GCC Macro Daily(Beta Mode)

Saudi Resilience Shines as Oil Slides

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.90 | +0.00% |

| MSCI Saudi | 38.75 | +0.10% |

| MSCI UAE | 19.53 | -0.51% |

| DFM General | 5,757.48 | +1.71% |

| MSCI Qatar | 19.23 | -0.88% |

| MSCI Kuwait | 38.38 | +0.24% |

| Brent Crude | 92.05 | -1.77% |

| WTI Crude | 87.36 | -1.73% |

| Gold | 4,560.50 | +1.36% |

| USD/SAR | 3.75 | +2.03% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.78% |

| Bitcoin | 74,044.27 | +0.92% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

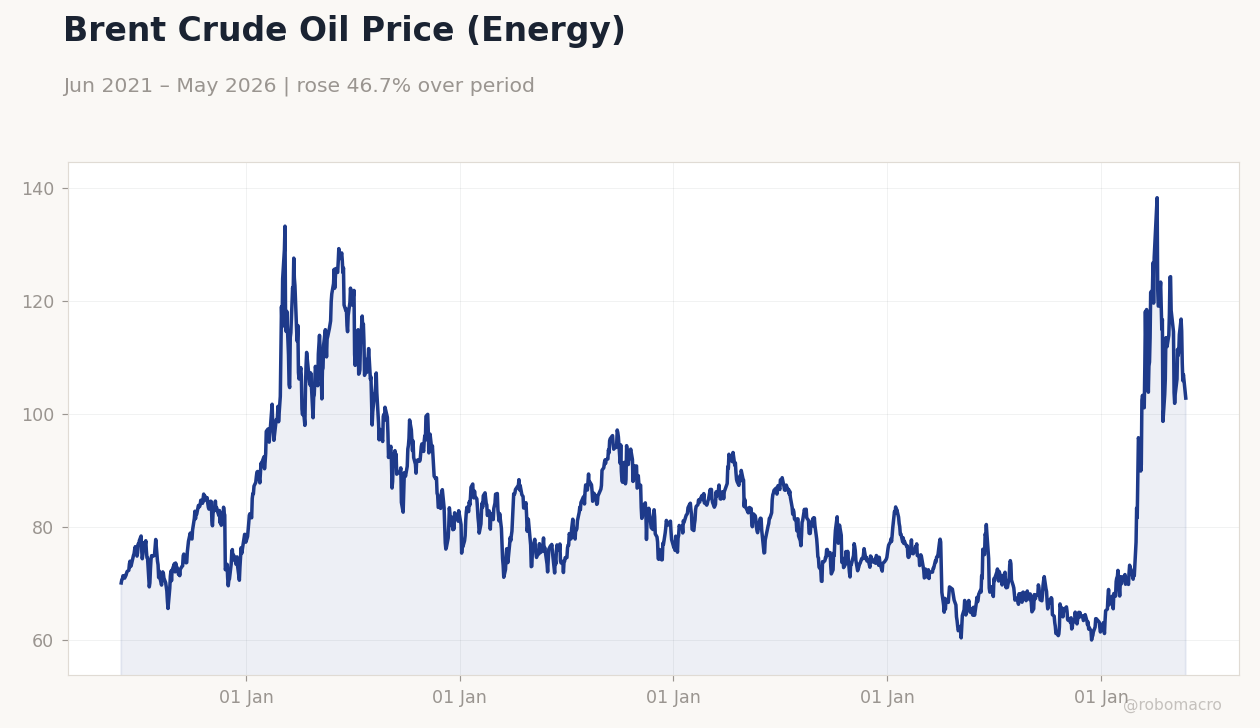

Brent Crude Oil Price (Energy) | Type: macro_line | USD per barrel: 102.8 (2026-05-26) | Range: 59.93–138.2 | Trend(5pt): 70.03,98.81,79.82,74.89,102.8

Brent Crude Oil Price (Energy) | Type: macro_line | USD per barrel: 102.8 (2026-05-26) | Range: 59.93–138.2 | Trend(5pt): 70.03,98.81,79.82,74.89,102.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Saudi Arabia signals readiness for multiple oil price scenarios while declaring Hajj a success

- Regional equities mixed as DFM rises 1.71% but MSCI Qatar falls 0.88%

- Brent crude drops 1.77% to $92.05 amid steady GCC FX pegs

Yesterday's Recap

Saudi Arabia’s economy minister stated the kingdom is prepared for varied oil price outcomes, underscoring fiscal buffers built through Vision 2030 diversification. No macro data releases occurred across the GCC yesterday. Equity markets showed divergence, with the DFM General Index climbing 1.71% to 5,757.48 while MSCI UAE slipped 0.51% to 19.53 and MSCI Qatar declined 0.88% to 19.23.

Brent and WTI crude fell 1.77% and 1.73% respectively to $92.05 and $87.36 on easing supply concerns. Gold advanced 1.36% to $4,560.50 as a safe-haven bid emerged. USD/SAR held at 3.75 while USD/KWD eased 0.78% to 0.31, keeping all GCC pegs intact.

News flow centered on Saudi Arabia’s successful 1447 AH Hajj season and ongoing non-oil growth momentum, including rising interest in venture debt among Saudi startups.

The Day Ahead

The GCC calendar remains empty today with no CPI, PMI or trade releases scheduled for any member state. Markets will monitor ongoing OPEC+ compliance and Saudi voluntary cuts of 1 mb/d. Attention stays on oil price trajectories and their direct impact on fiscal balances across all six economies.

UAE non-oil diversification under the 2050 strategy and Qatar’s North Field LNG expansion continue to draw investor focus. Regional equity turnover is expected to stay average absent fresh catalysts. Saudi Arabia’s statements on multiple oil price scenarios provide a steady policy anchor.

Other Economic Notes

Saudi Arabia continues to demonstrate economic resilience through non-oil sector expansion despite oil price swings. Venture debt is gaining traction among Saudi startups as an alternative to equity financing. Broader GCC efforts to attract foreign investment in renewables and hydrogen remain on track.

Fiscal buffers in Saudi Arabia and the UAE provide room to navigate lower oil revenues without immediate spending cuts. Yemen’s PLC expressed gratitude for the latest Saudi grant, reinforcing regional stability ties.

Global Macro News

Oil prices steadied as markets await a possible US-Iran ceasefire that could ease supply risks. Japan’s inflation slowed sharply, raising questions about energy import costs for Asian buyers of GCC crude. <i>↓ p.2</i>