GCC Macro Daily(Beta Mode)

UAE Stocks Surge as Oil Slides on Hormuz Worries

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.18 | +0.44% |

| MSCI Saudi | 39.38 | +0.23% |

| MSCI UAE | 19.62 | +3.81% |

| DFM General | 5,954.04 | +3.84% |

| MSCI Qatar | 18.60 | +0.35% |

| MSCI Kuwait | 38.23 | +0.30% |

| Brent Crude | 87.33 | -3.37% |

| WTI Crude | 84.88 | -3.23% |

| Gold | 4,215.00 | +3.05% |

| USD/SAR | 3.75 | +1.70% |

| USD/AED | 3.67 | +0.04% |

| USD/KWD | 0.31 | -0.55% |

| Bitcoin | 64,467.43 | +1.45% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

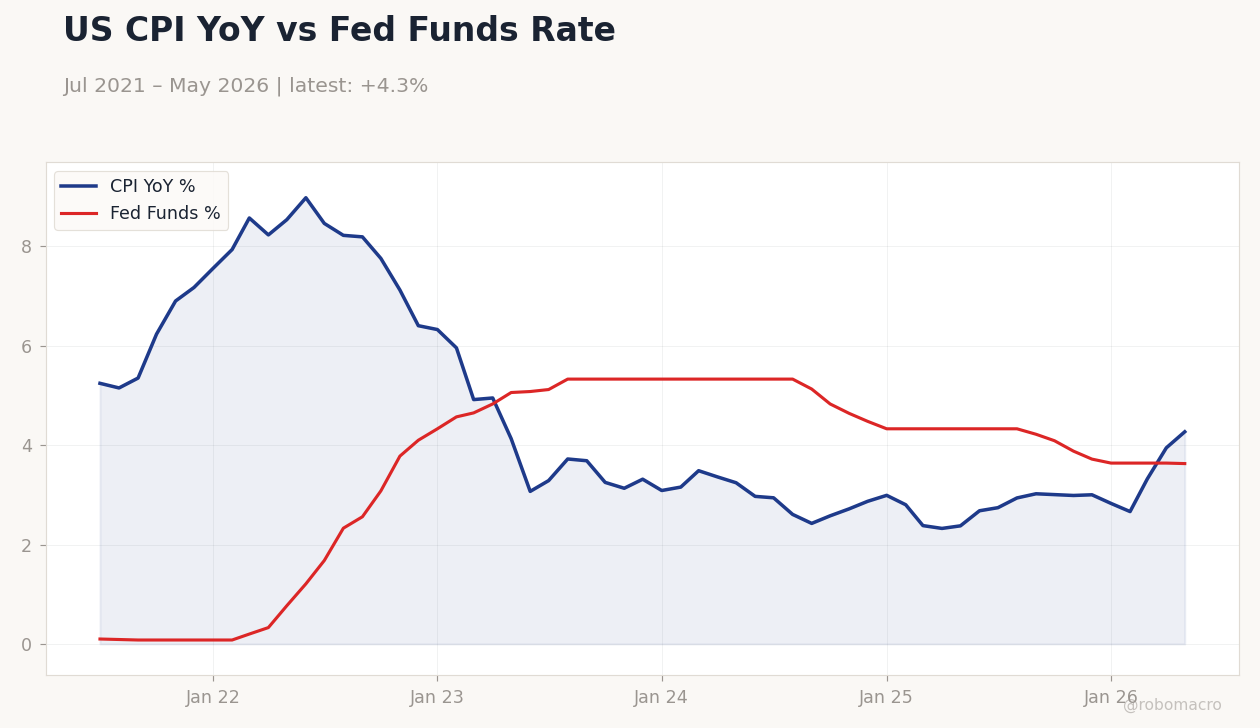

US CPI YoY vs Fed Funds Rate | Type: macro_line | CPI YoY %: 4.27 (2026-05-01) | Range: 2.325–8.979 | Trend(6pt): 5.245,8.192,3.133,2.991,3.947,4.27 | Fed Funds %: 3.63 (2026-05-01) | Range: 0.08–5.33 | Trend(6pt): 0.1,2.56,5.33,4.33,3.64,3.63

US CPI YoY vs Fed Funds Rate | Type: macro_line | CPI YoY %: 4.27 (2026-05-01) | Range: 2.325–8.979 | Trend(6pt): 5.245,8.192,3.133,2.991,3.947,4.27 | Fed Funds %: 3.63 (2026-05-01) | Range: 0.08–5.33 | Trend(6pt): 0.1,2.56,5.33,4.33,3.64,3.63

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI UAE jumped 3.81% while DFM General rose 3.84%, outpacing modest gains in Saudi and Qatar indices.

- Brent crude fell 3.37% to 87.33 amid mixed reports on Strait of Hormuz access following US-Iran developments.

- World Bank projects Saudi GDP growth of 3.1% for 2026, supported by mining cooperation deal with Kazakhstan.

Yesterday's Recap

UAE equity markets posted the strongest regional gains, with MSCI UAE climbing 3.81% and the DFM General index advancing 3.84% on broad buying in real estate and banking names. Saudi Arabia’s measures edged higher, with Aramco rising 0.44% to 27.18 and MSCI Saudi adding 0.23%. Qatar’s MSCI index gained 0.35% while Kuwait’s MSCI index rose 0.30%.

Oil prices declined sharply, Brent dropping 3.37% and WTI falling 3.23%, reflecting news flow around potential Hormuz disruptions and subsequent reopening signals. Gold advanced 3.05% to 4,215 as investors sought safe-haven assets. Saudi Arabia announced a legal framework for self-driving vehicles and agreed with Kazakhstan to expand mining cooperation.

The World Bank forecast 3.1% Saudi growth for 2026, underscoring non-oil diversification momentum.

The Day Ahead

Regional markets face a data-light session with no major GCC releases scheduled. Attention will remain on any further clarification regarding Strait of Hormuz transit after mixed US-Iran statements. OPEC+ JMMC preparations ahead of the July meeting may generate commentary on quota compliance.

UAE rail-related traffic adjustments in Dubai are unlikely to affect broader economic flows. Qatar real-estate transaction data for the latest week showed continued activity at 115.8 million dollars. Investors will monitor interbank rates for any early signs of liquidity response to oil-price volatility.

Other Economic Notes

Saudi Arabia’s non-oil growth continues to benefit from mining and industrial diversification initiatives under Vision 2030. UAE authorities are advancing energy-transition projects, including blue-hydrogen investments at Ruwais. Regional equity turnover remained elevated on the Tadawul while lighter on the DFM, indicating selective foreign interest.

Sovereign CDS spreads stayed contained, with Saudi at 52 bp and UAE at 38 bp, reflecting stable fiscal buffers despite oil swings. Broader GCC economies maintain focus on LNG capacity expansion and downstream integration.