GCC Macro Daily(Beta Mode)

Saudi Opens Property Portal as Oil Slides 6%

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Saudi Aramco | 26.34 | -0.15% |

| MSCI Saudi | 38.08 | -0.31% |

| MSCI UAE | 19.82 | +0.71% |

| DFM General | 6,269.51 | +2.51% |

| MSCI Qatar | 18.21 | -0.87% |

| MSCI Kuwait | 36.82 | -0.86% |

| Brent Crude | 72.32 | -6.18% |

| WTI Crude | 69.12 | -5.59% |

| Gold | 3,986.90 | -3.46% |

| USD/SAR | 3.75 | +3.10% |

| USD/AED | 3.67 | +0.03% |

| USD/KWD | 0.31 | -0.18% |

| Bitcoin | 60,723.19 | -3.10% |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

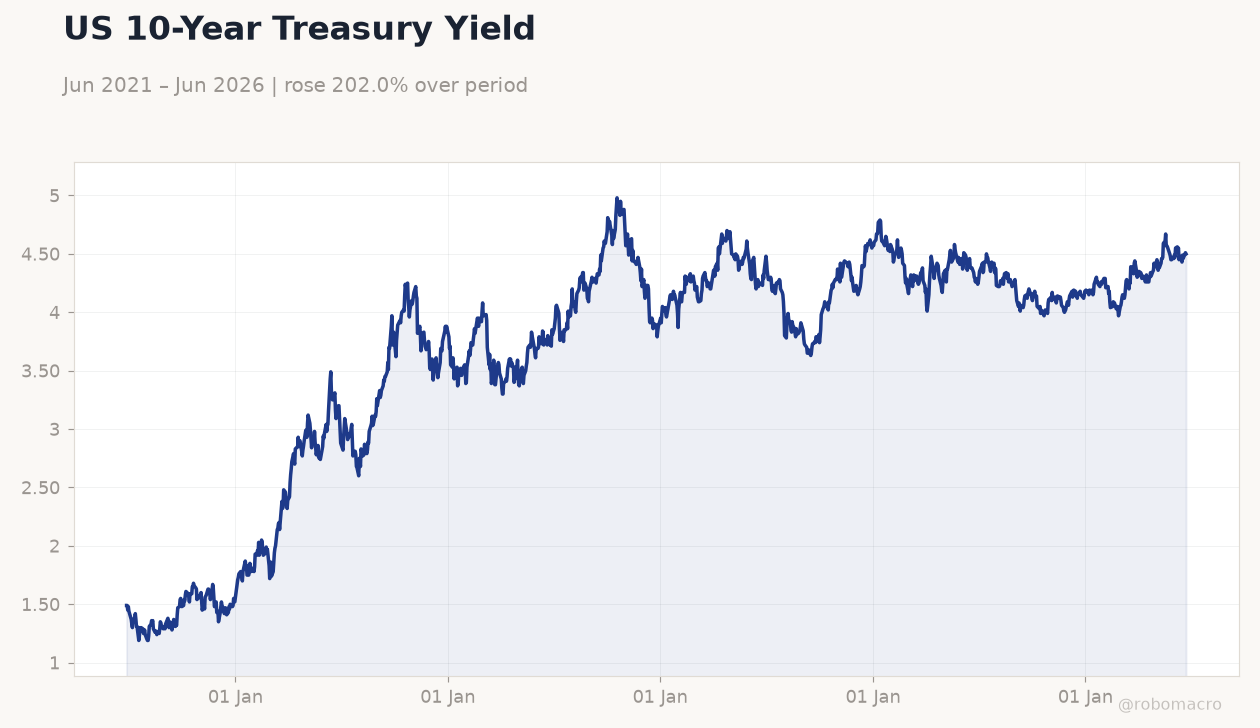

US 10-Year Treasury Yield | Type: macro_line | Percent: 4.5 (2026-06-23) | Range: 1.19–4.98 | Trend(6pt): 1.49,3.69,3.89,4.34,4.51,4.5

US 10-Year Treasury Yield | Type: macro_line | Percent: 4.5 (2026-06-23) | Range: 1.19–4.98 | Trend(6pt): 1.49,3.69,3.89,4.34,4.51,4.5

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Brent crude plunged 6.18% to $72.32/bbl on expectations of smoother Hormuz flows, pressuring GCC fiscal outlooks.

- Saudi Arabia opened its foreign real estate ownership portal and raised $2.81 billion via June sukuk across six tranches.

- UAE equities outperformed with DFM General surging 2.51%, while MSCI UAE rose 0.71% amid diplomatic activity.

Yesterday's Recap

Saudi equity benchmarks eased modestly, with Aramco falling 0.15% to 26.34 and MSCI Saudi declining 0.31%. UAE markets advanced as DFM General jumped 2.51% and MSCI UAE gained 0.71%. Qatar and Kuwait indices retreated 0.87% and 0.86% respectively.

Saudi authorities began accepting foreign real estate applications and priced $2.81 billion in sukuk, extending its funding program. Qatar reported progress toward restoring normal LNG output within weeks after the Ras Laffan incident, though 17% of capacity remains offline. UAE President hosted US Secretary of State Marco Rubio in Abu Dhabi.

Oil price weakness dominated sentiment across energy-linked assets despite stable FX pegs. Gold fell 3.46% to 3,986.90 while Bitcoin declined 3.10%. No economic data releases occurred in any GCC market.

The Day Ahead

No major data releases are scheduled across the six GCC economies. Saudi Vision 2030 diversification initiatives and UAE industrial promotion events continue without specific market-moving announcements. Regional diplomatic engagement remains active following recent high-level US visits to Abu Dhabi.

Market participants will monitor any follow-through on Qatar’s LNG restart timeline and Saudi sukuk allocation details. Broader focus stays on oil price stabilization and its direct fiscal implications for all GCC budgets. ACWA Power continues exploring desalination and green hydrogen projects in Morocco.

Other Economic Notes

Saudi non-oil momentum persists through Vision 2030 channels, including new foreign investment inflows into real estate and green hydrogen projects via ACWA Power. UAE continues advancing its industrial and sustainability agenda with targeted delegations and environmental initiatives such as planting 67 trees and recycling one tonne of e-waste. Regional equity divergence highlights UAE resilience versus softer performance in Saudi, Qatar and Kuwait.

Oil price volatility remains the dominant macro driver given its outsized weight in all six fiscal balances and external accounts. Qatar ranks among the global top five for economic resilience.