Yesterday's Recap

Mainland China's People's Bank of China (PBoC) maintained its benchmark Loan Prime Rate (LPR) for 1-year loans at 3% and 5-year loans at 3.5%, aligning with consensus expectations and reflecting Beijing's strategy to balance growth support without aggressive easing. This decision came amid reports of a slowing economy, with recent China CPI YoY at -0.10% indicating persistent deflationary pressures. Equity markets in mainland China closed mixed, as the Shanghai Composite advanced 0.39% to 4,162.88 driven by rebounds in property and consumer stocks, while the CSI 300 slipped 0.34% to 4,710.65 pressured by tech sector volatility.

In Hong Kong, the Hang Seng Index climbed 0.95% to 26,630.54, buoyed by financials despite concerns over global volatility from Middle East conflicts affecting airmail services and trade costs. Taiwan's TAIEX remained flat at 35,414.49 with no daily change, as semiconductor firms held steady amid cross-strait tensions highlighted in the Taiwan Affairs Work Conference. Currency movements saw USD/CNY rise 0.24% to 6.86, indicating slight yuan weakening, while USD/HKD edged down 0.01% to 7.82 within the peg band.

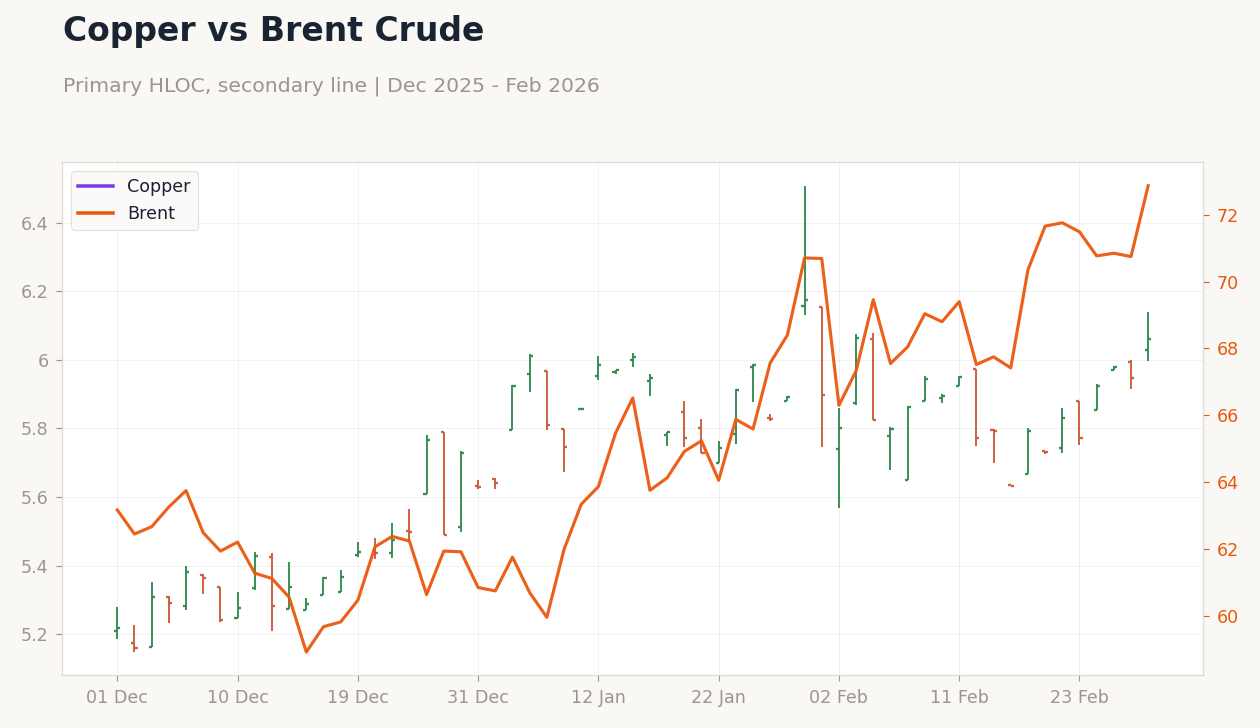

Commodity proxies for China growth, such as copper, surged 1.89% to 6.06, supported by manufacturing optimism, and Brent crude rose 3% to 72.87 amid Iran-related supply risks. Gold climbed 1.38% to 5,247.90 as a safe-haven asset, while Bitcoin fell 2.59% to 65,257.73.

The Day Ahead

With no major data releases scheduled for today in Greater China, markets will focus on ongoing reactions to yesterday's PBoC LPR hold and global oil price spikes from Iran tensions. Attention turns to potential State Council signals on fiscal stimulus for mainland China's property sector, which could influence equity sentiment. In Hong Kong, traders will monitor USD/HKD peg dynamics amid elevated global volatility, as flagged by Finance Secretary Paul Chan.

Taiwan may see flows tied to semiconductor export outlooks, with any updates from the Taiwan Affairs Work Conference potentially impacting cross-strait investment. Broader events include monitoring Lunar New Year travel estimates of 9.5 billion trips, which could provide insights into mainland consumer spending trends. Tomorrow remains light on releases, setting the stage for early next week's focus on trade data.