GCC Macro Daily(Beta Mode)

Oil Surges as GCC Equities Diverge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.16 | -0.37% |

| MSCI Saudi | 37.44 | -2.35% |

| MSCI UAE | 18.50 | -1.86% |

| DFM General | 5,767.77 | +0.86% |

| MSCI Qatar | 18.62 | -1.17% |

| MSCI Kuwait | 37.83 | -0.17% |

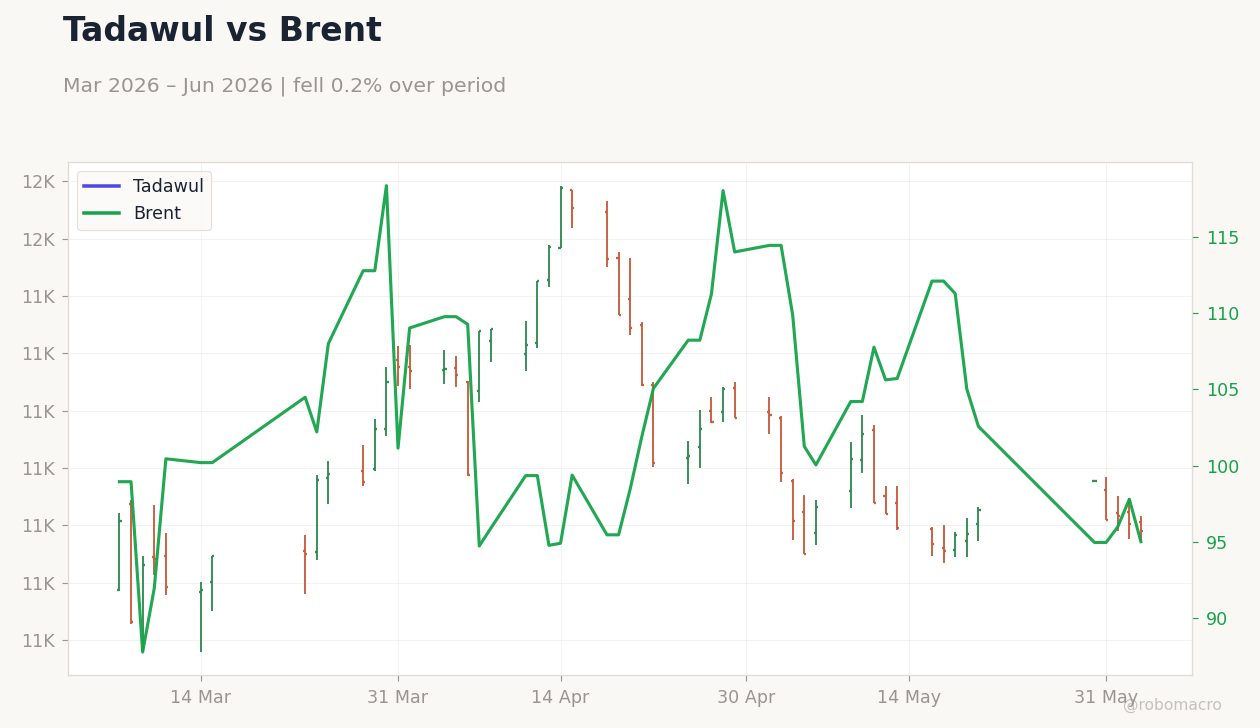

| Brent Crude | 96.17 | +3.31% |

| WTI Crude | 93.45 | +3.21% |

| Gold | 4,341.20 | +0.09% |

| USD/SAR | 3.75 | +1.69% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.48% |

| Bitcoin | 63,083.28 | +3.64% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude 3M | Type: market_hloc | USD/bbl: 96.57 (2026-06-07) | Range: 87.8–118.3 | Trend(5pt): 98.96,118.3,105.1,109.3,96.57

Brent Crude 3M | Type: market_hloc | USD/bbl: 96.57 (2026-06-07) | Range: 87.8–118.3 | Trend(5pt): 98.96,118.3,105.1,109.3,96.57

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Brent crude jumped 3.31% to $96.17/bbl, lifting fiscal outlooks across GCC producers.

- Saudi equities fell sharply with MSCI Saudi down 2.35%, while DFM General rose 0.86%.

- USD/SAR held at the 3.75 peg and USD/AED at 3.67, confirming continued monetary alignment.

Yesterday's Recap

GCC markets showed clear divergence on 6 June. Saudi Aramco fell 0.37% to 27.16 and MSCI Saudi dropped 2.35%, reflecting profit-taking after recent gains. In contrast, DFM General advanced 0.86% while MSCI UAE eased 1.86%.

Brent and WTI both rose over 3%, directly supporting Saudi and UAE fiscal balances. USD/SAR printed 3.75 and USD/AED 3.67, remaining locked to their respective pegs. USD/KWD eased 0.48% to 0.31, staying inside the basket band.

No macro data releases occurred in any GCC country. Equity volumes stayed average outside Aramco. Gold rose 0.09% to 4,341.20 while Bitcoin gained 3.64% to 63,083.28 with limited regional portfolio impact.

The Day Ahead

No scheduled data releases or central-bank meetings appear for 7 June across the six GCC states. Markets will track ongoing OPEC+ output adjustments and any fresh signals on North Field LNG timelines. Saudi diversification updates from the OECD meeting in Paris may draw follow-up commentary.

Regional equity flows are expected to remain sensitive to Brent above $95. Quiet trading is likely unless geopolitical headlines emerge.

Other Economic Notes

Saudi Arabia’s waqf framework and first coffee city in Baha continue to support non-oil growth under Vision 2030. Hotel pipeline data confirm the kingdom leads Middle East development, adding construction and tourism jobs. UAE health-and-wellness tourism initiatives are expanding in parallel with Saudi efforts.

Remittance outflows from UAE, Qatar and Bahrain have slowed amid regional uncertainty, easing pressure on current accounts. Japan reaffirmed support for future Saudi projects while the IMF highlighted the kingdom’s economic resilience. KSrelief distributed 25,000 hot meals in Gaza and an environmental-protection MoU was signed with Russia.

Global Macro News

OPEC+ approved a modest 188,000 b/d production increase, providing a mild supply-side offset to recent price strength. The US Fed leadership transition introduces uncertainty over the pace of future rate moves that mechanically affect GCC policy. <i>↓ p.2</i>