GCC Macro Daily(Beta Mode)

Oil Rises Sharply as GCC Equities Trade Mixed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.90 | +0.00% |

| MSCI Saudi | 38.75 | +0.10% |

| MSCI UAE | 19.53 | -0.51% |

| DFM General | 5,774.90 | +0.30% |

| MSCI Qatar | 19.23 | -0.88% |

| MSCI Kuwait | 38.38 | +0.24% |

| Brent Crude | 94.75 | +2.93% |

| WTI Crude | 91.83 | +5.12% |

| Gold | 4,504.80 | -1.22% |

| USD/SAR | 3.75 | +0.66% |

| USD/AED | 3.67 | +0.01% |

| USD/KWD | 0.31 | -0.73% |

| Bitcoin | 70,746.68 | -3.85% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

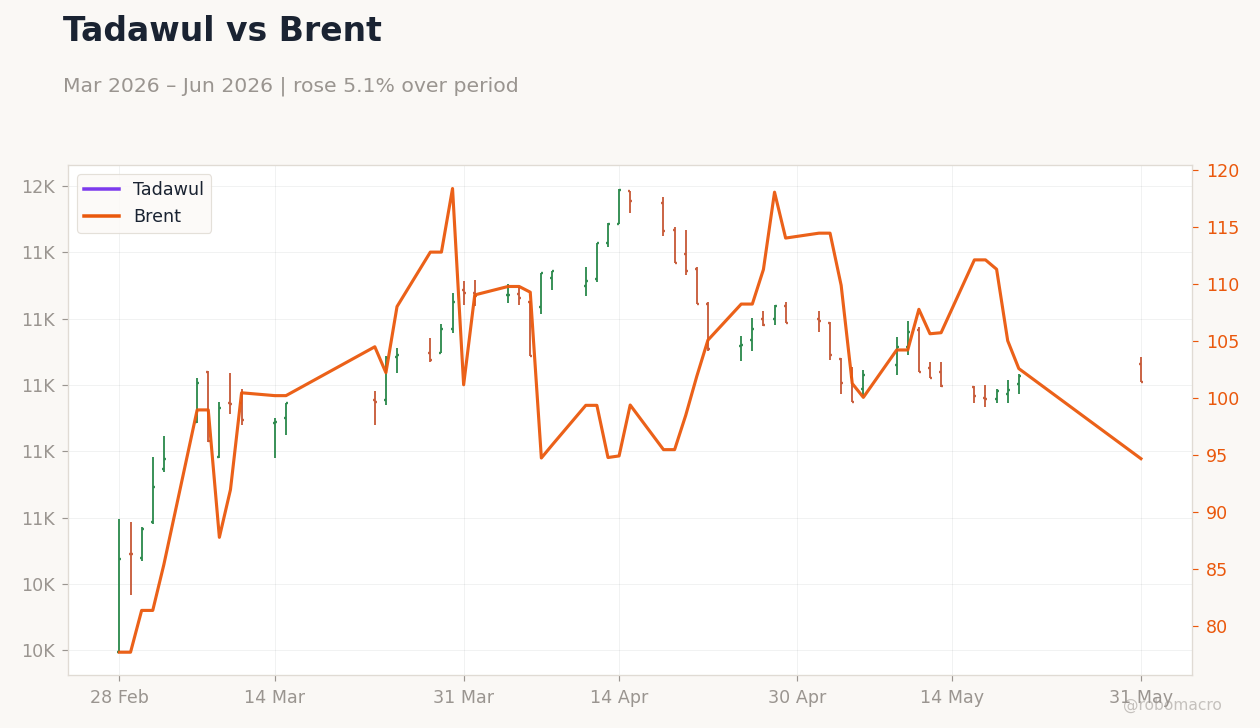

Brent Crude Oil Price (3Y) | Type: macro_line | USD per barrel: 102.8 (2026-05-26) | Range: 59.93–138.2 | Trend(6pt): 70.71,101.1,79.82,74.88,106.9,102.8

Brent Crude Oil Price (3Y) | Type: macro_line | USD per barrel: 102.8 (2026-05-26) | Range: 59.93–138.2 | Trend(6pt): 70.71,101.1,79.82,74.88,106.9,102.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Brent crude jumped 2.93% to $94.75/bbl while WTI rose 5.12% to $91.83/bbl on supply concerns.

- UAE 2025 GDP expanded 6.2% to $517bn, driven by non-oil sectors.

- Saudi economy minister signals readiness for varied oil-price scenarios as equities trade mixed.

Yesterday's Recap

GCC equity markets closed mixed on 31 May. Saudi Aramco held steady at 27.90 while MSCI Saudi edged up 0.10%. DFM General gained 0.30% but MSCI UAE slipped 0.51% and MSCI Qatar fell 0.88%.

MSCI Kuwait rose 0.24%. Saudi Arabia’s economy minister stated the kingdom is prepared for multiple oil-price outcomes, underscoring fiscal resilience. UAE non-oil expansion continued to support overall GDP growth.

Regional FX pegs remained stable with USD/SAR at 3.75 and USD/AED at 3.67. Saudi Arabia condemned Israeli aggression against Lebanon and strongly condemned Iranian attacks against Kuwait. Qatar congratulated Saudi Arabia on the success of the Hajj season.

Saudi Arabia opened visa applications for the new Umrah season and deported 7,466 illegal residents in a one-week crackdown while launching early preparations for the 2027 Hajj season. More than 1,000 athletes will take part in the UAE Games 2026 in Abu Dhabi. Dubai company introduced adoption leave and offers 85 days paid maternity leave.

A Dubai humanoid robot joined worshippers for Eid prayer. Arab Parliament condemned Iranian attacks on Kuwait. South Korea joined other nations confronting flight chaos and tourism losses from West Asia conflict.

Oil steadied as markets awaited possible US-Iran ceasefire. Saudi Arabia and UAE became Uzbekistan’s key partners in renewable energy projects.

The Day Ahead

No major data releases are scheduled across the GCC on 1 June. Markets will monitor Brent and WTI price action closely given their direct impact on fiscal balances. OPEC+ production discipline and any signals ahead of the June JMMC meeting remain in focus.

Regional equity volumes are expected to stay light amid the holiday-shortened week. Sovereign CDS levels in Saudi Arabia and the UAE should hold steady absent fresh geopolitical shocks.

Other Economic Notes

Saudi Arabia continues to demonstrate economic resilience through non-oil diversification under Vision 2030. UAE GDP outperformance highlights successful expansion in tourism, finance and renewables. <i>↓ p.2</i>