Greater China Macro Daily(Beta Mode)

PBoC Holds LPR, Stocks Mixed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,987.81 | -0.58% |

| CSI 300 | 4,598.85 | +0.10% |

| Hang Seng | 25,277.32 | -0.88% |

| TAIEX | 33,543.88 | -0.43% |

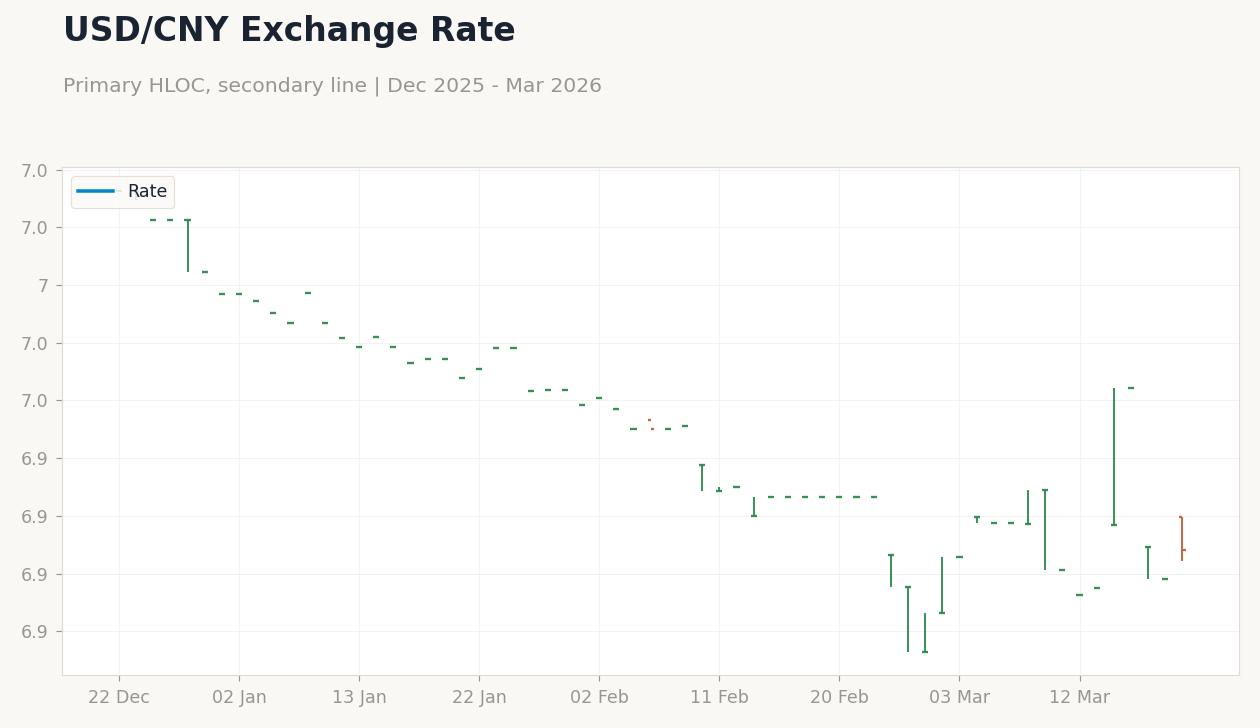

| USD/CNY | 6.89 | +0.18% |

| USD/HKD | 7.83 | -0.06% |

| Copper | 5.30 | -2.41% |

| Brent Crude | 106.77 | -1.73% |

| Gold | 4,492.00 | -2.36% |

| Bitcoin | 70,791.52 | +1.26% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| Loan Prime Rate 1Y | 3 | 3 | 3 |

| Loan Prime Rate 5Y | 3.50 | 3.50 | 3.50 |

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.867 (2026-02-01) | Range: -3.697–13.54 | Trend(6pt): 13.54,-3.197,4.122,-1.758,-1.661,-1.867

China Credit vs Broad Money | Type: macro_line | Credit Conditions: -1.867 (2026-02-01) | Range: -3.697–13.54 | Trend(6pt): 13.54,-3.197,4.122,-1.758,-1.661,-1.867

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- China's PBoC kept Loan Prime Rates unchanged at 3% (1Y) and 3.5% (5Y), signaling steady policy amid deflation risks.

- Mainland equities showed divergence with CSI 300 up 0.10% while Shanghai Composite fell 0.58%; Hang Seng and TAIEX declined amid global volatility.

- Yuan strengthened with USD/CNY at 6.89 on export strength, as oil shocks curb deflation but pressure EV demand.

Yesterday's Recap

China's central bank, the PBoC, held the 1-year Loan Prime Rate at 3% and the 5-year at 3.5%, aligning with consensus and previous levels, reflecting caution amid ongoing deflation with CPI YoY at -0.10% as of 2025-04-01. Mainland China's Shanghai Composite closed at 3,987.81, down 0.58%, pressured by commodity weakness, while the CSI 300 rose to 4,598.85, up 0.10%, buoyed by financial sector gains. Hong Kong's Hang Seng fell to 25,277.32, down 0.88%, hit by property and tech selloffs linked to rising global yields and liquidity strains via the USD/HKD peg at 7.83.

Taiwan's TAIEX dipped to 33,543.88, down 0.43%, weighed by semiconductor supply chain concerns amid U.S.-China tensions, though export outlooks provided some support. USD/CNY closed at 6.89, with the yuan strengthening on strong exports despite fertilizer export curbs straining global markets. Copper prices dropped 2.41% to 5.30, reflecting demand slowdowns in EVs and property.

Overall, Greater China markets navigated mixed signals from stable rates and external commodity pressures, with mainland China dominating the narrative.

The Day Ahead

With no major data releases scheduled for today in Greater China, markets will likely focus on global cues, including oil price fluctuations from the Iran war and their impact on mainland China's import costs. Attention may shift to any unscheduled PBoC liquidity operations, given recent yuan strength and export dynamics. In Hong Kong, traders will monitor USD/HKD peg movements around 7.83 for potential HKMA interventions amid stable aggregate balances.

Taiwan could see sentiment influenced by semiconductor export updates, though no formal events are on tap. Tomorrow's calendar is also empty, setting up a quiet end to the week unless geopolitical developments escalate. Investors should watch for any State Council signals on property support in mainland China to gauge stimulus prospects.

Other Economic Notes

Surging global oil prices from the Iran war are accelerating China's exit from deflation, with Brent crude at 106.77 down 1.73% but still elevated, potentially boosting import inflation while challenging energy-dependent sectors. EV demand slowdowns, as seen in Xpeng's weak revenue forecast, highlight broader consumption softness in mainland China amid property woes and export curbs on fertilizers. (cont...)