Greater China Macro Daily(Beta Mode)

China Trade Beats, Stocks Slip

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,119.26 | -0.34% |

| CSI 300 | 4,672.12 | -0.69% |

| Hang Seng | 25,716.76 | -0.70% |

| TAIEX | 33,581.86 | -1.56% |

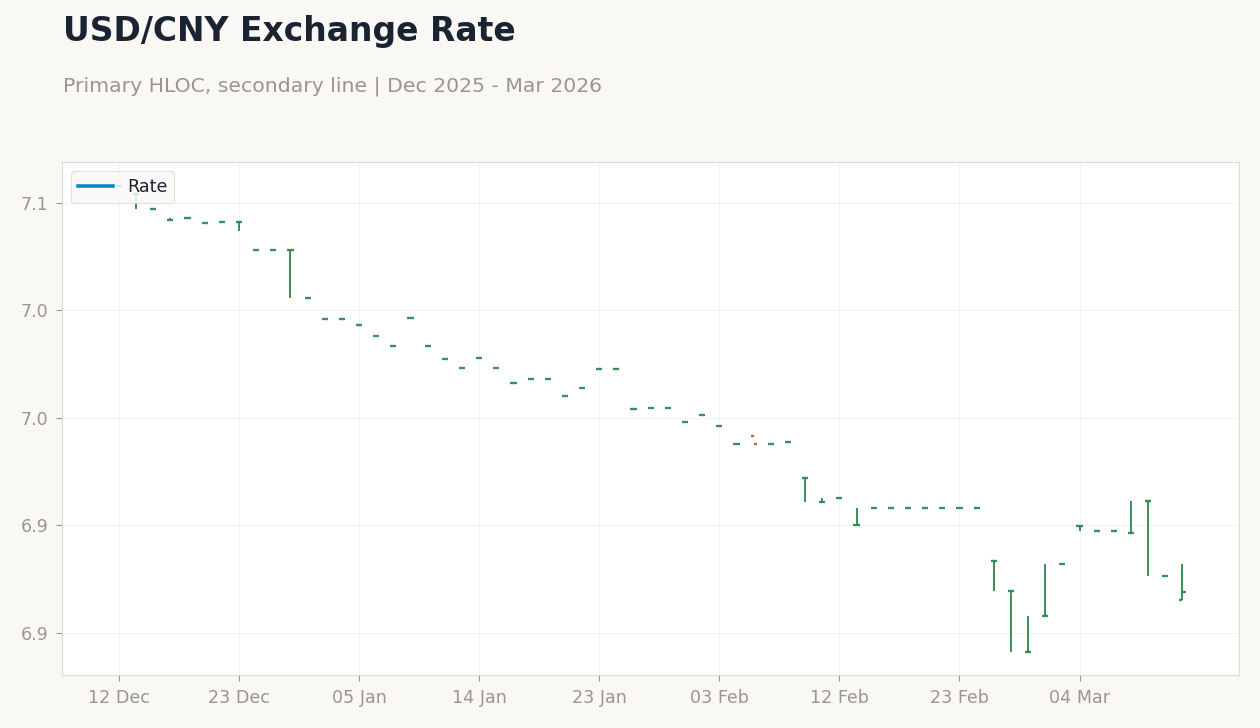

| USD/CNY | 6.87 | -0.11% |

| USD/HKD | 7.83 | +0.02% |

| Copper | 5.82 | -0.42% |

| Brent Crude | 97.28 | +5.76% |

| Gold | 5,084.10 | -1.61% |

| Bitcoin | 70,334.91 | +0.19% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Exports Year-over-Year | 6.60 | 7.10 | 21.80 |

