Greater China Macro Daily(Beta Mode)

Equities Slide on Iran War Jitters

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,897.41 | -0.88% |

| CSI 300 | 4,491.11 | -1.02% |

| Hang Seng | 24,856.43 | -1.89% |

| TAIEX | 33,337.62 | -0.30% |

| USD/CNY | 6.91 | +0.27% |

| USD/HKD | 7.82 | +0.07% |

| Copper | 5.47 | -1.06% |

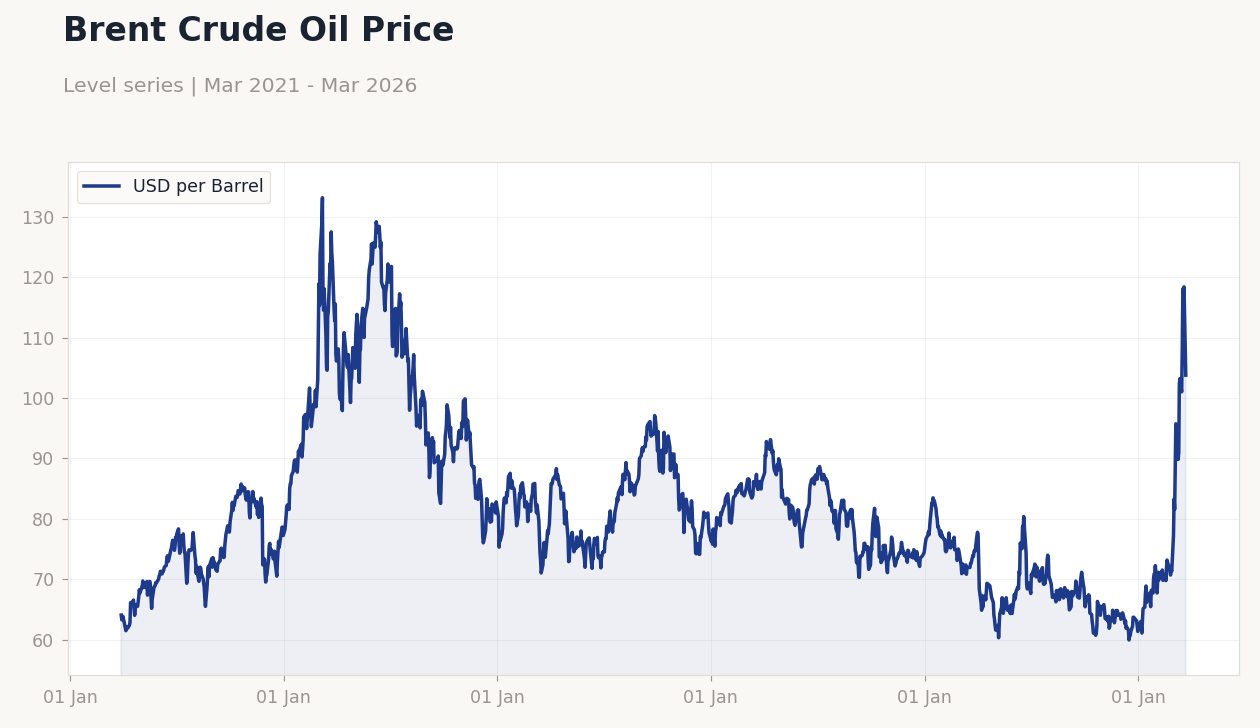

| Brent Crude | 101.26 | -0.94% |

| Gold | 4,376.90 | -3.80% |

| Bitcoin | 68,879.55 | -3.41% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| No events available | |||

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(5pt): 64.06,122.2,97.1,72.12,103.8

Brent Crude Oil Price | Type: macro_line | USD per Barrel: 103.8 (2026-03-23) | Range: 59.93–133.2 | Trend(5pt): 64.06,122.2,97.1,72.12,103.8

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| No events available | |||

- Greater China stocks fell amid escalating Iran conflict, with Hang Seng leading losses at -1.89% on global risk-off sentiment.

- USD/CNY rose 0.27% to 6.91, reflecting yuan pressure from commodity dips and petroyuan speculation.

- Commodities weakened, copper down -1.06% as Iran war disrupts supply chains, impacting China's growth proxies.

Yesterday's Recap

Greater China equities declined broadly on March 25, driven by heightened geopolitical tensions from the Iran war, with mainland China's Shanghai Composite dropping 0.88% to 3,897.41 and the CSI 300 falling 1.02% to 4,491.11 amid concerns over disrupted oil supplies and factory output. Hong Kong's Hang Seng index suffered the steepest loss at 1.89% to 24,856.43, weighed down by property and tech sectors as investors fled risk assets amid Middle East instability. Taiwan's TAIEX edged down 0.30% to 33,337.62, holding up relatively better due to resilient semiconductor demand despite global trade worries.

Currency moves saw USD/CNY appreciating 0.27% to 6.91, signaling mild yuan depreciation pressure from falling commodity prices, while USD/HKD ticked up 0.07% to 7.82 within the peg band. Key China-linked commodities retreated, with copper sliding 1.06% to 5.47 and Brent crude dipping 0.94% to 101.26, exacerbating deflationary risks in mainland China where latest CPI YoY stood at -0.10%. Gold plunged 3.80% to 4,376.90, reflecting broader safe-haven unwind, and Bitcoin fell 3.41% to 68,879.55 in sync with equity weakness.

No major macro data releases occurred across the region, keeping focus on market reactions to external shocks.

The Day Ahead

March 26 brings a quiet calendar for Greater China with no scheduled data releases or events from mainland China, Hong Kong, or Taiwan, allowing markets to digest ongoing Iran war developments and their implications for trade flows. Investors will monitor any PBoC liquidity injections via open market operations to stabilize the yuan amid petroyuan buzz. In Taiwan, attention remains on semiconductor export sentiment following recent strength, potentially influencing CBC's FX stance.

Hong Kong's aggregate balance dynamics could see subtle shifts if HKMA intervenes to defend the USD/HKD peg against volatility. Broader geopolitical updates, such as South China Sea talks or cross-strait tensions, may emerge to drive intraday moves. Overall, expect sentiment-driven trading with eyes on global oil prices impacting China's import bill.

Other Economic Notes

Mainland China's property sector faces ongoing headwinds, with small factories battered by the Iran war's supply disruptions despite official pledges of stability from Premier Li Qiang. (cont...)