Greater China Macro Daily(Beta Mode)

Stocks Rally as Oil Slumps

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,929.82 | +1.25% |

| CSI 300 | 4,523.57 | +1.09% |

| Hang Seng | 25,335.95 | +1.09% |

| TAIEX | 33,439.11 | +2.54% |

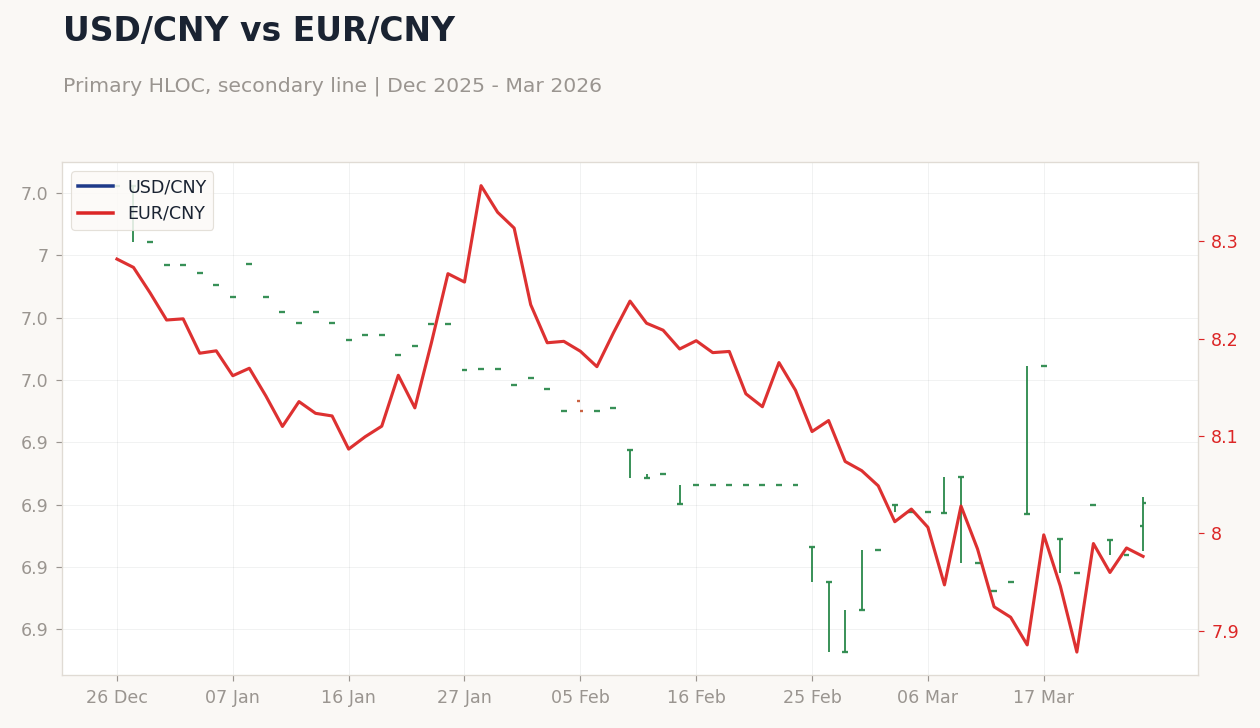

| USD/CNY | 6.90 | +0.30% |

| USD/HKD | 7.82 | -0.13% |

| Copper | 5.52 | +1.80% |

| Brent Crude | 98.05 | -6.16% |

| Gold | 4,503.30 | +2.36% |

| Bitcoin | 71,005.37 | +0.69% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

USD/CNY vs EUR/CNY | Type: market_hloc | USD/CNY: 6.901 (2026-03-25) | Range: 6.841–7.028 | Trend(6pt): 7.028,6.968,6.939,6.858,6.886,6.901 | EUR/CNY: 7.976 (2026-03-25) | Range: 7.878–8.357 | Trend(6pt): 8.282,8.099,8.206,8.064,7.96,7.976

USD/CNY vs EUR/CNY | Type: market_hloc | USD/CNY: 6.901 (2026-03-25) | Range: 6.841–7.028 | Trend(6pt): 7.028,6.968,6.939,6.858,6.886,6.901 | EUR/CNY: 7.976 (2026-03-25) | Range: 7.878–8.357 | Trend(6pt): 8.282,8.099,8.206,8.064,7.96,7.976

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Greater China equities advanced, with Taiwan's TAIEX leading gains on semiconductor strength amid global AI demand.

- Oil prices fell sharply, boosting sentiment despite Iran war disruptions, while gold surged as a safe haven.

- Trade resilience highlighted in news, with China's exports offsetting war shocks via AI investments.

Yesterday's Recap

Greater China equities posted solid gains amid optimism over AI-driven trade resilience offsetting global war tensions. Mainland China's Shanghai Composite closed at 3,929.82, up 1.25%, driven by financials and commodities-linked stocks as copper prices rose 1.80% to 5.52. The CSI 300 advanced 1.09% to 4,523.57, reflecting broad-based buying despite no major data releases.

Hong Kong's Hang Seng rose 1.09% to 25,335.95, supported by tech and property sectors amid steady USD/HKD at 7.82, down 0.13%. Taiwan's TAIEX surged 2.54% to 33,439.11, fueled by semiconductor exports outlook, with global AI demand shielding the economy from external shocks. USD/CNY rose 0.30% to 6.90, indicating PBoC tolerance for mild yuan depreciation amid trade surplus expectations.

Overall, markets shrugged off Brent crude's 6.16% drop to 98.05, viewing it as easing inflationary pressures in the region.

The Day Ahead

With no scheduled data releases for Greater China, markets will focus on any ad-hoc announcements from Beijing on trade policies amid Mexico's tariff hikes. Attention turns to potential PBoC liquidity injections to stabilize yuan dynamics following recent movements. In Taiwan, semiconductor firms may react to global chip demand signals, especially with trade tensions highlighted in news.

Hong Kong could see volatility tied to HKMA interventions if USD/HKD tests peg boundaries. Broader sentiment may hinge on evolving Iran war developments affecting energy imports. Investors anticipate quiet trading unless geopolitical headlines escalate.

Other Economic Notes

China's trade volumes remain robust, driven by AI investments that offset disruptions from the Iran war, as per recent reports. Property sector dynamics in mainland China continue to weigh on growth, with no fresh stimulus signals alleviating developer pressures. Hong Kong's security measures, including police demands for smartphone passwords in security cases, may deter foreign investment flows.

Philippine openness to energy talks with China in disputed seas may ease regional tensions, benefiting cross-border trade.