Greater China Macro Daily(Beta Mode)

China PMIs Firm, Stocks Climb

Market Snapshot

| Asset | Level | Change |

|---|---|---|

| Shanghai Composite | 3,944.83 | +1.36% |

| CSI 300 | 4,517.52 | +1.52% |

| Hang Seng | 24,788.14 | +0.15% |

| TAIEX | 31,722.99 | -2.45% |

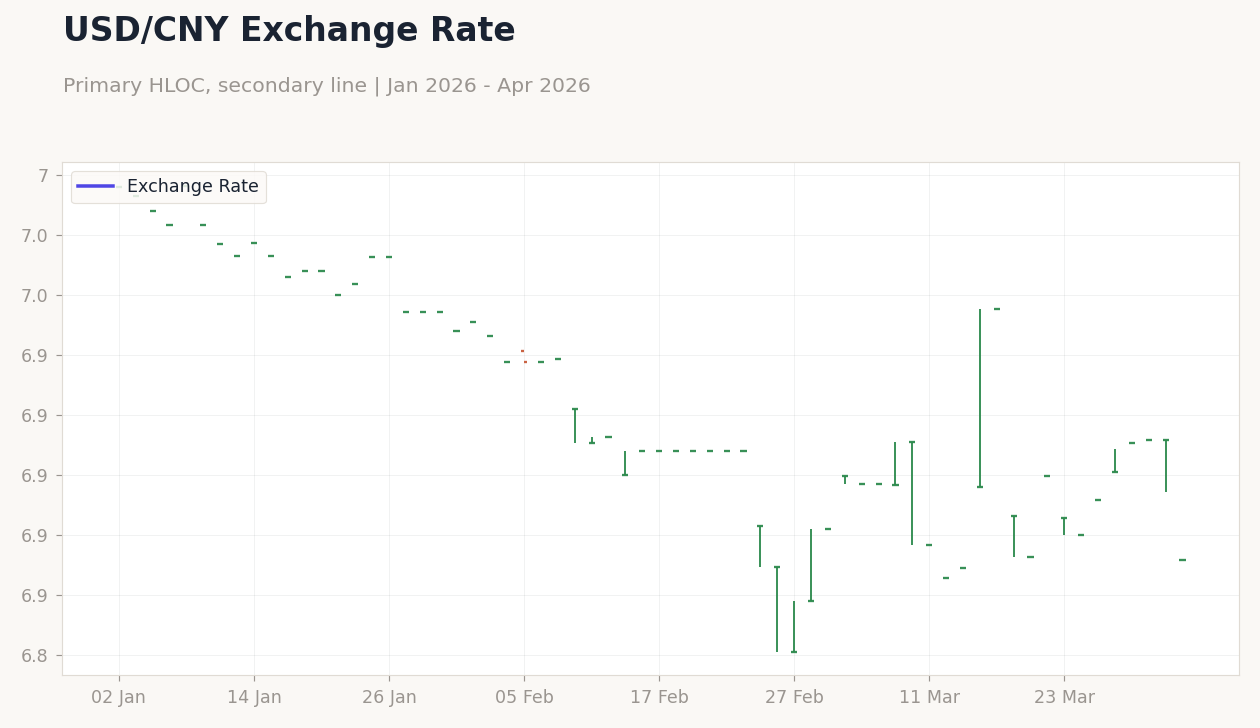

| USD/CNY | 6.87 | -0.58% |

| USD/HKD | 7.84 | -0.02% |

| Copper | 5.62 | +0.54% |

| Brent Crude | 100.30 | -15.25% |

| Gold | 4,784.60 | +2.95% |

| Bitcoin | 68,339.59 | +0.16% |

| China 2Y Govt Yield | - | - |

| China 10Y Govt Yield | - | - |

Prior Economic Events

| Data | Prior | Cons | Actual |

|---|---|---|---|

| NBS Manufacturing PMI | 49 | 50.10 | 50.40 |

| NBS Non-Manufacturing PMI | 49.50 | 49.90 | 50.10 |

| RatingDog Manufacturing PMI | 52.10 | 51.60 | 50.80 |

Shanghai vs Hang Seng | Type: market_hloc | Shanghai: 3892 (2026-03-31) | Range: 3813–4183 | Trend(5pt): 4023,4136,4134,4129,3892 | Hang Seng: 2.479e+04 (2026-03-31) | Range: 2.438e+04–2.797e+04 | Trend(5pt): 2.634e+04,2.675e+04,2.657e+04,2.59e+04,2.479e+04

Shanghai vs Hang Seng | Type: market_hloc | Shanghai: 3892 (2026-03-31) | Range: 3813–4183 | Trend(5pt): 4023,4136,4134,4129,3892 | Hang Seng: 2.479e+04 (2026-03-31) | Range: 2.438e+04–2.797e+04 | Trend(5pt): 2.634e+04,2.675e+04,2.657e+04,2.59e+04,2.479e+04

Today's Economic Events

| Data | Prior | Cons | Time |

|---|---|---|---|

| RatingDog Services PMI | 56.70 | 53.70 | 21:45 |

- Mainland China's NBS Manufacturing PMI rose to 50.4 in March, beating consensus of 50.1, signaling expansion amid recovering factory activity.

- RatingDog Manufacturing PMI eased to 50.8, missing expectations of 51.6, while non-manufacturing gauges showed modest gains.

- Equities advanced in mainland China and Hong Kong, buoyed by PMI data, though Taiwan's TAIEX declined on tech sector volatility.

Yesterday's Recap

Mainland China's NBS Manufacturing PMI for March climbed to 50.4 from 49.0, surpassing consensus of 50.1 and marking the first expansion in six months, driven by stronger new orders and production amid policy support. The NBS Non-Manufacturing PMI edged up to 50.1 from 49.5, slightly above expectations of 49.9, reflecting resilience in services despite property sector headwinds. RatingDog Manufacturing PMI dipped to 50.8 from 52.1, below consensus of 51.6, highlighting subdued export demand due to global trade tensions.

Mainland equities rallied on the PMI beats, with the Shanghai Composite closing at 3,944.83 for a 1.36% gain and the CSI 300 at 4,517.52 up 1.52%, led by industrials and materials amid copper price rises. Hong Kong's Hang Seng index inched up 0.15% to 24,788.14, supported by retail sales growth of nearly 12% in the first two months of 2026, though property supply concerns lingered. Taiwan's TAIEX fell 2.45% to 31,722.99, pressured by semiconductor export uncertainties linked to global supply chain disruptions from the Iran conflict.

Currency markets saw USD/CNY weaken 0.58% to 6.87, reflecting PBoC stabilization efforts, while USD/HKD held steady at 7.84 with a minor 0.02% dip.

The Day Ahead

Attention turns to mainland China's RatingDog Services PMI for March, due at 21:45 ET, with consensus expecting a decline to 53.7 from February's 56.7, potentially signaling cooling in the services sector amid economic slowdown. No major data releases are scheduled for Hong Kong or Taiwan, allowing markets to digest recent PMI figures and global oil volatility. Investors will monitor any State Council signals on property sector redesign, as news highlights ambitions to shift away from real estate dependency.

Cross-strait trade flows may come into focus with ongoing geopolitical tensions, particularly affecting Taiwan's semiconductor outlook. Broader Greater China sentiment could be influenced by commodity moves, with copper as a key proxy for mainland demand.

Other Economic Notes

Mainland China's push to rebalance trade, as reaffirmed in Qiushi journal, emphasizes moving away from unsustainable export-led growth amid rising global protectionism, potentially boosting domestic consumption and high-tech sectors. (cont...)