Greater China Macro Daily(Beta Mode)

China Rebounds Amid Iran War Risks

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,095.45 | -0.82% |

| CSI 300 | 4,669.14 | -0.39% |

| Hang Seng | 25,834.02 | +1.45% |

| TAIEX | 33,342.51 | -0.17% |

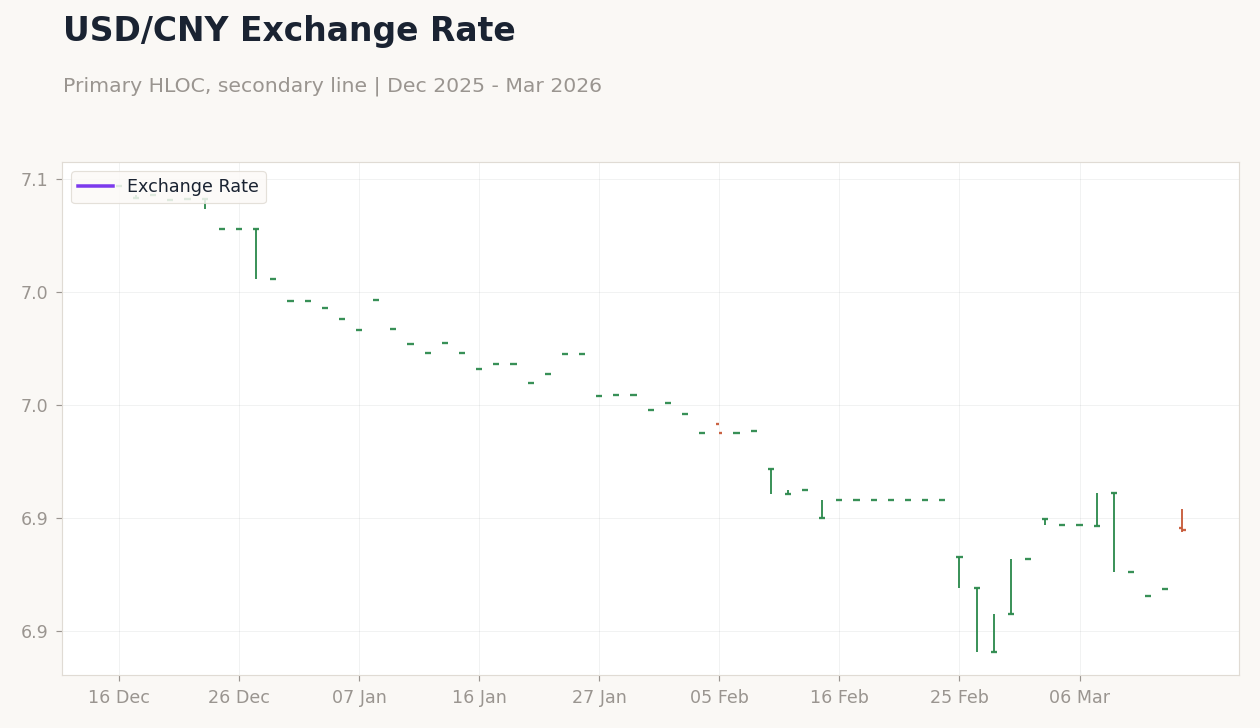

| USD/CNY | 6.89 | +0.38% |

| USD/HKD | 7.83 | +0.03% |

| Copper | 5.84 | +2.15% |

| Brent Crude | 100.84 | -2.23% |

| Gold | 5,011.30 | -0.82% |

| Bitcoin | 74,405.72 | +2.22% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.867 (2026-02-01) | Range: -3.697–13.54 | Trend(6pt): 13.54,-3.197,4.122,-1.758,-1.661,-1.867

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.867 (2026-02-01) | Range: -3.697–13.54 | Trend(6pt): 13.54,-3.197,4.122,-1.758,-1.661,-1.867

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 17:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 17:15 |

- China's economy showed unexpected strength in early 2026 indicators, defying global disruptions from the Iran war and Strait of Hormuz tensions.

- Mainland equities dipped slightly while Hong Kong's Hang Seng surged, reflecting mixed sentiment on property and trade outlooks.

- PBOC's yuan fixing at 6.9057 signals steady policy amid rising oil prices and U.S. trade talk delays.

Yesterday's Recap

Mainland China's Shanghai Composite closed at 4,095.45, down 0.82%, while the CSI 300 ended at 4,669.14 with a 0.39% decline, pressured by weak consumer spending data highlighting the worst non-Covid start to a year. Hong Kong's Hang Seng bucked the trend, rising 1.45% to 25,834.02, boosted by gains in energy and shipping stocks amid Iran's yuan-priced oil tanker proposals and local brokerage raids. Taiwan's TAIEX slipped 0.17% to 33,342.51, weighed by semiconductor profit-taking.

Currency markets saw USD/CNY climb 0.38% to 6.89, aligning with PBOC's strategic fixing to support exports, while USD/HKD edged up 0.03% to 7.83 within the peg band. Copper jumped 2.15% to 5.84, fueled by rebound hopes, contrasting Brent crude's 2.23% drop to 100.84 on Hormuz uncertainties. Gold fell 0.82% to 5,011.30, and Bitcoin rose 2.22% to 74,405.72.

No major data releases occurred yesterday across Greater China, but broader sentiment was shaped by China's power supergrid buffering energy shocks and Hong Kong's green shipping pivot. Taiwan's export outlook remained tied to chip demand, with cross-strait flows stable despite geopolitical noise.

The Day Ahead

Attention turns to mainland China's Loan Prime Rate announcements on March 19, with the 1Y rate expected to hold at 3% and the 5Y at 3.5%, potentially signaling PBOC's stance on property support amid deflationary pressures. No immediate events are slated for Hong Kong or Taiwan, but markets will monitor any spillover from global central bank decisions this week. Investors eye possible State Council signals on consumption stimulus following reports of weak spending.

Geopolitical developments, including U.S.-China trade talks and Iran war updates, could influence sentiment across Greater China equities and currencies. Broader focus includes Hong Kong's Middle East pivot risks and Taiwan's semiconductor linkages to inflation bets.

Other Economic Notes

China's consumer spending faces headwinds, with early 2026 data indicating the weakest non-pandemic start, underscoring challenges to Beijing's growth targets despite a broader economic rebound. Property sector dynamics in mainland China show tentative optimism, with bond yields on 30-year notes rising amid oil-fueled inflation fears. (cont...)