GCC Macro Daily(Beta Mode)

UAE Equities Rally as Oil Slides Sharply

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 26.52 | -0.30% |

| MSCI Saudi | 38.56 | +0.38% |

| MSCI UAE | 20.30 | +3.49% |

| DFM General | 6,269.51 | +2.51% |

| MSCI Qatar | 18.54 | +0.22% |

| MSCI Kuwait | 37.41 | +0.00% |

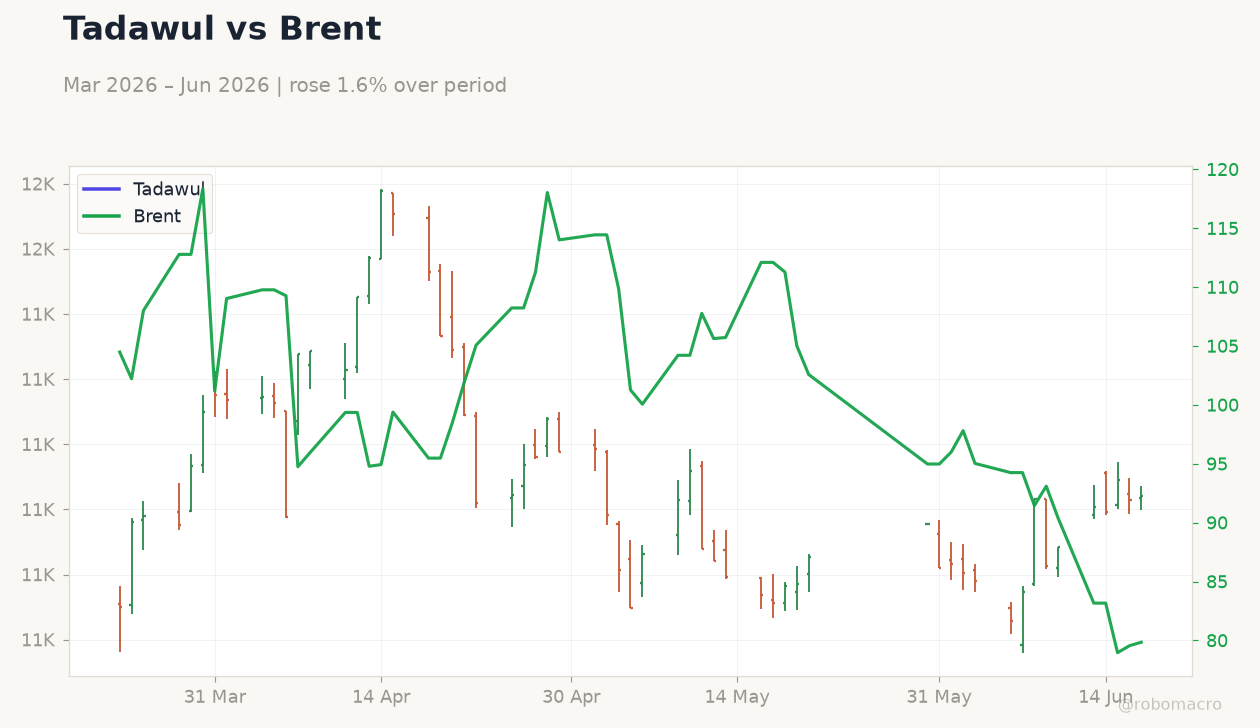

| Brent Crude | 76.31 | -2.04% |

| WTI Crude | 72.44 | -3.18% |

| Gold | 4,075.20 | -2.55% |

| USD/SAR | 3.75 | +3.15% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.18% |

| Bitcoin | 62,457.39 | -2.34% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude 3M | Type: market_hloc | USD/bbl: 76.31 (2026-06-23) | Range: 76.31–118.3 | Trend(5pt): 99.94,94.93,100.1,94.98,76.31

Brent Crude 3M | Type: market_hloc | USD/bbl: 76.31 (2026-06-23) | Range: 76.31–118.3 | Trend(5pt): 99.94,94.93,100.1,94.98,76.31

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- UAE indices surge with MSCI UAE up 3.49% and DFM General gaining 2.51% on strong local sentiment.

- Brent crude falls 2.04% to $76.31/bbl while WTI drops 3.18%, pressuring fiscal outlooks across the GCC.

- Qatar confirms no LNG export disruption after Ras Laffan blast; Fitch sees Saudi assets under management exceeding $400 billion by 2027.

Yesterday's Recap

Regional equity markets posted divergent closes on 22 June with UAE assets outperforming. The DFM General Index climbed 2.51% to 6,269.51 while MSCI UAE jumped 3.49% to 20.30, led by real estate and banking names. Saudi Arabia’s MSCI index edged 0.38% higher to 38.56 even as Aramco slipped 0.30% to 26.52.

Kuwait’s MSCI index was unchanged at 37.41. Qatar’s MSCI index rose 0.22% to 18.54. Qatar’s energy ministry stated that the Ras Laffan gas plant explosion would leave LNG export capacity unaffected.

Oil price weakness weighed on sentiment despite stable FX pegs, with USD/SAR holding at 3.75 and USD/AED at 3.67. Gold fell 2.55% to 4,075.20/oz and Bitcoin declined 2.34% to 62,457.39. No economic data releases occurred across GCC markets.

The Day Ahead

No major data releases are scheduled across the six GCC economies on 23 June. Markets will monitor global crude price action and any OPEC+ compliance signals ahead of the July ministerial meeting. Regional investors are expected to track follow-through in UAE equities after yesterday’s strong gains.

Geopolitical headlines from the Strait of Hormuz and Red Sea remain the dominant risk variable for energy prices. Central banks will continue to align policy rates with the Federal Reserve path given prevailing currency pegs.

Other Economic Notes

Fitch projects Saudi assets under management will exceed $400 billion by 2027, underscoring Vision 2030 progress. Saudi Arabia’s economy posted a V-shaped recovery after earlier shocks according to Gulf International Bank analysis. UAE authorities advanced anti-money laundering cooperation through a new partnership between the Ministry of Economy and Emirates Institute of Finance.

Broader non-oil diversification efforts continue to attract foreign direct investment across the UAE and Saudi Arabia. Saudi Arabia approved its first joint satellite project with Egypt. Turkish officials confirmed rail-link financing talks with Saudi Arabia remain under review.