GCC Macro Daily(Beta Mode)

UAE Stocks Surge as Oil Prices Plunge

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 27.18 | +0.44% |

| MSCI Saudi | 39.38 | +0.23% |

| MSCI UAE | 19.62 | +3.81% |

| DFM General | 5,733.88 | -0.42% |

| MSCI Qatar | 18.60 | +0.35% |

| MSCI Kuwait | 38.23 | +0.30% |

| Brent Crude | 83.03 | -4.92% |

| WTI Crude | 80.68 | -4.95% |

| Gold | 4,333.00 | +2.80% |

| USD/SAR | 3.75 | -0.00% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.03% |

| Bitcoin | 65,698.02 | -0.02% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

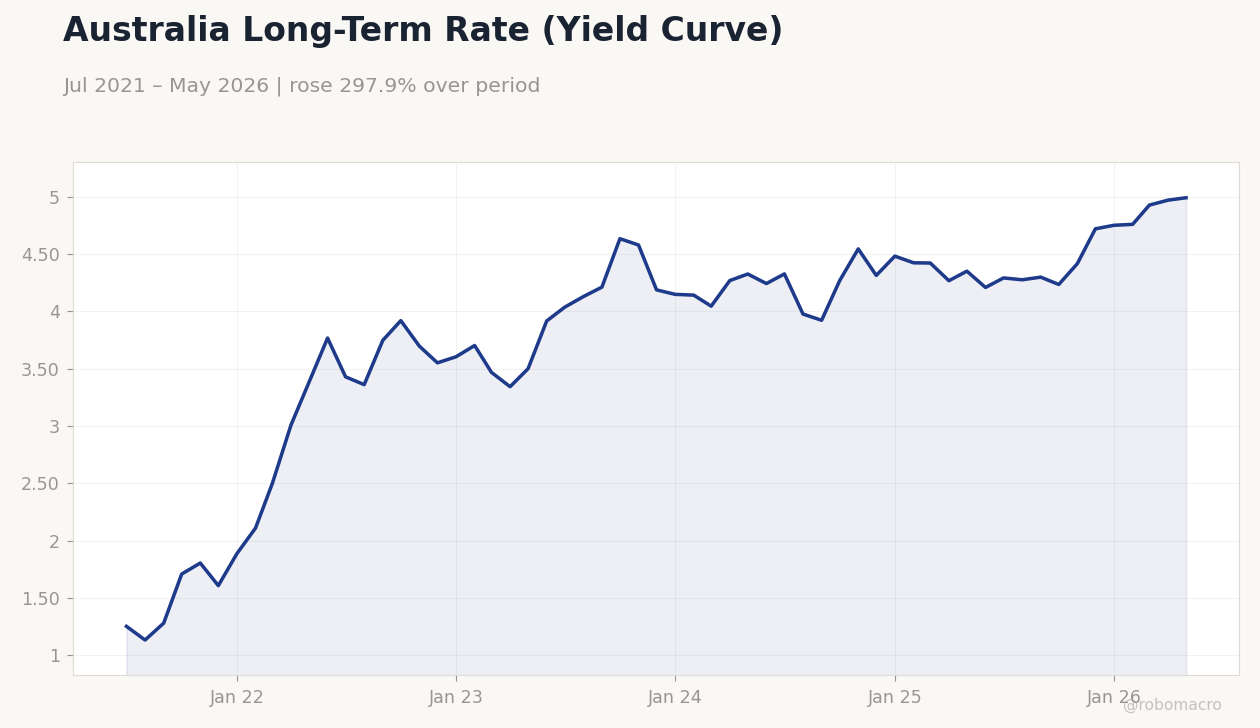

Australia Long-Term Rate (Yield Curve) | Type: macro_line | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Australia Long-Term Rate (Yield Curve) | Type: macro_line | 10Y Yield %: 4.99 (2026-05-01) | Range: 1.135–4.99 | Trend(6pt): 1.254,3.747,4.578,4.481,4.926,4.99

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- MSCI UAE jumps 3.81% while Brent crude drops 4.92% to $83.03/bbl

- Saudi Arabia signs oil and gas MoU with South Korea and mining pact with Kazakhstan

- Saudi construction sector returns to growth in May; Qatar real estate trading hits $115.8 million weekly

Yesterday's Recap

Regional equity markets showed divergence on June 14. MSCI UAE rose sharply while DFM General eased 0.42%. Saudi Aramco gained 0.44% to 27.18 and MSCI Saudi added 0.23%.

MSCI Qatar and MSCI Kuwait posted modest gains of 0.35% and 0.30%. Brent and WTI crude each fell nearly 5% on softer global demand signals. Gold advanced 2.80% to $4,333/oz as a safe-haven bid emerged.

Saudi Arabia advanced bilateral energy cooperation with South Korea and mining ties with Kazakhstan, while construction activity in the kingdom re-entered expansion territory. Qatar real estate transaction values climbed to $115.8 million in the latest week. No major economic data releases occurred across the GCC.

The Day Ahead

The GCC calendar remains light with no major data releases scheduled for June 16. Focus will stay on follow-through from recent Saudi-Korean energy agreements and UAE infrastructure projects. Regional equity turnover is expected to remain elevated after yesterday’s volume spike in Tadawul.

Oil price direction will continue to dictate sentiment across fiscal and equity channels in all six economies. UAE traffic works on Emirates Road and Etihad Rail projects may affect local logistics flows.

Other Economic Notes

Saudi Arabia’s non-oil diversification efforts gained further momentum through international mining and energy partnerships. UAE continues to advance logistics and tourism links, including planned direct flights from Moldova. Qatar maintains steady real estate market activity amid broader regional capital inflows.

All six GCC economies remain highly sensitive to Brent price swings given heavy hydrocarbon revenue dependence. Saudi Arabia introduced a legal framework for self-driving vehicles and suspended 21 Umrah service firms for violations.

Global Macro News

Sharp declines in Brent and WTI reflect softer near-term demand expectations outside the OECD. Gold’s 2.8% rally signals persistent safe-haven demand amid geopolitical uncertainty. USD/SAR and USD/AED pegs held unchanged at 3.75 and 3.67, underscoring continued monetary alignment with the Federal Reserve.

<i>↓ p.2</i>