| Imports Year-over-Year | 5.70 | 6.30 | 19.80 |

| Trade Balance | 114,110m | 179,600m | 213,620m |

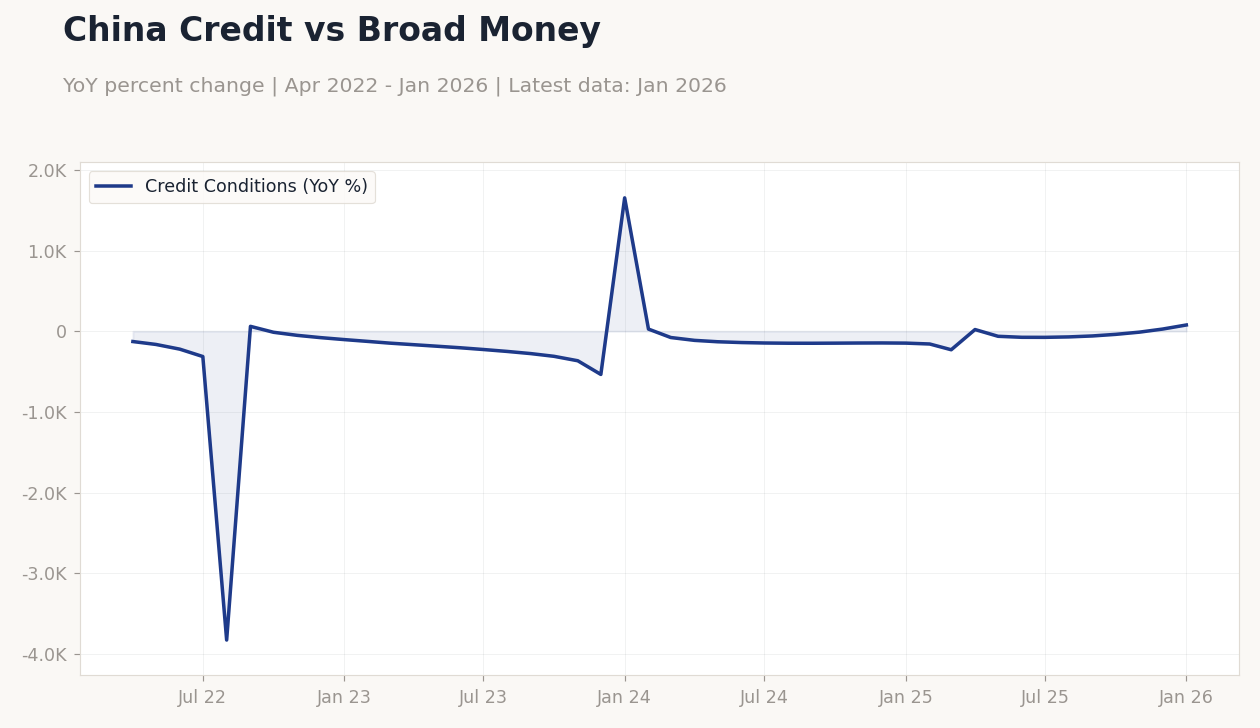

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.642 (2026-01-01) | Range: -3.671–13.22 | Trend(6pt): 13.22,-3.432,4.15,-1.829,-1.558,-1.642

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.642 (2026-01-01) | Range: -3.671–13.22 | Trend(6pt): 13.22,-3.432,4.15,-1.829,-1.558,-1.642

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| New Yuan Loans | 4,710,000m | 979,000m | 01:00 |

- China's February exports surged 21.8% YoY vs. 7.1% consensus, imports rose 19.8% YoY vs. 6.3%, yielding a CNY 213.62B surplus amid strong global demand.

- Equities dipped across Greater China: Shanghai Composite -0.34%, CSI 300 -0.69%, Hang Seng -0.70%, TAIEX -1.56% on tech and oil pressures.

- PBoC held lending rates steady, signaling yuan tolerance; HKMA advances blockchain for cross-border trade with Shanghai.

Yesterday's Recap

China's February trade data, released after hours on March 9, exceeded expectations, with exports jumping 21.8% YoY against a 7.1% consensus and imports increasing 19.8% YoY versus 6.3% expected, producing a trade surplus of CNY 213.62 billion that topped the CNY 179.6 billion forecast. This robust showing highlighted resilient external demand despite global challenges, supporting commodity sentiment as copper eased 0.42% to $5.82. Greater China equities closed lower, with the Shanghai Composite down 0.34% at 4,119.26 and CSI 300 off 0.69% at 4,672.12, driven by tech and real estate profit-taking.

Hong Kong's Hang Seng fell 0.70% to 25,716.76, pressured by financials and developers amid rising oil prices, with Brent crude up 5.76% to $97.28. Taiwan's TAIEX dropped 1.56% to 33,581.86, led by semiconductor declines on U.S.-China trade tensions and supply chain concerns. Currencies were stable, with USD/CNY down 0.11% to 6.87 on a firmer PBoC fix, and USD/HKD up 0.02% to 7.83 within the peg.

Gold declined 1.61% to $5,084.10 as safe-haven flows eased, while Bitcoin rose 0.19% to $70,334.91.

The Day Ahead

Focus shifts to China's new yuan loans release on March 14 at 01:00 ET, with consensus at CNY 979 billion after January's CNY 4.71 trillion, offering clues on credit expansion and stimulus impact. No key events for Hong Kong or Taiwan, but geopolitical risks may heighten TAIEX volatility tied to semiconductors. Watch PBoC for liquidity moves to maintain yuan stability post-trade strength.

Global oil gains could pressure Greater China's import costs, while U.S. tariff probes may indirectly affect cross-strait trade and Taiwan's tech mood.

Other Economic Notes

Mainland China's property market faces ongoing challenges, but strong trade suggests export growth may counter domestic softness, though deflation persists with CPI YoY at -0.10% as of April 2025. Hong Kong's 2026 Budget prioritizes AI, robotics, biotech, tourism revival, and talent attraction, amid rising cross-border fuel trips due to oil surges and blockchain efforts to streamline trade with Shanghai. Taiwan's semiconductor sector grapples with U.S.-China frictions, as the foreign minister stresses non-escalation against Beijing's pressures, underscoring risks to global chip supplies where Taiwan holds 90% of advanced production.

(cont...)