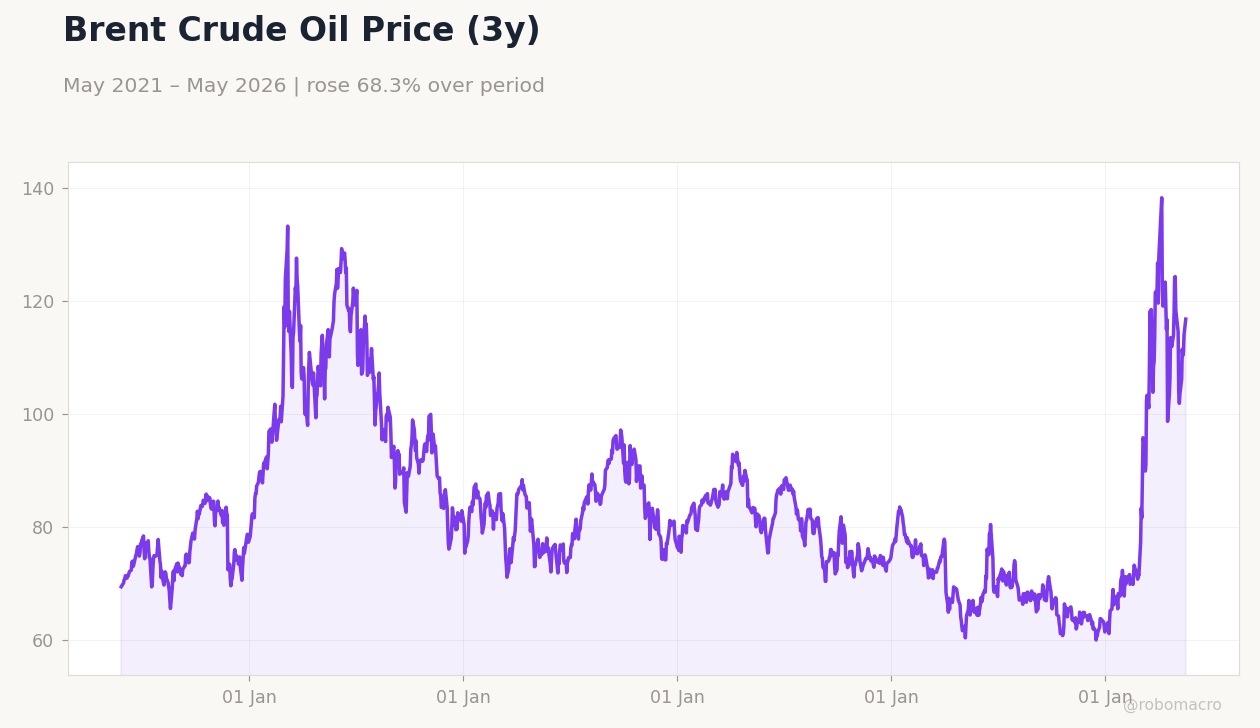

| Brent Crude | 95.37 | -7.89% |

| WTI Crude | 92.35 | -4.40% |

| Gold | 4,502.00 | -0.42% |

| USD/SAR | 3.75 | +2.09% |

| USD/AED | 3.67 | +0.02% |

| USD/KWD | 0.31 | -0.06% |

| Bitcoin | 75,735.58 | -2.00% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

US Industrial Production YoY | Type: macro_line | YoY %: 1.353 (2026-04-01) | Range: -1.558–8.958 | Trend(6pt): 8.958,1.052,-0.7743,-0.2741,0.9907,1.353

US Industrial Production YoY | Type: macro_line | YoY %: 1.353 (2026-04-01) | Range: -1.558–8.958 | Trend(6pt): 8.958,1.052,-0.7743,-0.2741,0.9907,1.353

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI UAE and Qatar indices led regional gains with advances above 1.1% while Brent crude fell sharply to $95.37.

- Saudi non-oil activity remained resilient as Aramco completed its Petronas refinery exit and leisure initiatives advanced.

- UAE aviation and energy firms advanced diversification steps with ENOC signing a cleaner jet-fuel supply agreement.

Yesterday's Recap

GCC equity markets posted broad gains on 25 May. MSCI UAE rose 1.11% and DFM General Index climbed 1.71% as real-estate and banking names attracted flows. MSCI Qatar added 1.88% while MSCI Kuwait gained 1.57%.

Saudi Aramco closed unchanged at 27.90 after the company exited its Malaysian refinery venture with Petronas. Brent crude dropped 7.89% to 95.37 and WTI fell 4.40%, pressuring energy-linked revenues across the region. News flow highlighted Saudi Arabia’s resilient economy on both oil and non-oil fronts, with the General Entertainment Authority launching the Qatif Calendar 2026 to boost tourism and hospitality.

UAE authorities released Eid Al Adha prayer timings and confirmed free parking windows in Dubai during the holiday period.

The Day Ahead

No major data releases are scheduled for 27 May across the six GCC economies. Markets will monitor ongoing Hajj logistics in Saudi Arabia and Eid-related consumption patterns in the UAE. Regional investors will also track tanker movements through the Strait of Hormuz following recent reports of additional Abu Dhabi and Qatari cargoes clearing the waterway.

Any updates on US-Iran talks currently hosted in Qatar could influence near-term risk sentiment. Sovereign wealth fund flows into renewables and hydrogen projects remain on the watch list.

Other Economic Notes

Saudi Arabia continues to advance Vision 2030 non-oil diversification with leisure-economy initiatives gaining traction. UAE energy-transition spending, including ENOC’s cleaner-fuel supply deal, supports long-term aviation decarbonisation targets. Broader GCC fiscal balances remain sensitive to the recent sharp move lower in Brent, which could widen projected 2026 deficits if prices stay below $100.

Healthcare-travel demand across UAE, Saudi Arabia and Oman shows uneven recovery.

Global Macro News

US-Iran negotiations in Doha intensified with senior Iranian officials discussing frozen assets and potential pathways to ease sanctions. Donald Trump publicly urged Saudi Arabia, Qatar and Pakistan to join an expanded Abraham Accords framework tied to any Iran deal. <i>↓ p.2</i>