Greater China Macro Daily(Beta Mode)

China PMIs Beat, Markets Mixed

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,924.40 | +0.03% |

| CSI 300 | 4,494.33 | +0.05% |

| Hang Seng | 24,750.79 | -0.81% |

| TAIEX | 32,518.16 | -1.80% |

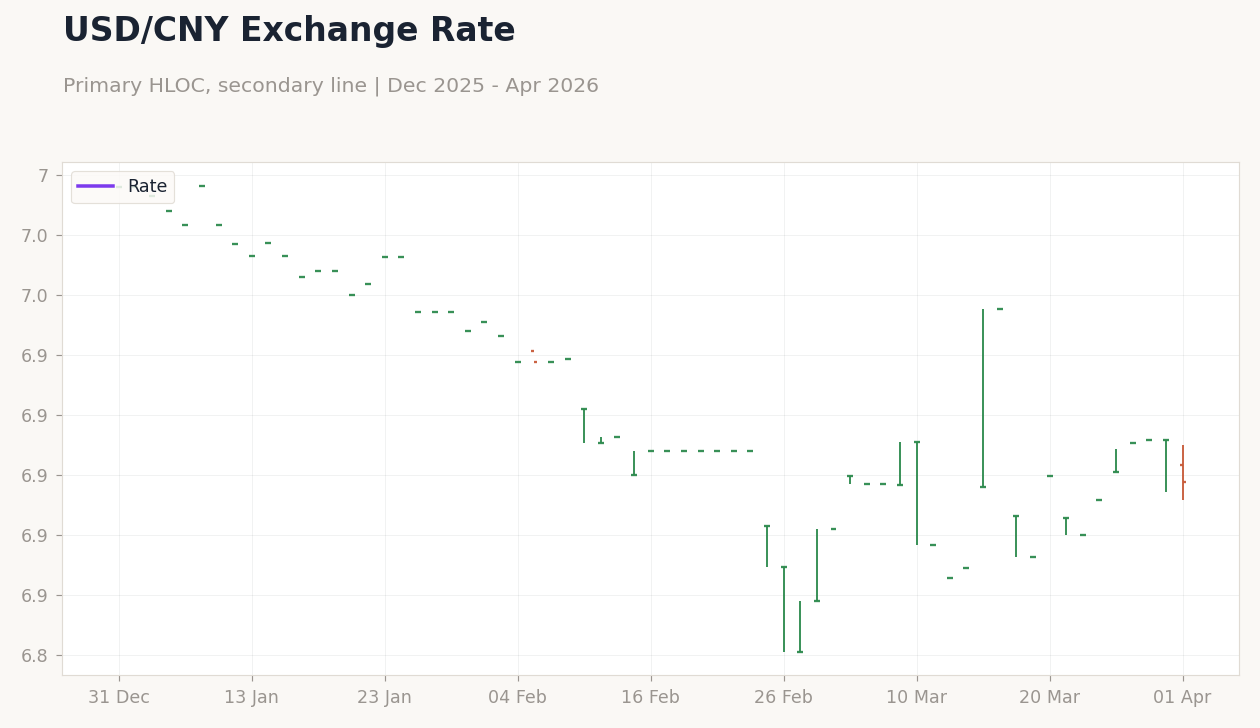

| USD/CNY | 6.90 | -0.20% |

| USD/HKD | 7.84 | +0.04% |

| Copper | 5.65 | +3.21% |

| Brent Crude | 103.28 | -8.42% |

| Gold | 4,699.60 | +3.84% |

| Bitcoin | 68,222.98 | +2.30% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NBS Manufacturing PMI | 49 | 50.10 | 50.40 |

