GCC Macro Daily(Beta Mode)

Saudi GDP Expands 3% Led by Non-Oil Sectors

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.16 | +0.00% |

| MSCI Saudi | 38.81 | +1.36% |

| MSCI UAE | 18.77 | +0.37% |

| DFM General | 5,734.81 | +0.29% |

| MSCI Qatar | 18.59 | +1.86% |

| MSCI Kuwait | 37.27 | -0.00% |

| Brent Crude | 92.07 | -2.31% |

| WTI Crude | 88.75 | -2.79% |

| Gold | 4,210.50 | -2.89% |

| USD/SAR | 3.75 | +1.78% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.55% |

| Bitcoin | 61,257.79 | -2.91% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

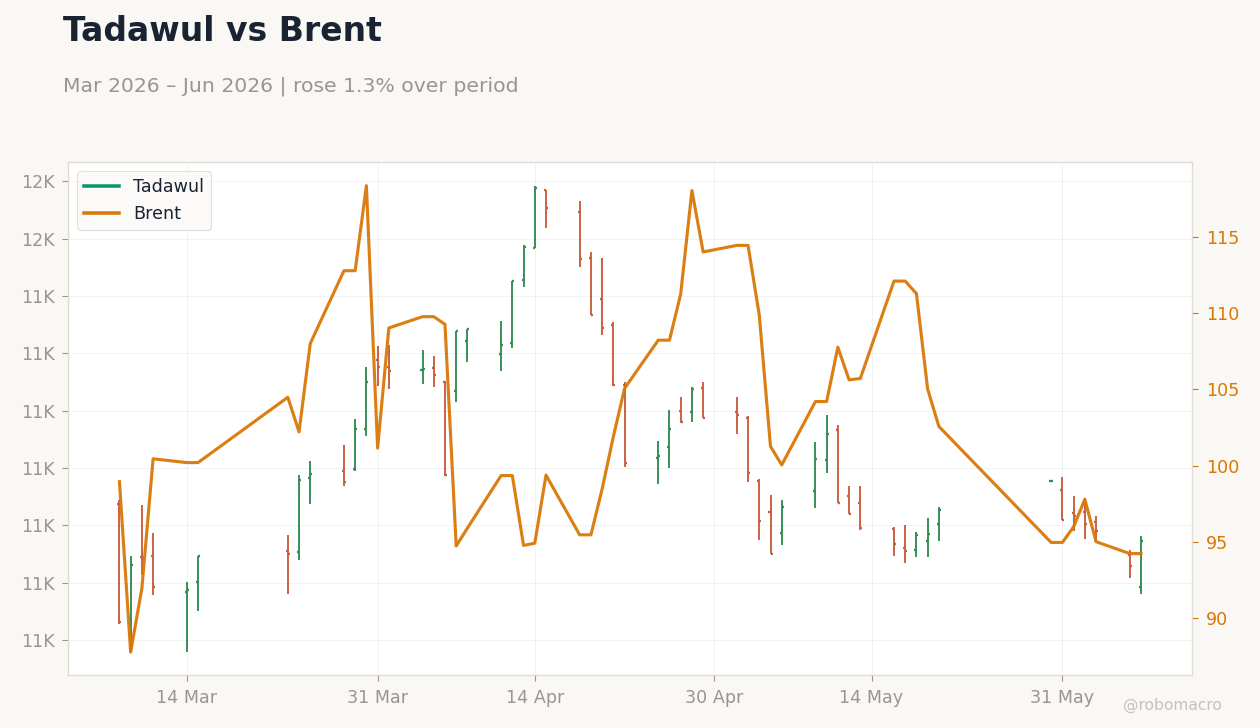

Brent Crude 3M | Type: market_hloc | Price USD: 92.15 (2026-06-09) | Range: 87.8–118.3 | Trend(5pt): 98.96,118.3,105.1,109.3,92.15

Brent Crude 3M | Type: market_hloc | Price USD: 92.15 (2026-06-09) | Range: 87.8–118.3 | Trend(5pt): 98.96,118.3,105.1,109.3,92.15

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Saudi Arabia posted 3% real GDP growth in Q1 2026, driven by non-oil sectors and government operations rebound.

- Regional equities advanced with MSCI Saudi up 1.36% and MSCI Qatar gaining 1.86%, while Brent crude fell 2.31% to $92.07.

- GCC FX pegs remained stable amid lower oil prices and quiet central bank policy stance.

Yesterday's Recap

Saudi Arabia’s economy expanded 3% year-on-year in Q1 2026, with non-oil activities leading the expansion and government operations contributing to the rebound. Equity markets closed higher across most GCC bourses, led by Saudi Arabia where MSCI Saudi rose 1.36% and the DFM General index added 0.29%. Qatar equities outperformed with MSCI Qatar climbing 1.86%, while Kuwait remained flat.

Oil prices declined sharply, with Brent dropping 2.31% to $92.07 per barrel and WTI falling 2.79% to $88.75, reflecting softer global demand signals. Gold prices retreated 2.89% to $4,210.50 per ounce. Currency pegs held steady, with USD/SAR at 3.75 and USD/AED at 3.67, while USD/KWD eased 0.55%.

No major data releases occurred across the GCC on June 8.

The Day Ahead

No major economic releases are scheduled for GCC markets on June 9. Attention will remain on oil price movements and their implications for fiscal balances in Saudi Arabia and the UAE. Regional investors may monitor any updates ahead of the June OPEC+ ministerial meeting.

Equity trading volumes are expected to stay moderate following yesterday’s gains in Saudi and Qatari indices. Broader sentiment will hinge on global crude demand indicators and any developments in non-oil diversification projects.

Other Economic Notes

Saudi Arabia’s non-oil sector continues to expand under Vision 2030 initiatives, supporting overall GDP resilience despite lower oil realizations. UAE diversification efforts under the 2050 strategy remain on track, with real-estate and banking sectors providing steady equity support. Food security cooperation advanced as Saudi Arabia signed 13 strategic deals with Russia worth $1.28 billion.

Broader GCC economies benefit from stable peg arrangements that anchor inflation expectations amid global commodity volatility.

Global Macro News

Lower oil prices weighed on energy-linked assets across the GCC, with Brent’s 2.31% decline pressuring near-term fiscal revenue projections for Saudi Arabia and Oman. Global equity sentiment softened alongside Bitcoin’s 2.91% drop, reflecting risk-off flows that also pushed gold lower. <i>↓ p.2</i>