Greater China Macro Daily(Beta Mode)

Equities Slide as Yuan Dips

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 4,011.25 | -1.27% |

| CSI 300 | 4,594.48 | -1.37% |

| Hang Seng | 25,500.58 | -2.02% |

| TAIEX | 33,689.68 | -1.92% |

| USD/CNY | 6.90 | +0.19% |

| USD/HKD | 7.83 | -0.04% |

| Copper | 5.52 | -0.59% |

| Brent Crude | 103.02 | -4.06% |

| Gold | 4,651.90 | -4.87% |

| Bitcoin | 70,494.41 | -1.05% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

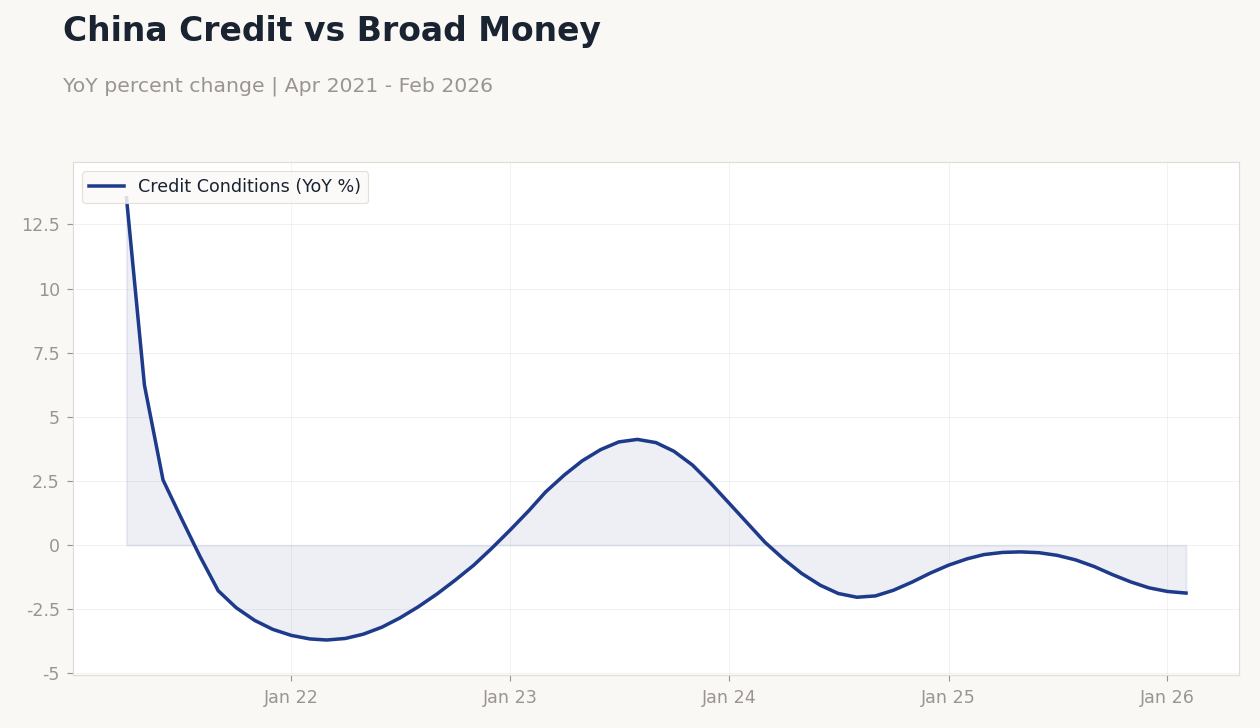

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.867 (2026-02-01) | Range: -3.697–13.54 | Trend(6pt): 13.54,-3.197,4.122,-1.758,-1.661,-1.867

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.867 (2026-02-01) | Range: -3.697–13.54 | Trend(6pt): 13.54,-3.197,4.122,-1.758,-1.661,-1.867

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 17:15 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 17:15 |

- Greater China equities fell amid global risk-off, with Shanghai Composite down 1.27%, CSI 300 off 1.37%, Hang Seng dropping 2.02%, and TAIEX declining 1.92%.

- USD/CNY rose 0.19% to 6.90, signaling mild yuan weakening, while USD/HKD eased 0.04% to 7.83 within the peg band.

- Commodities weakened, with copper down 0.59%, Brent crude falling 4.06%, and gold dropping 4.87%, reflecting China demand concerns.

Yesterday's Recap

Greater China equities broadly declined on March 18, with mainland China's Shanghai Composite closing down 1.27% at 4,011.25 and CSI 300 falling 1.37% to 4,594.48, pressured by ongoing property sector woes and weak global sentiment. Hong Kong's Hang Seng index dropped 2.02% to 25,500.58, reflecting investor caution amid Middle East tensions impacting trade flows. Taiwan's TAIEX slid 1.92% to 33,689.68, weighed down by semiconductor supply chain disruptions linked to export slowdowns in the region.

Currency markets showed USD/CNY climbing 0.19% to 6.90, indicating slight yuan depreciation despite news of strong exports bolstering the currency to a three-year high earlier. No major macro data releases occurred in Greater China yesterday, but commodity proxies like copper fell 0.59% amid concerns over mainland China's industrial demand. Cross-strait trade dynamics remained in focus, with reports of Japan’s exports slowing due to reduced China demand during holidays and US tariffs.

The Day Ahead

Attention turns to mainland China's Loan Prime Rate announcements at 17:15 ET, with the 1Y rate expected to hold at 3% and the 5Y at 3.5%, signaling potential PBoC stability amid deflationary pressures. Consensus anticipates no changes, but any surprise cut could boost property and consumption sectors. Hong Kong and Taiwan have no scheduled releases, though geopolitical developments may influence markets.

Investors will monitor any State Council signals on stimulus following recent yuan strength. Broader attention includes global oil price volatility, which could affect Greater China's import costs.

Other Economic Notes

Mainland China's middle class is increasingly engaging in 'shadow saving,' stockpiling cash amid economic uncertainty, potentially hindering consumption recovery and global growth. Reports indicate China is tapping vast oil stockpiles to offset Middle East supply disruptions, stabilizing domestic energy costs but straining global markets. Fertilizer export cuts from China are adding pressure to international agriculture, exacerbating food price inflation worldwide.

Taiwan's semiconductor outlook remains tied to export resilience, despite regional trade headwinds. (cont...)