GCC Macro Daily(Beta Mode)

Saudi Q1 Growth Hits 3% as Oil Climbs

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.06 | -0.37% |

| MSCI Saudi | 38.67 | +0.35% |

| MSCI UAE | 18.74 | +1.24% |

| DFM General | 5,785.24 | +0.88% |

| MSCI Qatar | 18.64 | +0.32% |

| MSCI Kuwait | 37.88 | -0.00% |

| Brent Crude | 94.57 | +3.41% |

| WTI Crude | 91.74 | +4.01% |

| Gold | 4,077.60 | -4.28% |

| USD/SAR | 3.75 | +1.70% |

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.52% |

| Bitcoin | 62,072.09 | +0.69% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

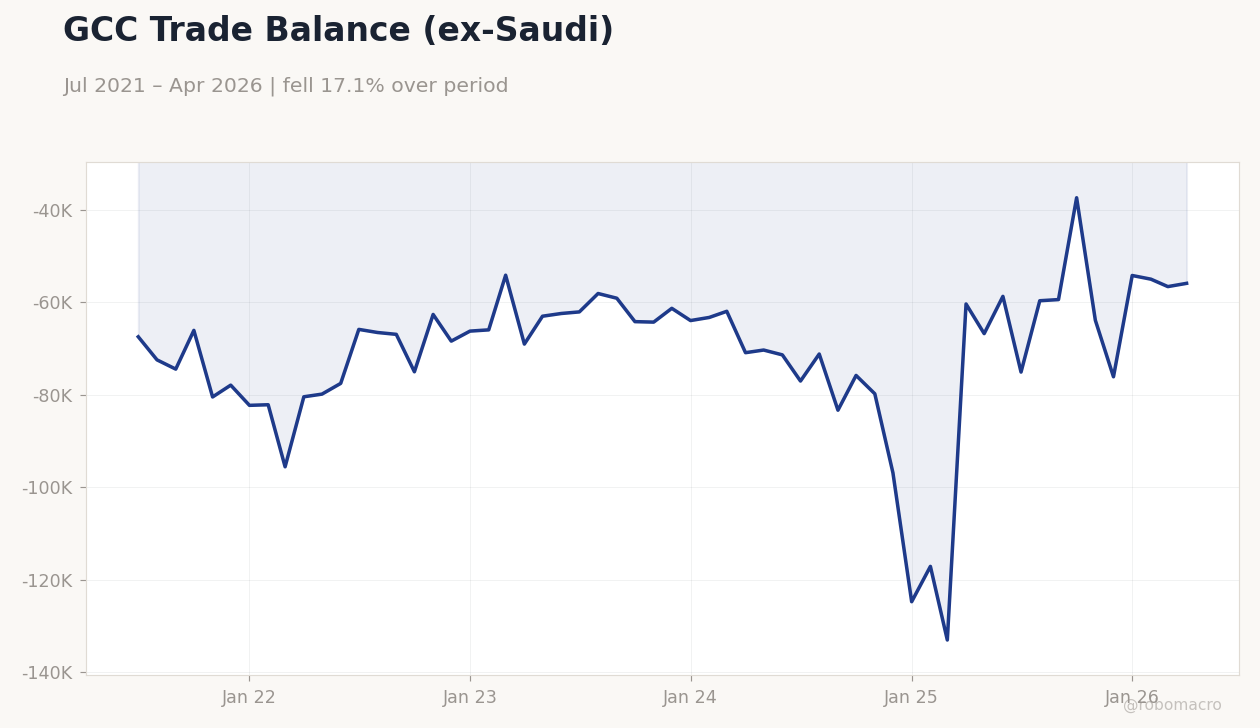

GCC Trade Balance (ex-Saudi) | Type: macro_line | USD bn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

GCC Trade Balance (ex-Saudi) | Type: macro_line | USD bn: -5.588e+04 (2026-04-01) | Range: -1.33e+05–-3.738e+04 | Trend(6pt): -6.744e+04,-6.691e+04,-6.426e+04,-1.247e+05,-5.658e+04,-5.588e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Saudi Arabia posts 3% Q1 GDP growth led by non-oil sectors

- MSCI UAE jumps 1.24% while Brent crude climbs 3.41%

- Regional equities advance on stable pegs and higher energy prices

Yesterday's Recap

Saudi Arabia reported 3% real GDP growth for Q1 2026, with non-oil activities providing the main expansion driver as oil sector output remained constrained. Equity markets responded positively, with MSCI UAE rising 1.24% and DFM General Index gaining 0.88%. MSCI Saudi advanced 0.35% while Aramco shares fell 0.37% to 27.06 despite Brent crude rising 3.41% to 94.57 dollars per barrel.

WTI crude also rose sharply, up 4.01% to 91.74 dollars. Gold declined 4.28% to 4,077.60 dollars per ounce. USD/SAR held at the 3.75 level while USD/KWD eased 0.52%.

No major data releases occurred across the other GCC states. Saudi Arabia and Türkiye signed railway and transport cooperation agreements. Qatar expanded national service eligibility to certain residents and children of Qatari mothers.

The Day Ahead

No scheduled macroeconomic releases appear on calendars for Saudi Arabia, UAE, Qatar, Kuwait, Oman or Bahrain. Markets will monitor OPEC+ compliance signals ahead of the late-June meeting and any updates on North Field LNG expansion timelines from QatarEnergy. Regional investors may track follow-through on Saudi-Türkiye railway cooperation agreements signed earlier this week.

Equity volumes on Tadawul and DFM are expected to remain elevated given the recent oil price strength. Attention will also stay on Red Sea shipping developments and their potential impact on energy supply risk premia.

Other Economic Notes

Saudi Arabia’s non-oil economy continues to expand under Vision 2030 initiatives, with the latest GDP print confirming resilience despite softer oil activities. Broader GCC diversification efforts remain on track, supported by higher energy revenues that bolster fiscal buffers and project financing. Domestic tourism within the region is shielding visitor numbers from international slowdowns linked to ongoing conflicts.

Sovereign credit spreads stayed contained, reflecting market confidence in peg sustainability and reserve adequacy.

Global Macro News

Brent and WTI crude prices posted sharp gains on supply concerns tied to Middle East tensions and steady OPEC+ production discipline. US gas price increases have rekindled domestic inflation worries, indirectly supporting higher energy export receipts for GCC producers. <i>↓ p.2</i>