| NBS Non-Manufacturing PMI | 49.50 | 49.90 | 50.10 |

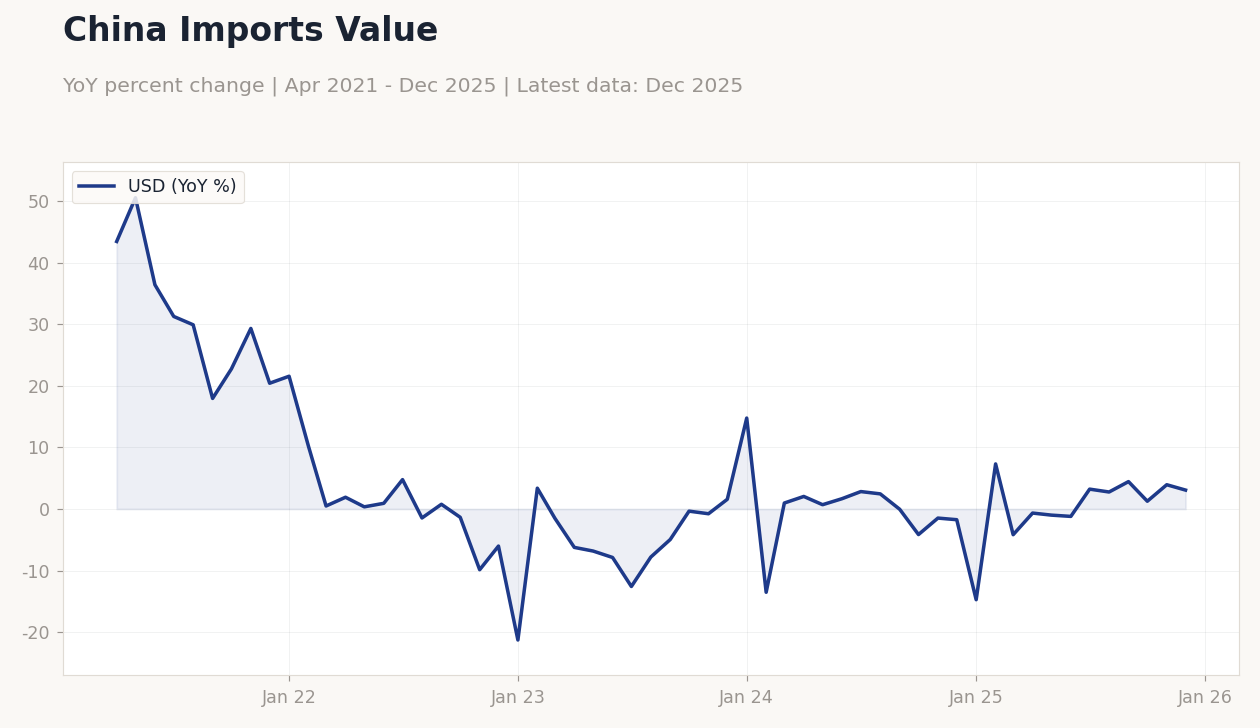

China Imports Value | Type: macro_line | USD: 3.066 (2025-12-01) | Range: -21.28–50.54 | Trend(5pt): 43.43,0.9165,-7.811,-4.153,3.066

China Imports Value | Type: macro_line | USD: 3.066 (2025-12-01) | Range: -21.28–50.54 | Trend(5pt): 43.43,0.9165,-7.811,-4.153,3.066

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RatingDog Manufacturing PMI | 52.10 | 51.60 | 17:45 |

| RatingDog Services PMI | 56.70 | 53.70 | 17:45 |

- Mainland China's NBS Manufacturing PMI rose to 50.4 in March, beating consensus of 50.1 and signaling expansion amid policy support.

- Hong Kong exporter confidence dropped sharply, while Taiwan semiconductor exports showed strength in related news.

- Equities were mixed: modest gains in mainland indices contrasted with declines in Hang Seng and TAIEX amid global tensions.

Yesterday's Recap

Mainland China's NBS Manufacturing PMI for March came in at 50.4, surpassing the consensus estimate of 50.1 and previous reading of 49.0, indicating the first expansion in six months driven by improved new orders and production. The NBS Non-Manufacturing PMI edged up to 50.1, beating expectations of 49.9 from a prior 49.5, reflecting a slight recovery in services activity amid ongoing stimulus measures. Shanghai Composite closed at 3,924.40 with a +0.03% gain, while CSI 300 rose +0.05% to 4,494.33, supported by optimism over manufacturing stabilization.

In Hong Kong, the Hang Seng index fell -0.81% to 24,750.79, pressured by exporter confidence hitting a two-year low amid trade turbulence. Taiwan's TAIEX dropped -1.80% to 32,518.16, weighed down by geopolitical concerns despite positive semiconductor outlook. USD/CNY weakened -0.20% to 6.90, reflecting mild depreciation, while USD/HKD ticked up +0.04% to 7.84 within the peg range.

Copper prices, a key proxy for China growth, surged +3.21% to 5.65, offsetting Brent crude's -8.42% drop to 103.28 amid Middle East instability.

The Day Ahead

Mainland China's RatingDog Manufacturing PMI is due at 17:45 ET today, with consensus expecting a dip to 51.6 from the previous 52.1, potentially signaling moderation in private sector activity. The RatingDog Services PMI, scheduled for April 2 at 17:45 ET, is forecasted at 53.7 versus prior 56.7, which could highlight cooling in non-manufacturing amid external pressures. No major data releases are slated for Hong Kong or Taiwan today, allowing focus on mainland indicators.

Investors will watch for any PBOC signals on liquidity following recent reference rate adjustments. Geopolitical developments, including Middle East tensions, may influence cross-strait sentiment. Tomorrow brings no key events, shifting attention to broader global cues.

Other Economic Notes

Mainland China's property sector shows tentative signs of revival with Hong Kong homebuyers piling into new launches despite rate jitters and Middle East tensions, though broader confidence remains fragile. Taiwan's semiconductor industry benefits from strong underlying growth, as evidenced by TSMC's Q4 demand lift, bolstering export outlook amid global AI chip needs. (cont...)